Steem Crypto Challenge Month #2 : Diving into DeFi. / Un tuffo nella DeFi. [ENG/ITA]

In the world of Bitcoin and other Cryptocurrencies, you never get bored, by now we have got used to the surprising innovations that arise from Blockchain Technology.

I'm talking about Decentralized Finance, the latest speculative phenomenon based on Blockchain clearly at high risk especially because it is in its beginnings in the total absence of brokers and controllers, but this does not mean that in the future it cannot find its place as a valid alternative to traditional financial instruments, becoming a reliable and safe instrument.

But what is DeFi?

DeFi can be defined as the decentralized and automated version of traditional financial instruments, decentralized because it does not need intermediaries, but thanks to smart contracts an agreement is stipulated directly between the parties, automated because Blockchain Technology enforces the agreements through Internet.

DeFi for the most part is built on the Ethereum blockchain network and exchanges are entirely peer-to-peer, i.e. devices connected to each other that acting both as client and server, have equal access to collective resources by archiving and sharing them publicly; therefore the exchanges take place on decentralized platforms that do not belong to anyone, to any company or institution.

But what services does DeFi offer?

As mentioned before, DeFi offers traditional financial services such as trading, payments, loans, wealth management, insurance, through decentralized applications based on blockchain.

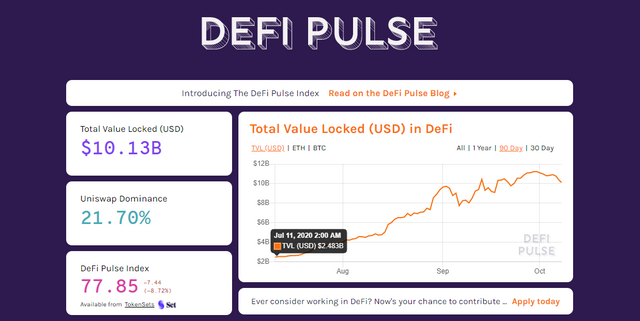

From January to August 2020 the DeFi sector registered a 33.8x growth from 1,425 BTC invested in DeFi projects globally at over 48,000 BTC.

It is not difficult to explain why DeFi's success and its dizzying numbers.

Decentralized Finance is a completely new financial system open to all, not only to those who own large capital as traditional finance requires, in fact it is also called open finance because of its accessibility to individuals with low income thanks to the absence of intermediaries which reduces its costs.

Just as cryptocurrencies make money and payments universally accessible to anyone and anywhere in the world, Decentralized Finance is the alternative to traditional finance accessible to all thanks to an internet connection.

Let's take a concrete example: accessibility to LOANS.

The regulations on which traditional financial and banking institutions are based are now obsolete, rigid and inflexible, often hostile to the needs of people who need liquidity.

Through some DeFi dApps it is possible to take a loan without having to sign piles of forms and the guarantee of payslips, everything is automatically regulated by smart contracts, when the conditions signed by the parties are satisfied.

The only guarantee is the cryptocurrencies deposited on the platform that provides the loan. So if we need liquidity, perhaps to do some shopping or to pay rent but we don't want to release our investments in cryptocurrencies, just use the latter as a guarantee to receive money on loan.

It is clear that this can also be a limit, especially for those who have no cryptocurrency fund, but we are only at the beginning of the dApp revolution, what the future of blocks holds is an unknown but we know very well that its potential is enormous.

What if in the future, perhaps not too far away, we could buy our home by accessing mortgages provided by a dApp?

Is it so unthinkable?

The acts would be registered forever on a reliable and transparent blockchain public register, without the need for intermediaries which would mean cutting the costs associated with them, the basis of the smart contract must be the mutual trust of the interested parties as well as the protection of their privacy and above all a protection system will be required which provides for the automatic transfer of money to the lender in the event of negligence on the part of the debtor.

As they say dreams are desires ..

What about my country?

Although the Central Bank of Italy has not yet given the green light to the Blockchain since it does not fully guarantee efficiency, reliability, security as well as scalability, in the words of Domenico Gammaldi, Senior Director of the Market Supervision service and on the Bank of Italy's Payment System, next November 2020, the Bank of Italy will hold the first conference dedicated to cryptography in Rome.

So something is moving in my country too, albeit slowly but unfortunately this is in the DNA of the older generations of boomers that have heavily influenced the entire Italian political and economic sector and still do not leave room for the new generations more inclined to embrace changes and new technologies.

And the numbers speak for themselves, even we Italians are letting ourselves be conquered by the innovation of the financial sector, especially in the area of payments and investments.

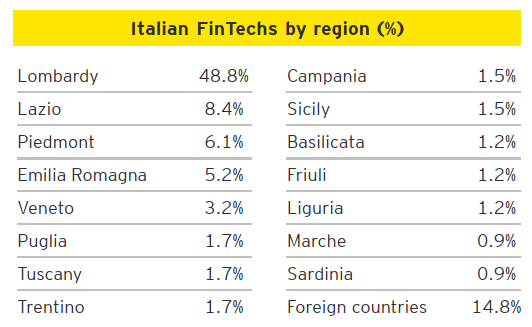

In 2018, about 11 million Italians, and we are talking about 1 in 4 Italians, used at least one fintech service and were satisfied with it: mobile payment services, those for family budget management, P2P transfers and chatbots were more popular.

We are certainly behind other countries in terms of knowledge of Decentralized Finance and its use, but we Italians are also increasingly ready to welcome finance 3.0.

If not, why, according to a 2017 study by the Bank of Italy, had 65% of the major Italian banking institutions already started investing in the Fintech sector in the short term?

From Fintech to Decentralized Finance, the step is ever shorter, soon anyone will become familiar with blockchain-based alternative finance and will be able to become their own bank with their smartphone.

It is not easy to decide for yourself what to invest and how to manage your savings, especially for those who until now have always been used to the presence of intermediaries, banks and financial institutions.

But now the change has begun and fortunately there is no turning back but only proceed in the direction of an increasingly decentralized and liberalized financial system that only in this way it will be able to compete with Decentralized Finance.

The blockchain is offering traditional banking and financial institutions around the world the opportunity to take a technological leap forward, it is only up to them to decide whether to innovate and keep up with the needs of consumers that exactly coincide with the potential of the blockchain, that is:

Transparency, Security, Decentralization, Efficiency and Speed in transactions and above all Easy Access to Credit.

I didn't think I would go into it so much but it's such a broad speech that you cannot cope with with a few pages.

Maybe it need a following with the next post.

In the meantime, thank you for reading my post and see you soon.

With this post I participate in Steem Crypto Challenge Month - Update of Challenge # 2, every week in October we can express our point of view on issues related to the world of crypto currencies.

Read the original post for more information, click here .

- ITALIANO -

Nel mondo di Bitcoin e delle altre cripto valute non ci si annoia mai, oramai ci siamo abituati alle sorprendenti novità che nascono dalla Tecnologia Blockchain.

Sto parlando della Finanza Decentralizzata, l'ultimo fenomeno speculativo basato su Blockchain chiaramente ad alto rischio soprattutto perché è ai suoi inizi nella totale assenza di mediatori e controllori, ma questo non significa che in futuro non possa trovare il suo posto come valida alternativa ai tradizionali strumenti finanziari, diventando uno strumento affidabile e sicuro.

Ma che cosa è la DeFi?

La DeFi può essere definita come la versione decentralizzata e automatizzata degli strumenti finanziari tradizionali, decentralizzata perché non ha bisogno di intermediari, ma grazie ai contratti intelligenti chiamati Smart Contract, viene stipulato un accordo direttamente tra le parti, automatizzato perché attraverso internet la Tecnologia Blockchain rende esecutivi gli accordi.

La DeFi per la maggior parte è costruita sul network della blockchain di Ethereum e gli scambi sono interamente peer-to-peer, cioè dispositivi collegati tra loro che agendo sia da client che da server, accedono alla pari alle risorse collettive archiviandole e condividendole pubblicamente; quindi gli scambi avvengono su piattaforme decentralizzate che non appartengono a nessuno, a nessuna azienda o istituto.

Ma quali servizi offre la DeFi?

Come accennavo prima, la DeFi offre i tradizionali servizi finanziari come trading, pagamenti, prestiti, gestione patrimoniale, assicurazioni, attraverso applicazioni decentralizzate basate su blockchain.

Da gennaio ad agosto 2020 il settore DeFi ha registrato una crescita di 33,8 volte, passando da 1.425 BTC investiti in progetti DeFi a livello globale a oltre 48.000 BTC.

Non è difficile spiegare il perché del successo della DeFi e dei suoi numeri da capogiro.

La Finanza Decentralizzata è un sistema finanziario completamente nuovo e aperto a tutti, non solo a chi possiede grossi capitali come richiede la finanza tradizionale, infatti è chiamata anche open finance proprio per la sua accessibilità a individui con basso reddito grazie all'assenza di intermediari che ne riduce i costi.

Così come le cripto valute rendono il denaro e i pagamenti universalmente accessibili a chiunque e in qualsiasi parte del mondo, la Finanza Decentralizzata è l'alternativa alla finanza tradizionale accessibile a tutti grazie ad una connessione internet.

Facciamo un esempio concreto: l'accessibilità ai prestiti.

I regolamenti su cui si basano gli istituti finanziari e bancari tradizionali sono ormai obsoleti, rigidi e inflessibili spesso ostili alle esigenze delle persone che hanno bisogno di liquidità.

Attraverso alcune dApps DeFi è possibile prendere un prestito senza dover firmare mucchi di moduli e la garanzia delle buste paga, il tutto è regolato automaticamente dagli smart contract, nel momento in cui le condizioni sottoscritte dalle parti siano soddisfatte.

L'unica garanzia sono le cripto valute che si depositano sulla piattaforma che eroga il prestito. Quindi se abbiamo bisogno di liquidità magari per pagare l’affitto o per fare delle spese ma non vogliamo svincolare i nostri investimenti in cripto valute, basta usare quest'ultimi come garanzia per ricevere denaro in prestito.

E' chiaro che ciò può essere anche un limite soprattutto per coloro che non hanno nessun fondo in cripto monete, ma siamo solo agli inizi della rivoluzione delle dApp, cosa ci riserva il futuro dei blocchi è un'incognita ma sappiamo benissimo che le sue potenzialità sono enormi.

E se in futuro, magari neanche troppo lontano, potessimo comprare la nostra casa accedendo a dei mutui erogati da una dApp?

E' così impensabile?

Gli atti sarebbero protocollati per sempre su un registro pubblico blockchain affidabile e trasparente, senza la necessità di intermediari che significherebbe tagliare i costi connessi ad essi, alle base del contratto intelligente dovrà esserci la fiducia reciproca delle parti interessate oltre alla tutela della loro privacy e soprattutto sarà necessario un sistema di protezione che preveda il trasferimento automatico del denaro al prestatore in caso di negligenza da parte del debitore.

Come si dice i sogni son desideri..

Che succede nel mio paese?

Nonostante la Banca Centrale d'Italia non abbia ancora dato semaforo verde alla Blockchain poiché non garantisce pienamente almeno ad oggi l'efficienza, l'affidabilità la sicurezza oltre che la scalabilità, secondo le parole di Domenico Gammaldi, Direttore Superiore del servizio Supervisione sui Mercati e sul Sistema dei Pagamenti della Banca Italia, il prossimo novembre 2020, la Banca d'Italia terrà a Roma il primo convegno dedicato alla crittografia.

Quindi anche nel mio paese qualcosa si sta muovendo, seppur lentamente ma questo purtroppo è nel DNA delle vecchie generazioni di boomer che hanno condizionato pesantemente tutto il settore politico ed economico italiano e ancora non lasciano spazio alle nuove generazioni più inclini ad abbracciare i cambiamenti e le nuove tecnologie.

E i numeri parlano chiaro, anche noi italiani ci stiamo lasciando conquistare dall'innovazione del settore finanziario soprattutto nell'ambito dei pagamenti e degli investimenti.

Nel 2018 circa 11 milioni gli italiani e parliamo di 1 italiano su 4, hanno usato almeno un servizio fintech e ne sono rimasti soddisfatti: servizi di pagamenti mobile, quelli per la gestione del budget familiare, i trasferimenti P2P e i chatbot hanno avuto maggior gradimento.

Staremo anche indietro rispetto ad altri paesi per quanto riguarda la conoscenza della Finanza Decentralizzata e il suo utilizzo, ma anche noi italiani siamo sempre più pronti ad accogliere la finanza 3.0.

Se non fosse così come mai da uno studio del 2017 della Banca d'Italia, il 65% dei maggiori istituti bancari italiani già aveva iniziato ad investire nel breve termine nel comparto Fintech?

Dalla Fintech a Finanza Decentralizzata il passo è sempre più breve, presto chiunque prenderà confidenza con la finanza alternativa basata su blockchain e potrà diventare la banca di se stesso col suo smartphone.

Non è facile decidere da soli su cosa investire e come gestire i propri risparmi, soprattutto per chi fino ad oggi è sempre stato abituato alla presenza di figure intermediarie, banche, istituti finanziari.

Ma ormai il cambiamento è iniziato e per fortuna non si può più tornare indietro ma soltanto procedere nella direzione di un sistema finanziario sempre più decentralizzato e liberalizzato che solo così potrà competere con la Finanza Decentralizzata.

La blockchain sta offrendo agli istituti bancari e finanziari tradizionali di tutto il mondo l'occasione di fare un balzo tecnologico in avanti, spetta solo a loro decidere se innovarsi e stare al passo con i bisogni dei consumatori che coincidono esattamente con le potenzialità della blockchain e cioe è:

Trasparenza, Sicurezza, Decentralizzazione, Efficienza e Velocità nelle transazioni e soprattutto Facilità di Accesso al Credito.

Non pensavo di dilungarmi così tanto ma è un discorso così ampio che non si riesce ad affrontare con poche pagine. Forse ci vuole il continuo col prossimo post.

Nel frattempo vi ringrazio per aver letto il mio post e a presto.

Below you can read my post related to the 1st week topic.

Di seguito puoi leggere il mio post relativo all'argomento della 1° settimana.

They also have options, they can do certain tasks to get a loan. EOS Micro Loan and Flash Loans are two such DeFi projects to address this particular category.

The whole crypto ecosystem is abuzz with DeFi, I think it is that fuel for the mega bull run like 2017. Not financial advice though.

Steem on.

#twopercent #india #affable

I think DeFi holds surprises for us that are still unimaginable for now. The important thing is that it continues to be within everyone's reach.

Thanks for reading my post.😄

Congratulations you are one of the winners of the Steem Crypto Challenge Month...

Thank you for taking part

The Steemit Team

Thank you very much and most of all thank you for organizing this truly inspiring contest and makes us want to participate and get involved on Steemit Platform.

Hope you keep entering.

Still over 20 days and 3 more topics to go !

The Steemit Team

Brava!!tu si che sai scrivere bene!!!

Ci provo.😜😁

Steemit 1st Steps for New Users

https://steemit.com/hive-142140/@punicwax/steemit-1st-steps-for-new-users

Very interesting and useful post.👍

Bravissimissima!

Grazieee.😜