Rise of Hard Money is a Harbinger of Misery

Bitcoin’s coming rise to $1 million within 4 years and gold’s renewed rise, are a harbinger of an imminent, crippling stagflationary, economic collapse. See also my subsequent blog Secrets of Bitcoin’s Dystopian Valuation Model.

I wrote:

Bitcoin is a wrecking ball destroying all the status-quo, sweeping it aside as refuse† of the creative destruction necessary to usher in the new world.

Continued from prior post:

Armstrong wrote:

6th Wave […] isn’t a walk in the park to some glorified new age of knowledge […] cannot leave behind the majority.

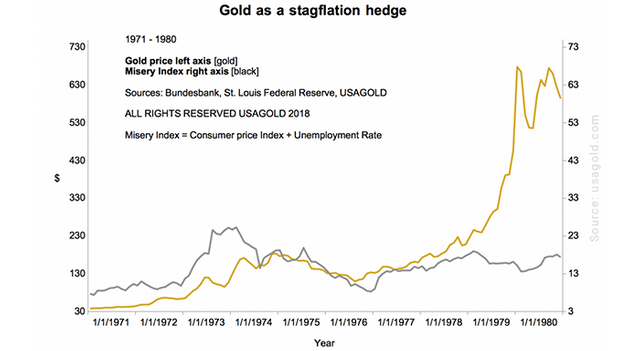

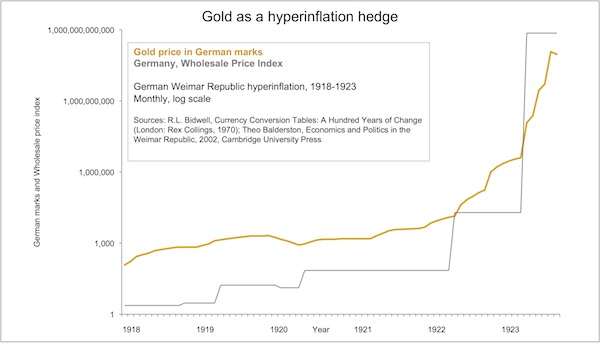

Gold in times of crises

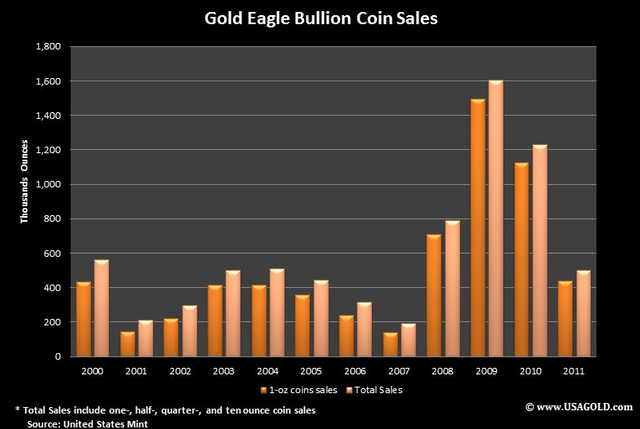

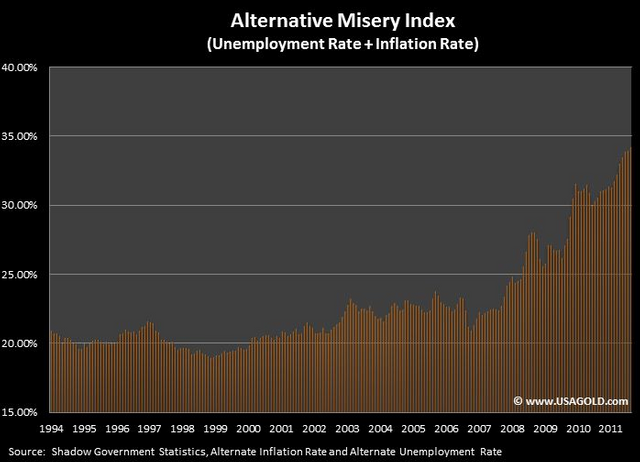

Strong Correlation Between “Misery Index” and Gold Demand

Bitcoin Price Boom Signals Massive Dystopian Panic Over 2019 Recession: Analyst

The sudden swell of Bitcoin’s price to $8,000 USD this year shows global recession fears are mounting. This according to Michael Hartnett, the chief investment strategist at Bank of America Merrill Lynch […] He argues the effect of low-interest rates since 2008 on bond yields has left investors starved of profits, sending them into a global “greed trade” across corporate, emerging market, and crypto securities.

If major global investors that used to invest in bonds, the safest assets in the world, have jumped ship to swim for bitcoin — the ponzi scheme currency of lunatics, hackers, scammers, criminals, misfits, and the hopelessly naive — how bad do the world’s big players know things are? Terrifying.Bitcoin proponents should pause the victory lap for a moment and let it sink in how weird this is. Regular-ish, everyday-ish people with deep pockets who used to buy investments like bonds are now investing like all the fringe lunatics.

That is a massive and very sudden collapse of confidence in the world’s governments and the basic structure of the financial system. This could be some fall of the Roman Empire level phenomena unfolding before our very eyes in real time.

“We have long been skeptical of cryptocurrencies' value in most environments other than a dystopian one characterized by a loss of faith in all major reserve assets (dollar, euro, yen, gold) and in the payments system,”John Normand, JPMorgan's head of cross-asset fundamental strategy, said in a research note earlier this year.Dystopia is the mother of invention. Well, bitcoin’s value is clearly very high. A tsunami of investors have now joined the early adopters in hoarding the digital asset like it’s running out. Which it is. So by this JP Morgan head’s reasoning, the escalating U.S. China trade war among other global macro trends has pushed the economic environment to the brink of dystopia.

And now a Bank of America Chief is saying investors are losing faith in our government and the financial establishment. But no one needed a big bank chief to tell us they’re flipping their guts over what the establishment’s doing to their money right now. Bitcoin’s early adopters know how afraid of bitcoin the rest of the world was.

Armstrong wrote:

Money and assets are always on opposite sides. When even gold was money it was not this miracle stability within an economic sea of chaos.

The problem has NEVER been what is money – the real problem has ALWAYS been government mismanagement. So returning to a gold standard would never make politicians honest since we had Bretton Woods and they blew that gold standard up as well.

Prosperity Coincides With Loosening of Hard Money

The End Game for Fiat Currency

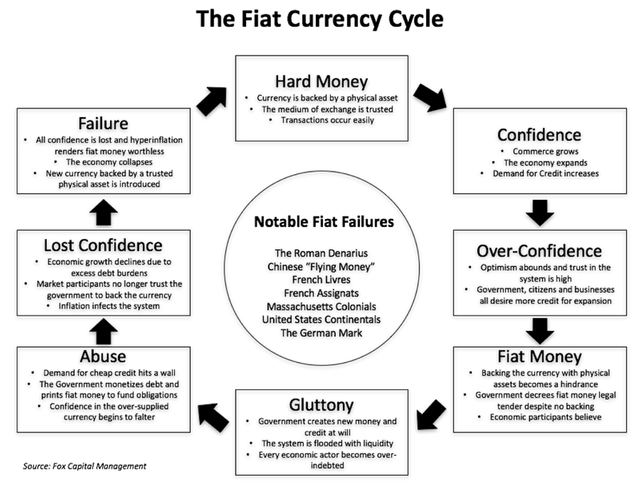

Predicting the inevitable demise of a fiat currency cycle is neither bold nor incendiary. For thousands of years, every fiat currency cycle the world has ever known started and ended the same way. It happened during the Roman Empire with the Denarius, in China during the 11th century with paper “flying money,” in France multiple times beginning with infamous central banker John Law’s Banque General, in the early USA with paper Colonials and Continentals, and perhaps most famously in Weimar Germany with the Mark after WWI. All fiat currencies eventually collapse, and largely for the same reason: the issuing government becomes over-indebted and abuses its privilege by debasing its specie or over-printing its money, which results in a logical collapse of confidence. Timing the ultimate demise is difficult, but having confidence in its inevitability is not.

Cycles are a basic natural phenomenon and are thus unavoidable. For money, the cycle always begins with “hard” currency containing or backed by a physical asset, typically a valuable commodity like gold, copper or silver. Users of the currency have confidence in its value because they know it is or represents a certain amount of something tangible. The medium of exchange is trusted, transactions occur, the system runs smoothly and the economy grows. Eventually, the issuing government becomes over-confident in its success and grows tired of dealing with the constraints this hard-exchange requirement places upon its ability to borrow, spend and expand.

It is at this point in the cycle that the issuing government decrees by fiat (“let it be done” in Latin) that its currency is no longer exchangeable for any tangible asset or commodity, but is instead backed by a promise that the government is “good for it” via its taxing authority or other means. Thus, the money transitions from hard currency to “legal tender” fiat currency, with no intrinsic value beyond the word of its issuer.

With confidence in the system still high, the issuing government is now free to create and borrow fiat money at will for infrastructure projects, welfare programs, expansionary wars and anything else they deem worthwhile. Without the fetters of a hard currency, money is created and spent seamlessly, with the entire system awash in credit as confidence abounds. The good times roll.

Eventually, however, both the government and its citizens become stretched beyond their means, and the economic demand for fiat money, regardless of how cheap it is to borrow, begins to hit a wall. As the credit cycle falls into a downward spiral, the government printing presses go into overdrive, creating new money out of thin air to pay off debts, meet excessive social requirements, and fund bloated operations.

Once it becomes clear that the government is blatantly abusing its unique privilege of creating fiat money, confidence in the currency and the issuer behind it begins to falter. Purchasing tangible assets requires more and more fiat currency. Inflation infects the system as people scramble to exchange their weakening currency for hard commodities and resources. This happens slowly at first, then all at once. Ultimately, confidence is completely lost, and the once-valuable fiat currency is literally not worth the paper it is printed on. The systemic collapse of the monetary system is complete as the cycle reaches its revolution.

In order to build a new monetary and economic system out of the ashes, the next government must first rebuild confidence in the medium of exchange. Thus, they introduce a new form of hard currency fully exchangeable for a tangible asset like gold, copper or silver. Confidence is restored and the cycle begins anew. Wash, rinse, repeat.

Where We Are in the Cycle

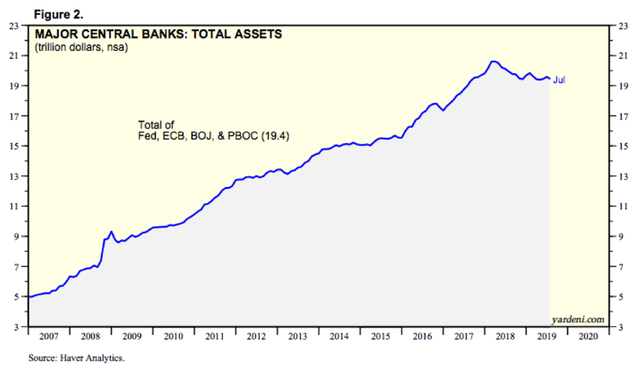

[…] Quantitative easing quickly created a large increase in excess reserves in the banking system. This in turn led to excess demand for “risk-free” sovereign debt and investment grade assets. It also ensured market participants that there was a large and persistent buyer regardless of conditions. These unconventional policies (ZIRP and QE) led directly to a universal scramble for yield at any price, artificially low volatility, an abandonment of traditional price discovery mechanisms, and a massive distortion for the pricing of risk. Even more troubling is that the patient became wholly addicted to this “emergency” medicine which was supposed to be just a temporary measure.

With every major central bank following the same playbook post the GFC, global central bank balance sheets swelled from $5 trillion in 2007 to over $19 trillion today. During the last few years, central banks attempted to normalize their bloated balance sheets, but they quickly discovered that financial markets are now fully reliant upon excess liquidity to function properly. All central banks have since abandoned those plans, with the ECB just announcing a new round of open-ended QE after pausing for a scant nine months, and the Fed increasing its balance sheet again via emergency repo operations just last week. The addicted patient has made it clear that any withdrawal of stimulus medication will result in systemic volatility. Of course, central banks view any such turbulence as unacceptable with such a fragile economic backdrop. Rock, meet a hard place.

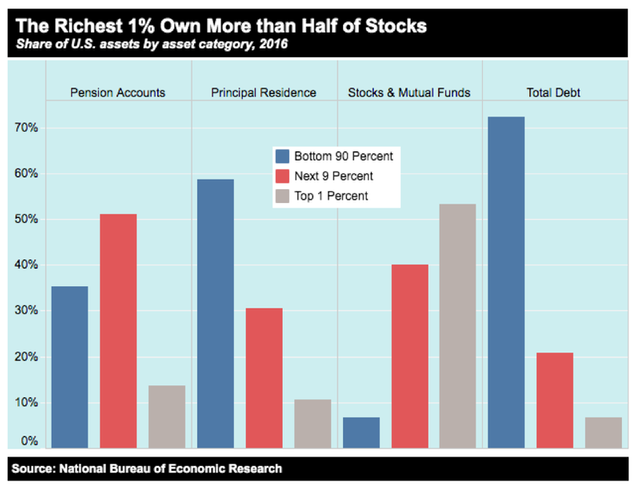

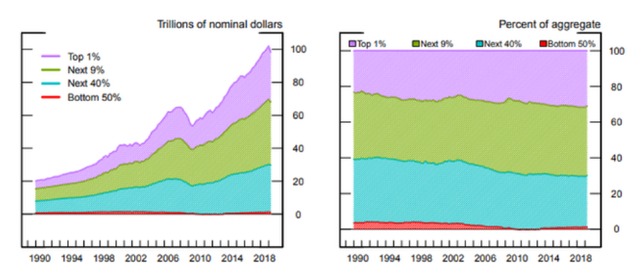

Another unintended consequence of these unconventional monetary policies is the historic wealth gap, and the polarized social and political environment that accompanies such extreme differences between the rich and the poor. By bailing out the banking system in 2008, and then inflating financial asset prices (stocks & bonds) on every market wobble since then, central banks have demonstrated a clear policy of “socialism for the rich” and “capitalism for the poor.” The vast majority of citizens do not possess large securities accounts, so asset price inflation increasingly benefits fewer and fewer people, widening the skew between the “haves” and “have-nots” (the richest 1% own over 50% of stocks). One might think that the massive amount of monetary and fiscal stimulus would benefit the working class through the corporate channel, but it turns out that corporations just used artificially low interest rates and tax cuts for financial engineering. Instead of investing in their businesses, they simply levered up their balance sheets for stock buybacks and M&A to boost equity option prices. In fact, while corporations have levered up to historic extremes, capital expenditures have languished and worker compensation as a percent of sales has actually declined. So, the rich have gotten a lot richer, while the poor have seen little benefit from these experimental policies, and have actually been punished as savers by artificially low rates. Ironically, the only equality lies in every citizen’s shared obligation for the massive pile of new government debt that’s been created.

This huge chasm between the haves and have-nots has naturally led to extreme social and political polarization, with “populism” on the rise in both factions. Formerly extreme liberal viewpoints in the US have become more mainstream policy, as the have-nots demand socialism for all, not just for the rich. They argue that the monetary and fiscal policy that has served the elites so well should now benefit the masses through deficit monetization, government funding of entitlement programs, loan forgiveness, universal basic income, and hefty taxes on corporations and the rich. In short, they want wealth redistribution and control of the printing presses to get what’s “owed” to them, and they very well might succeed given the current social mood.

[…]

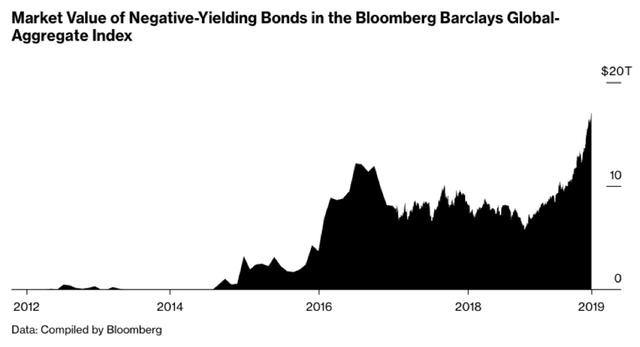

Negative Rates

[…] There is now currently over $17 trillion of negative yielding debt in the world today, so this has become a mainstream phenomenon […]

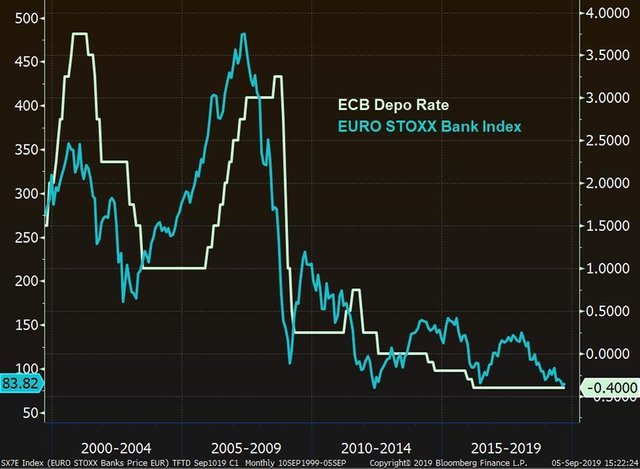

Negative rates are antithetical to financial theory and create a perversion of asset and risk pricing models. When using a negative number as your risk-free rate to determine the present value of future cash flows, cash becomes more valuable than any asset. This creates a serious problem for the banking sector. Investors dump bonds for cash, but do not want to pay a fee (negative rate) to park money in the banking system. As depositors withdraw their cash, bank capital becomes compromised, and they are unable to dig out because their business model has been completely destroyed, first by compressed net margins, and finally by negative rates. This “run on the bank” thrusts the fractional reserve money multiplier into reverse, sucking liquidity from a system now fully reliant upon it. European bank executives are pleading daily for the ECB to move off of negative deposit rates, but this is not going to happen, as new ECB chief Christine Lagarde (not coincidentally a debt workout lawyer) has recently hinted at even more negative rates. Ironically, the experimental medicine which saved the banking system (ZIRP & QE) is now actually killing the patient, and there is no way out of this conundrum.

Another problem facing central banks is that negative policy rates paradoxically LOWER inflation expectations as it stokes deflationary psychology, and the lack of income for savers actually increases the savings rate and not consumer spending. Just recently the Federal Reserve of San Francisco published a white paper which concluded that inflation expectations in Japan dropped immediately after the BOJ first took rates negative in 2016 and remain even lower today. In Germany, the personal savings rate has INCREASED significantly since the ECB deposit rate went below zero […] Finally, for pension and entitlement programs, negative rates destroy the model. Aside from the inability to generate any yield from their fixed income investments to meet obligations, pensions use a discount rate to determine proper funding requirements. Using a negative discount rate would render all pensions technically underfunded. Quite a dilemma to say the least.

[…]

Fire and Ice

So how does this all play out? There are obviously many routes and outcomes for all the players and markets involved. That said, we do believe that some results are more likely than others, and that a few are simply unavoidable. From a big picture standpoint, the progression is likely to be led by further debt deflation and economic contraction (Ice), followed by the final act of hyper-inflation as all sovereign debt and fiat currency becomes entirely mistrusted (Fire). […] However, knowing full well that this is a road to ruin, central banks will also continue to build gold reserves (which they have been doing for years) to have on hand as many poker chips as possible when the new post-collapse global monetary regime is established, undeniably with gold as its anchor. By that point, central banks will probably (and correctly) be recognized as the biggest culprits for the systemic failure. Ultimately, they will be abolished and disbanded. […]

For the business sector, historically high leverage ratios will become unmanageable and the demise of financial engineering will occur right when recessionary conditions obligate layoffs and spending freezes. Populist policies will increase the tax and regulation burden as the corporate sector faces backlash from decades of elitist treatment, and stock options and buybacks will become outlawed. Worker revolts will be supported by the government, and long overdue bankruptcies of profligate companies will explode. Large industries will become nationalized in an effort to stem the tidal wave of layoffs and unemployment, coinciding with a mass disintegration of stock and bond securities amidst a global depression.

This progression will be aided by populist government policy driven by the “have-nots” who finally get in power and legislate the transition from “socialism for the rich” to socialism for all, with higher spending and crippling taxes on the wealthy. Despite record deficits and government debt/GDP ratios, fiscal spending will go into overdrive, further compromising the credit quality of sovereign issuers. As citizens begin to doubt the value of fiat currency backed solely by over-leveraged sovereigns, and the rich attempt to export their financial assets to safer havens, governments will enact capital controls while outlawing cash, private gold ownership and crypto currencies. Globally, protectionist policies and trade wars will ignite into real wars, as each country scrambles for physical resources while exchanging as much of their eroding fiat paper for hard assets as quickly as possible (Trump’s recent offer to buy Greenland doesn’t seem so funny within this context). Global discord will make cooperation in the face of sovereign debt restructurings extremely difficult at the worst possible time. It will likely require the pain of total collapse before necessity dictates rational compromise among wary nations for a new financial framework.

Armstrong wrote:

I am sorry, but you cannot possibly demonstrate that only a tangible monetary system would work when in fact the medium of exchange is solely based upon intangible human desires post-Bronze Age. Before 1650 BC, money was tangible because it was a barter system among people.

Money became intangible post-1650 BC (REPRESENTATIVE) and based solely upon CONFIDENCE that others will also accept whatever the form of payment might be.Gold is a LUXURY — it is not a TANGIBLE based monetary unit for it has no utilitarian value whatsoever. If you try to argue that TANGIBLE based monetary systems are better, that is barter and in that case, the medium of exchange must have some sort of use value such as food or bronze. Never do we see Gold forming some sort of TANGIBLE based monetary system.

Gold ONLY emerged as a medium of exchange because it was once exclusively the property of royalty, and as such, it was a luxury with no practical use as food or a weapon. Therefore, gold is not TANGIBLE but it historically also requires CONFIDENCE to exist as a medium of exchange as does paper money or receipts.You need to get you definitions correct. Any form of a medium of exchange which is TANGIBLE must have some practical utilitarian based value. Gold was a luxury and required the CONFIDENCE that someone else would also desire it for if they did not, then what would you do with it since you could neither eat gold not use it as a weapon.

Above Armstrong is pointing out that gold has a very high stocks-to-flows ratio because it has nearly no utility other than for hodling.

Armstrong wrote:

The whole argument is a gold standard inhibited growth and created massive deflation – the 26 year Long Depression of the late 19th century. Gold does not provide for a stable monetary system and that is why Bretton Woods collapsed. Gold should remain as a private investment/hedge.

Money cannot be fixed in value while everything else floats.

Buy gold for personal reasons and as a hedge against government. If you want money to be tangible and of some constant value, then you will never see a raise, your house must remain the same price, and no investment becomes possible other than money.

We will end up with a new currency anyway and it will not be gold backed or some fixed exchange rate that is anti-freedom.

That is what Marx tried. Paint your entire body. You will die because your skin needs to breath.The monetary system[…]must fluctuate. Flat-line it and you kill society – you are dead. Cheer up! A new currency is coming.

From §Background on the Money Question, Part Two of “Money in the Gilded Age”:

Officially, the nation's money was based on gold and silver before the Civil War,

but in practice, paper money entrepreneurship fueled economic expansion. In the antebellum period local and State banks could print their own money, and in the twenty years before the Civil War more than 4000 different kinds of paper money circulated. Even more striking, according to the Treasury Department, more than forty percent of the money in circulation was counterfeit.

The North printed more than 450 million dollars in paper notes, popularly termed "Greenbacks." It used them to pay soldiers and suppliers, and from there they entered the economy. Greenbacks let Lincoln finance the unpopular war. Greenbacks let Lincoln finance the unpopular war.

They also produced an economic boom for the North.

From Why conservatives spin fairytales about the gold standard:

Hard money meant a general deflation of prices in relation to the dollar. Each year from 1875 to 1896, farm prices fell 3 percent. Georgia farmers saw the price of a pound of cotton fall from 10 cents to 5 cents […] Corn prices fell so low that Nebraska farmers decided to burn it for fuel rather than spend money and time shipping it to market to sell it.

If farmers could get a loan or a mortgage, hard money made it more expensive to pay off. When the real value of the dollar rose, the real value of their debts rose with it. Farmers had to sell a lot more wheat or corn to meet those debts.

Scarce credit combined with scarce dollars. Because the Eastern banks had a monopoly on issuing bank notes, farmers in the West and South often lacked access to currency. The lack of dollars in rural America became particularly acute after the growing season, when there was insufficient currency to move the harvest to market.

Farmers were not alone when it came to the burdens of hard money. During the long economic depressions of the 1870s and 1890s, workers and manufacturers felt the weight of the same deflationary price cycle. They asked why anyone would invest in an iron mill, for example, when the price per ton of iron stagnated or fell.

Gold made losers of farmers and other working people selling goods at deflated prices. It made losers of people who paid mortgages and owed debts. And it made losers of those who lacked access to credit and currency.

But gold was good for those who controlled the currency, held gold or issued loans. It was good for the banking corporations, Wall Street financiers and other creditors. As a result,

the gold standard shifted resources from the poor to the rich, and from the Midwest, West and South to the financial centers of the Northeast.

Armstrong wrote:

Before the Protestant Reformation,

banking was exclusively a Jewish industry for Catholics had the sin of usury. Catholics who wanted to get into the banking industry funded the Protestant Reformation as their cover to take over banking.Medieval [Jewish] bankers were merchants prior to

St. Thomas Aquinas who declared money lending to be a sinin Summa Theologica,which cleared the field of Christians. The first bankers coming out of the Dark Ageswere northern Italians, not Jews.

Armstrong wrote:

[

During the 600 year Dark Age] the banking industry remained largely tempered and controlled. Fees could be collected for providing a service butthe practice of lending money for interest was strictly forbidden due to the Sin of Usury.

The line that divides the medieval period and that of the birth of capitalism comes in during the Protestant Reformation. Take away the religious slogans and the political corruption that emerged with the Church at that time and what you are left with is the economic reasons for the rebellion. Prior to the Reformation, banking had been exclusively conducted by the Jewish community. Their religion was the only one in the west that did not deem lending money to be a sin. Catholics, who engaged in lending for interest, ran the risk of being excommunicated from the Church. The Protestants used this restriction as evidence that the Pope was the Anti-Christ suggesting that he was attempting to control the people by prohibiting the buying or selling on credit, as similar to the warnings in the Revelations. Of course, this was an extreme interpretation of the Bible, but it served a political purpose. Economics credits the birth of capitalism with the Reformation because in the Protestant regions of Europe, Christians moved head first into banking.

Prior to the Protestant Reformation banking in the middle ages centered largely on the goldsmiths. This tradesman group accepted deposits and issued receipts in return. This effectively created the

rebirth[regression] of banking in the Middle Ages similar to that which had exists in Babylonian times.

the absence of banking and credit discourages human interaction and thus acts an impediment to economic and social growth. Too much debt and credit runs the risk of destroying the very foundations of civilization as witnessed by the fall of Athens and Rome. If there is one lesson to be learned from history, it is that need for moderation in both directions of the economic pendulum.

Armstrong wrote:

Aristotle[…]saw the[…]men, making money from money. This actually influenced Karl Marx.Aristotle did not understand the economic evolution process dynamically, which has taken place in ALL societies throughout recorded history. What Aristotle saw was the abandonment of what I have dubbed the Villa Economy of self-sufficiency and the gravitation of both people and capital toward commerce. This part of the economic cycle usually involves people becoming attracted to the big city and abandoning the farm life. Every society sees this oscillation both in the concentration of capital as well as people.

[He] tried to draw a line between capitalism that would assist economic growth and that which would fuel these booms and busts driven by speculation in his mind’s eye:

“Now money-making […]

for usury is most reasonably detested, as it is increasing our fortune by money itself, and not employing it for the purpose it was originally intended, namely exchange.”

Bitcoin Will Not Be Effectively Spendable

Continued from prior post:

such as the very onerous “proof of source of funds” […] on-chain transactions fees will be $1000+ when BTC is $1 million. Thus too few people transacting on-chain

The stock-to-flows model informs us that the BTC price and thus transaction fees will rise inexorably. This means BTC will over time kick more and more people off-chain, until eventually only the uber elite can transact on-chain.

Armstrong wrote:

They see that as 100% accountable for tax purposes. Any new currency will be a unit of account internationally with each currency converted into that […] The new currency will be electronic. This will be the RESERVE CURRENCY andthat will not be used in each country to buy things. This will be up there with the SWIFT CODE system.

Armstrong doesn’t realize he repeatedly describes the way Bitcoin will rise:

Only a two-tier currency system can possibly weather the economic storm on the horizonfrom the collapse of the European Union at the hand of this lethal combination of policies. The next banking crisis will most likely begin in the Eurozone due to a continued failure to resolve the systemic weaknesses of its construction. The failure to have consolidated the debts means that the failure on the state level will ripple through the entire European economy. In the United States, state debt is not used for reserves. The failure of California will only send bond seekers into the federal debt who are fleeing state and municipal debt. We see that in Europe as capital fled from most members concentrating in Germany, which is the US Treasury equivalent within the Eurozone. With the first bail-in under the BRRD agreement, the contagion will be devastating as was the case when Michigan closed its banks in 1933 in the USA.The Financial Rand fell below the domestic commercial rand when the 1992 political crisis unfolded, and capital fled South Africa unwilling to invest in a nation that might move into civil war.

The two-tier currency system can and does help to distinguish between domestic and international capital flows.

There is the potential to create a two-tier monetary system with a new type of international currency that is separate and distinct from that of the domestic currency. This would allow the US dollar to end its reserve status and end the clash between domestic and foreign policy objectives.

Bitcoin Will Be Politically Vilified And Confiscated

So many high pride fools who think that the rise of hard money is something that will enrich them at the expense of the rest of society. They want to prioritize living somewhere with a Disneyland or other trappings of normal society, and they fail to realize that the rise of hard money only coincidences with the loss of public confidence in society and government. So many fools wasting time on crypto scams that have no chance at all of being relevant to what is coming nor helping to avert it.

And reflect on how gold will also be vilified as a conduit for money laundering of illicit Bitcoins:

https://www.reddit.com/r/Bitcoin/comments/1lfobc/i_am_a_timetraveler_from_the_future_here_to_beg/

Governments tried to stay relevant in my society by buying Bitcoin, which just made the problem worse, by increasing the value of Bitcoin. Governments did so in secret of course, but my generation's "Snowdens" are in fact greedy government employees who transferred Bitcoin to their own private account, and escaped to anarchic places where no questions are asked as long as you can cough up some money.

All of us will be destroyed as I warned in 2010:

http://www.marketoracle.co.uk/Article20327.html

The following from the Reddit post is not entirely correct:

For anyone who hasn't yet figured out what's so backwards about the "inflation is good" argument, here's what's so blatantly wrong with this reasoning:

Whether or not someone saves money instead of spending it is in part due to the expectation of future purchasing power, which, roughly speaking, is positively correlated with economic activity, and negatively correlated with money supply. According to the OP's hypothetical, economic activity is slowing faster than the […] money supply is growing, so one would expect their purchasing power to be constantly decreasing. Decreasing purchasing power provides an incentive to purchase consumables, purchase durable goods for future consumption, or purchase durable goods for future trade. Performing any of those actions increases economic activity, and thus will start reversing the trend of decreasing purchasing power. This is a self-stabilizing system, and there's no reason to think that a constant money supply will lead to runaway collapse of an economy.

What you fail to incorporate in your reasoning is the perpetual halvings and doublings of the S/Fs ratio until 2141. Thus as I explained in detail in another blog, the economic activity of the world will not recover until the opportunity cost of mining is lower than those other productive human activities. Economic devastation due to technological unemployment comes first. Most humans have worthless skills in the new technological knowledge age economy with robotics for example replacing human labor.

Bitcoin vs. Gold

I wrote:

goldbugs are myopic absolutists that forever dream to live in a perfect world that can’t exist. They never think through the ramifications of what they want and compare the alternatives.

Friction always exists, for without it the past and future would be undifferentiated and we could not exist (everything would happen at the same spacetime and we couldn’t perceive any differentiation of past and future). Usury and proof-of-work are just forms of friction. What makes them somewhat less optimal is that some centralized entity is able to aggregate/leverage/funnel that friction into centralized power. Yet the power-law distribution is a fact of nature. It’s actually required (but I won’t go too deep into that because the explanation will become too abstract, theoretical, and complex).

Yet w.r.t. to fungibility and consensus systems, [some decades from now] a centralized power may be necessary to enforce and prevent disintegration into chaotic disagreement (e.g. forkathons with competing double-spends). You may argue that gold is fungible without any centralized power, but the centralized power facet enters at the level of the alternative choices civilization has for stored monetary value representation and the wars and disagreements those choices cause. Society is unwilling to allow some lazy fat cats sitting on gold doing nothing while extracting all the production from society in the form of deflation! That is why the money supply must increase (either via creating more of the same unit-of-account or alternatives becoming available).

Money is an information system that enables cooperation and civilization. The quantity theory of money is wrong, wrong, wrong at many different levels of analysis.

And wrote:

Another facet is that it has been shown that Bitcoin requires an oligarchy to form, else it will no longer converge on consensus as the transaction fees become significant relative to programmed block reward. Thus even if we posit that the global elite are not cooperating nor in control, then they must or a victor must form, else Bitcoin will eventually fork off into chaos. Yet we require the same about gold and the formation of a new monetary reset with a new reserve standard (that someone must take control to make the choice and enforce it). So one way or the other, some oligarchy must enforce order, else we end up in a Dark Age. But as I pointed out, the route to a new reserve standard via gold is impossible (you’ll end up with a scorched earth nuclear-bombs WW3 as the superpowers battle it out over due to collapsing economics and war-politics during massive deflation for which asset or mix of assets should be the reserve and who should oversee and control that)! Whereas, Bitcoin is virally replacing the world’s banking systems without any need for top-down political coordination.

Bitcoin is a market-based solution to an otherwise intractable globalization political problem. As @CoinCube had explained, globalism is all about maximizing coordination so that on the local level humans have more degrees-of-freedom and so the knowledge age can proceed. As he also explained, there’s no such thing as 100% decentralization, which is what would be required for @r0ach’s ([a] goldbug’s) theories about gold to be true. As Armstrong has explained many times, every form of fungible money is a fiat, even gold. It’s human greed, lust for power, and idolization of fungible stored monetary value which may lead them into the 666, while the non-fungible knowledge age provides an outlet for those who choose it. At the generative essence, for example the feminist politics is just non-meritorious greed and lust for power and the manipulation of religion/philosophy to accomplish such.Gold is not at all involved in this decentralization of information. It’s analogous to the comparison of the value of mechanically crushed gravel compared to etched silicon. The intellectual property component of the valuation is orders-of-magnitude differentiated. @r0ach (@realr0ach) why can’t you comprehend that purely monetary stored value is dying, because the industrial age and fixed capital investment is dying. Why can’t you comprehend my essay, “Rise of Knowledge, Demise of Finance”? You’re as myopic as the Luddites, who couldn’t accept that technology had changed the economics from their antiquated, truculent understanding of the world.

And wrote:

Your valuation of gold is presumably (given prior statements in this thread) based on the belief that it has always been money and always will be money (i.e. could be handed down to the children and grandchildren as a family heirloom), but that is historically false. Better forms of money come along and render the prior forms useless as money, e.g. sheepskins, shells, slabs of iron/bronze used to all be money. Gold was more compact, transportable and more fungible than the aforementioned antiquated forms of money. Paper money was even more so, but could be created willy-nilly by various nation-state regimes. Now crypto is even more so and adds the inability for any one nation-state to corrupt it’s invariants (e.g. protocol programmed money supply). And I’m (and I presume others are) working on even further improving the decentralized invariance of ledgers. Technology doesn’t stop moving forward just to accommodate old people who still think the world is flat.

It’s just time. Precious metals are nearly finished in human history. To all readers, we’re at the cusp of a major shift in the monetary history of the world. Get on the train or be left behind.

Afaics, all forms of fungible physical money are becoming defunct, including gold. Gold will become just like any other physical asset equivalent to real estate. It will no longer be effectively movable, because no one will be willing to buy it without paying tracked electronic money for it in exchange which of course the governments can then tax, confiscate, and restrict movement same as for real estate. Barter isn’t coming back. Gold will become trinkets for fondling and gazing, like jewelry, gaudy gold trim such as at the Trump executive suites.

I wrote in my previous blog:

¹ The killer app of Bitcoin instead appears to be as the reserve (i.e. “hodler”) currency of cryptocurrencies, and possibly eventually the de facto international reserve asset— at least in the Internet and intangible goods economic sphere wherein gold is a useless ancient relic, especially within the context of the said sphere.

Armstrong wrote:

maximum [gold] price[…]for 2032[…]$22,000 – $24,000[…] Those who think they can create their own currency […] Ain’t gonna happen

Those who thought they were clever and think they can make tax-free income in Bitcoin, all I have to say is – been there done that. There were tax straddles that allowed people to push income from one year to the next using futures. They were sold by the major brokerage houses in the late 1970s. The IRS allows such schemes to progress, then hits them with huge interest, penalties, and sometimes criminal prosecutions. If anyone thinks they can use Bitcoin tax-free – good luck. You are probably destined for real tax-free living at the closest Federal prison. Don’t worry, like Motel 6 – they will keep the light on for ya.

“How does one liquidate their gold holdings in a private manner?” Good luck. The French went after coins shows requiring that they report all attendees. The shows no longer go to Paris. The coin and bullion dealers were by law in France barred from dealing in cash. The French started to travel to Belgium to buy and sell gold.

Here follows another example of why demand for Bitcoin will trump demand for gold.

If buy 5 oz of gold or one BTC at ~$6k, then gold goes to maximum $20k but BTC to $1+ million. So if sell $100k at some point and hodl any remaining stash. So for gold 28% would be lost to taxes (USA taxation) because 100% of stash would be sold. For bitcoin, only 10% of the stash would be taxable (because only 10% of stash would be sold) and currently only at the portion above $38k would be taxed at 10%. So if the taxes on the $100k sold would only be paid after BTC reaches $1 million, then for that BTC scenario only 0.72% would be lost to taxes.

Note the tax calculation will vary by jurisdiction, e.g. there’s no capital gains tax (CGT) for UK residents on legal tender gold coins. And a tax break exclusive to a specific jurisdiction is risky because they can change the tax law suddenly before you sell. Whereas, with Bitcoin you have options such as (at least for USA residents) gifting it to someone in another jurisdiction tax-free.

Also Armstrong equivocated:

The speculation is rather absurd like gold will be $50,000 or $100,000 is just total nonsense […] for gold to reach such levels, nothing would be left including a place to even spend it […] The dark pictures they paint are not something gold would survive […] everything would rest back to the hunter-gather period meaning food is everything […]

The maximum our models project is $5,000. That is probably the point at which total chaos is unleashed anyhow and you end up with a completely new monetary system […] There is a high probability that they will declare gold illegal for transactions and prosecute under money laundering, which has been redefined as simply hiding money from government.

https://www.armstrongeconomics.com/markets-by-sector/precious-metals/gold/gold-silver-the-view/

I do not expect this target to rise above $5,000, butthat is entirely possible, although certainly not beyond $12,000 which is the most extreme possibility and is probably not attainable. Such a level at $12,000 appears very unlikely because the system would likely implode long before that would ever develop […]That is a projection based upon technical analysis ONLY. It is not the COMPUTER’S forecast since we first have to achieve the low.

https://www.armstrongeconomics.com/markets-by-sector/precious-metals/gold/gold-how-high-is-high/

$5,000 is the extreme maximum target– not the minimum.I do not see any possibility of $30,000or some other outrageous forecast. Even reaching $5,000 will not be easy, and we have to be concerned that they could simply declare gold illegal as they did in 1934

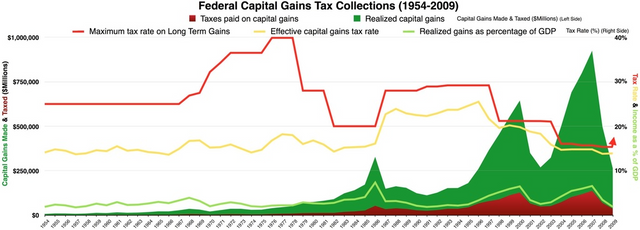

Taxes Rise Due to Politics of the Misery of Stagflation

Note that the CGT was raised from 25% to 40% during the 1970s which was the last time the USA suffered severe stagflation:

But now we have a more leftist leaning society, the public has not been invested in the stock market since 2009, and the stagflation will be much more severe in the coming decade especially in terms of levels of unemployment.

I discussed in more detail in the prior post (←you must click and read it), why the coming stagflation will be much worse than the 1970s. In that prior post I also explained why the Income Tax in the USA is unconstitutional. Armstrong clarified the history of the income tax:

Income tax was first implemented in Great Britain […] These were imposed out of necessity. The taxes signed by President Taft were more of a socialistic philosophy which was gaining support at least prior to the Russian Revolution in 1917. The rise of the “progressive” movement came into real force with the Panic of 1893.

As far as the

“voluntary” nature of the tax that is strictly true. However, the tax has a duty to file.The crime is a failure to file – not a failure to pay.

Aaron Russo’s Freedom To Fascism movie (←highly recommended you watch) documented the unconstitutionality of the IRS and the income tax:

Russo explains — to the former IRS Commissioner and General Consul to the IRS who helped write the tax code — that the law which Armstrong refers to which requires us to file is in violation of the Supreme Court and only supported by lower court which were violating the Supreme Court rulings as jurisprudence precedents:

And then the former IRS Commissioner Sheldon Cohen warned Russo in Yiddish as translated, “Nothing will help you.”:

After the movie and just before his death due to cancer, Russo gave a video interview with Alex Jones wherein he explained that Nicholas Rockefeller had told in advance about 9/11 and the coming plan for the 666 financial system:

In that interview Russo also explained that his motivation for making the Freedom To Fascism movie was the unconstitutional retroactive change to the tax code that cost him $600,000 in the 1980s (which should serve as a warning to those counting on for example the Puerto Rico tax exemption or any other form of tax avoidance maneuvers):

The world is going to be very jealous that a small % of the population is concentrating the wealth by making investments in USA stocks, gold, and Bitcoin:

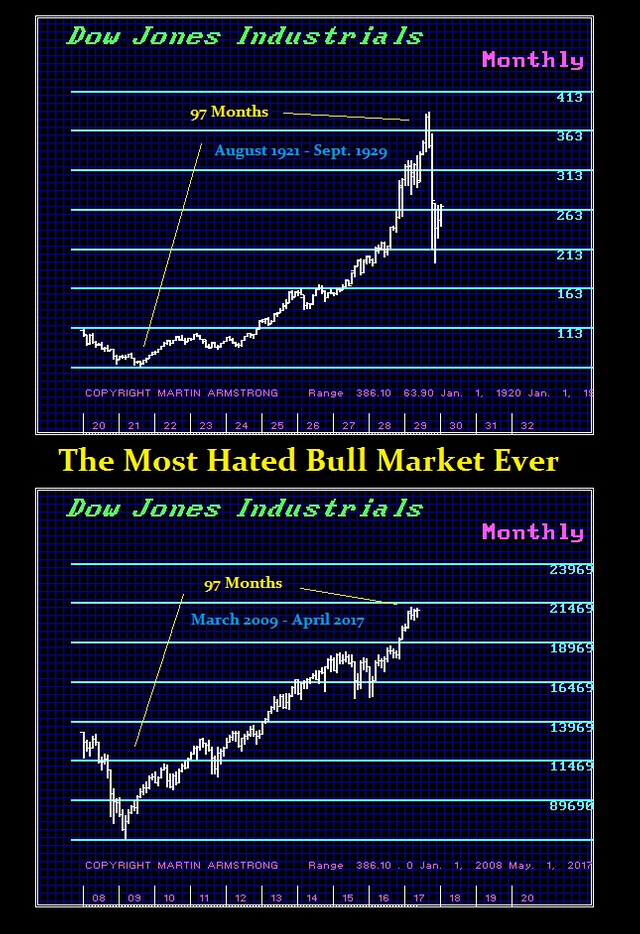

This has been the MOST HATED BULL MARKET in history. What is fascinating is how long this current bull market has been in play yet all we hear is how it is going to collapse like 1929 and fall to dust on the floor. I have been asked for interviews because they have been unable to find someone bullish.

We are facing a major cycle inversion beyond what most people have any concept of how markets trade because all they look at is 1929. Here we can see that the Roaring Bull Market of the 1920s lasted only 97 months. From March of 2009, this present bull market reached 97 months in April. This was the time for a pause and we got it. The S&P500 and the NASDAQ soared to new highs when the Dow did not. Yet in 1929 shoeshine boys were trading the market. This time, retail participation is still near the historic lows since 2007. After 97 months, you expect the bulk of people to be bullish, yet they are bearish. This is more than just a curiosity.

We are looking at a future that is astonishing. With the Dow now breaking out to new highs, we are preparing for the cycle inversion and a Phase Transition. We will be issuing a special report in a few weeks covering what will lead to the greatest trading trap of all time.

So buckle up. Get ready for the time of your life. Such opportunities come once in a few generations, not even in a single lifetime.

This rally since 2009 has been the most BEARISH rally ever in history. Think of this like the mirror image of gold. Gold has declined for 5 years and you have people screaming here we go with ever $20 rally. In the stock market, it has been exactly the opposite. Every time the market decline, they say here we go it will crash by 70-90%.

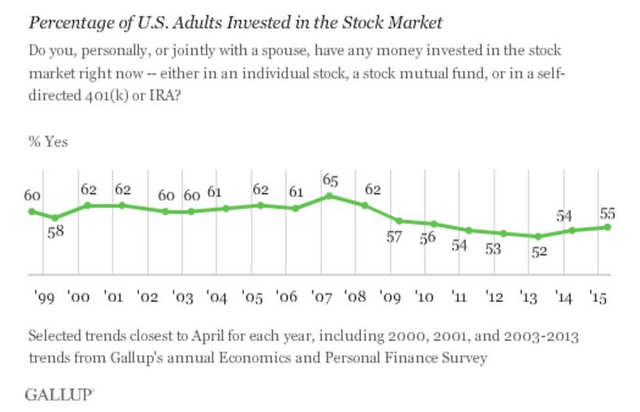

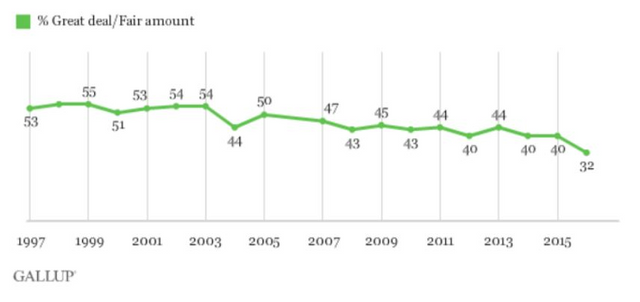

This is what I mean that the MAJORITY must always be wrong for they are the fuel that moves markets. I have been stating persistently that the Dow cannot “C R A S H” when the majority are bearish and retail participation is at historic lows (see Gallup poll).

The only real buyers have been due to the dollar, and sophisticated traders. The bulk of everyone else are BEARISH and cannot bring themselves to buy for they are still fighting the last rally in 2007 when they got caught.

Those who lost in 2007, just cannot bring themselves to say buy. This is why retail participation remains at historic lows. As long as that prevails, there is no way we have sufficient longs buying the highs from which a panic can then unfold by scaring the herd […] Only when the market crosses the 23,500 level do we see people surrendering and saying S H I T this is just going up […] All collapses unfold from highs with longs in panic. Major lows take place with shorts in panic. Short-covering at this stage demonstrates this is by no means a MATURE rally and we have a lot to go. Those who lost in 2007, just cannot bring themselves to say buy. This is why retail participation remains at historic lows.

When hard assets rise, (highly leveraged asset demand such as) real estate plummets, and the world goes into stagflation that is the precursor to massive social unrest, predatory taxation, capital controls and thus collapse. For those holding the hard assets, they see this as deflation not stagflation. But the masses experience stagflation.

From prior post:

With significant surge in such subversive usage, governments will increase regulation in an attempt to stop Bitcoin from subverting their capital controls, e.g. increasing enforcement of Anti-Money Laundering (AML), such as the very onerous “proof of source of funds” and “source of wealth”.

Readers should make sure they can unequivocally document the legal source of their funds.https://intercom.help/sharesies/legal-and-regulation/proving-source-of-funds-and-source-of-wealth

https://blog.revolut.com/what-is-source-of-funds-and-how-does-it-affect-me/

Armstrong wrote in Vancouver to Investigate Real Estate Buyers for Money Laundering:

they [the Canadian government] need to blame someone other than themselves. They released a report claiming that dirty foreign capital was the cause of the real estate boom. The real estate market is now under investigation for money laundering. It had been obvious for a long time that capital was parking in Vancouver. Now the twist will be to investigate and see where the money came from. If they can determine it is tainted,

they will confiscate the property.

Some additional articles of relevance I found:

https://www.armstrongeconomics.com/world-news/taxes/the-endless-hunt-for-taxes/

https://www.lewrockwell.com/2019/06/james-howard-kunstler/the-zeitgeist-knows/

https://www.oftwominds.com/blogjune19/quiet-revolution6-19.html

https://www.armstrongeconomics.com/markets-by-sector/interest-rates/when-will-interest-rates-rise/

https://www.armstrongeconomics.com/international-news/politics/where-to-live-in-the-meltdown/

Additionally the G20 is moving towards a global minimum tax:

https://www.reuters.com/video/2019/06/08/the-g20-is-targeting-tech-titans-tax-hav?videoId=560239835