Investment Language 101 Series: TERM OF THE DAY: -- What Is: ' Net Present Value - NPV ' | E.107 | Trading Candle Cheat Sheet Incl. Each Episode.

A series designed to help all the new people flooding into & entering Crypto/Investments daily who get thrown into the rabbit hole so to speak and everything is new to them.

Bitshares 101 Focus/Resources Section for New Crypto Folks now included near the end of each post - starting just prior to Christmas 2017. BTS is a Decentralized Exchange and much more. Very undervalued!

It is a TLDR / Short Form Series, covering ONLY one thing each episode in blue collar, easy to understand language to give a SHORT OVERVIEW of the term or lesson of the day.

It is specifically designed this way to keep it short and simple.

People can then search out extra info if they wish.

I've never seen a regular series or resource running on Steemit to continually address this basic need so I decided to do it.

TERM OF THE DAY:

What is....

' Net Present Value - NPV ' ?

--

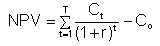

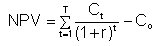

Net Present Value (NPV) is the difference between the present value of cash inflows and the present value of cash outflows over a period of time. NPV is used in capital budgeting to analyze the profitability of a projected investment or project.

The following is the formula for calculating NPV:

Where

Ct = net cash inflow during the period t

Co = total initial investment costs

r = discount rate, and

t = number of time periods

A positive net present value indicates that the projected earnings generated by a project or investment (in present dollars) exceeds the anticipated costs (also in present dollars). Generally, an investment with a positive NPV will be a profitable one and one with a negative NPV will result in a net loss. This concept is the basis for the Net Present Value Rule, which dictates that the only investments that should be made are those with positive NPV values.

When the investment in question is an acquisition or a merger, one might also use the Discounted Cash Flow (DCF) metric.

Apart from the formula itself, net present value can often be calculated using tables, spreadsheets such as Microsoft Excel

--

Breaking Down...

' Net Present Value - NPV ' :

--

Determining the value of a project is challenging because there are different ways to measure the value of future cash flows.

Because of the time value of money (TVM), money in the present is worth more than the same amount in the future. This is both because of earnings that could potentially be made using the money during the intervening time and because of inflation.

In other words, a dollar earned in the future won’t be worth as much as one earned in the present. (Fiat currency)

--

The discount rate element of the NPV formula is a way to account for this. Companies may often have different ways of identifying the discount rate. Common methods for determining the discount rate include using the expected return of other investment choices with a similar level of risk (rates of return investors will expect), or the costs associated with borrowing money needed to finance the project.

For example, if a retail clothing business wants to purchase an existing store, it would first estimate the future cash flows that store would generate, and then discount those cash flows (r) into one lump-sum present value amount of, say $500,000.

If the owner of the store were willing to sell his or her business for less than $500,000, the purchasing company would likely accept the offer as it presents a positive NPV investment. If the owner agreed to sell the store for $300,000, then the investment represents a $200,000 net gain ($500,000 - $300,000) during the calculated investment period. This $200,000, or the net gain of an investment, is called the investment’s intrinsic value.

Conversely, if the owner would not sell for less than $500,000, the purchaser would not buy the store, as the acquisition would present a negative NPV at that time and would, therefore, reduce the overall value of the larger clothing company.

Let's look at how this example fits into the formula above. The lump-sum present value of $500,000 represents the part of the formula between the equal sign and the minus sign. The amount the retail clothing business pays for the store represents Co. Subtract Co from $500,000 to get the NPV: if Co is less than $500,000, the resulting NPV is positive; if Co is more than $500,000, the NPV is negative and is not a profitable investment.

-- Net Present Value Drawbacks and Alternatives:

One primary issue with gauging an investment’s profitability with NPV is that NPV relies heavily upon multiple assumptions and estimates, so there can be substantial room for error. Estimated factors include investment costs, discount rate and projected returns. A project may often require unforeseen expenditures to get off the ground or may require additional expenditure at the project’s end.

Additionally, discount rates and cash inflow estimates may not inherently account for risk associated with the project and may assume the maximum possible cash inflows over an investment period. This may occur as a means of artificially increasing investor confidence. As such, these factors may need to be adjusted to account for unexpected costs or losses or for overly optimistic cash inflow projections.

Payback period is one popular metric that is frequently used as an alternative to net present value. It is much simpler than NPV, mainly gauging the time required after an investment to recoup the initial costs of that investment. Unlike NPV, the payback period (or “payback method”) fails to account for the time value of money. For this reason, payback periods calculated for longer investments have a greater potential for inaccuracy, as they encompass more time during which inflation may occur and skew projected earnings and, thus, the real payback period as well.

Moreover, the payback period is strictly limited to the amount of time required to earn back initial investment costs. As such, it also fails to account for the profitability of an investment after that investment has reached the end of its payback period. It is possible that the investment’s rate of return could subsequently experience a sharp drop, a sharp increase or anything in between. Comparisons of investments’ payback periods, then, will not necessarily yield an accurate portrayal of the profitability of those investments.

-- Net Present Value vs. Internal Rate of Return:

Internal rate of return (IRR) is another metric commonly used as an NPV alternative. Calculations of IRR rely on the same formula as NPV does, except with slight adjustments. IRR calculations assume a neutral NPV (a value of zero) and one instead solves for the discount rate. The discount rate of an investment when NPV is zero is the investment’s IRR, essentially representing the projected rate of growth for that investment. Because IRR is necessarily annual – it refers to projected returns on a yearly basis – it allows for the simplified comparison of a wide variety of types and lengths of investments.

For example, IRR could be used to compare the anticipated profitability of a 3-year investment with that of a 10-year investment because it appears as an annualized figure. If both have an IRR of 18%, then the investments are in certain respects comparable, in spite of the difference in duration. Yet, the same is not true for net present value. Unlike IRR, NPV exists as a single value applying the entirety of a projected investment period.

If the investment period is longer than one year, NPV will not account for the rate of earnings in way allowing for easy comparison. Returning to the previous example, the 10-year investment could have a higher NPV than will the 3-year investment, but this is not necessarily helpful information, as the former is over three times as long as the latter, and there is a substantial amount of investment opportunity in the 7 years' difference between the two investments.

Your Friend in Liberty, Barry.

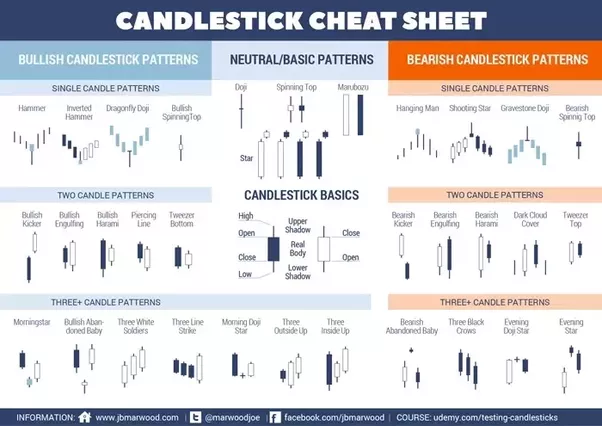

Trading Candle Cheat Sheet:

--

Further Reading/Source/Resources

Friend of the People -- Enemy of the State.

--

Bitshares 101 Focus/Resources Section:

for New Crypto Folks.

https://bitshares.org/

--

-- Bitshares is a Trading platform, and a LOT more.... designed by blockchain wizard here Dan Larimer - @dan / @dantheman.

I've blogged on him, and BTS many many times.

It's a place you can use that is decentralized, with an active community, to use trading lessons like this, that we are learning together.

Just a few of my past $BTS blogs....

to help you apply lessons today!

--

Thanks for reading, have a nice day.

PixaBay has tons of free pictures for us all to use!!!

Super Easy/Fast Picture Edits / Resizing at: http://www.picresize.com/ and also https://www298.lunapic.com/editor/

If you liked this blog post - please Resteem it and share good content with others!

--

Some of my recent blogs:

--

--

Most Images: Gif's - via Giphy.com , Funny or Die.com / Pixabay. Today:

If you feel my posts are undervalued or you want to donate to tip me - I would appreciate it very much.

--

LiteCoin (LTC) - LKdsnvSXk9JW99EiNicFMGKc1FXiBo9tUE

EOS (EOS) - 0xD37bEFf5bf07E3aa432de00cE0AaA8df603A4fB0

Ethereum (ETH) - 0x3Ad69Ff057C9533ca667B2d7E3E557F5eeFd4477

Ethereum Classic (ETC) - 0x5ab2b08d4ce8d454eb9d1ecc65c6d8b0c5f9784c

Bitcoin (BTC) - 18J6RRuzX4V7b2CDbx7tWZYNBLkkGWsvWX

DASH - XgZvsvSZgPkNbmGbRhc3S1Pt2JAc7QHwiS

PIVX - DA3azxQqJiX9t7EviuacpamfNhMi2zGAUh

Stratis (STRAT) - SNsJp6v1jXvKWy4XcXSXfNQ9zhSJJppJgv

ZCash (ZEC) - t1aCPEYELkGaf3GtgGTiCEDo7XfPm4QEwmL

Please note -- I will have limited internet access for awhile -- so PLEASE do not be upset that I cannot reply right away, or to everyone. I am dealing with some changes, and will have limited time online and will be happy if I get a few blog posts up a week.

This has really upset some people but I do not force my opinions on others, or need to communicate every detail of my life or issues, most people do not care anyways. I invested around 10 hours or more a day on Steemit most of my first 13 mths here, trying to build community, put out content and engage people, help and donate to people, and I just do not have that time in my life right now, and that includes for replies and voting/curation.

I have done my best, sorry if you do not understand like some are clearly having a problem with. It's a blogging platform, and I will do my best at everything, and to keep blogging.

Carry On.

A series designed to help all the new people flooding into & entering Crypto/Investments daily who get thrown into the rabbit hole so to speak and everything is new to them.

Bitshares 101 Focus/Resources Section for New Crypto Folks now included near the end of each post - starting just prior to Christmas 2017. BTS is a Decentralized Exchange and much more. Very undervalued!

It is a TLDR / Short Form Series, covering ONLY one thing each episode in blue collar, easy to understand language to give a SHORT OVERVIEW of the term or lesson of the day.

It is specifically designed this way to keep it short and simple.

People can then search out extra info if they wish.

I've never seen a regular series or resource running on Steemit to continually address this basic need so I decided to do it.

TERM OF THE DAY:

What is....

' Net Present Value - NPV ' ?

--

Net Present Value (NPV) is the difference between the present value of cash inflows and the present value of cash outflows over a period of time. NPV is used in capital budgeting to analyze the profitability of a projected investment or project.

The following is the formula for calculating NPV:

Where

Ct = net cash inflow during the period t

Co = total initial investment costs

r = discount rate, and

t = number of time periods

A positive net present value indicates that the projected earnings generated by a project or investment (in present dollars) exceeds the anticipated costs (also in present dollars). Generally, an investment with a positive NPV will be a profitable one and one with a negative NPV will result in a net loss. This concept is the basis for the Net Present Value Rule, which dictates that the only investments that should be made are those with positive NPV values.

When the investment in question is an acquisition or a merger, one might also use the Discounted Cash Flow (DCF) metric.

Apart from the formula itself, net present value can often be calculated using tables, spreadsheets such as Microsoft Excel

--

Breaking Down...

' Net Present Value - NPV ' :

--

Determining the value of a project is challenging because there are different ways to measure the value of future cash flows.

Because of the time value of money (TVM), money in the present is worth more than the same amount in the future. This is both because of earnings that could potentially be made using the money during the intervening time and because of inflation.

In other words, a dollar earned in the future won’t be worth as much as one earned in the present. (Fiat currency)

--

The discount rate element of the NPV formula is a way to account for this. Companies may often have different ways of identifying the discount rate. Common methods for determining the discount rate include using the expected return of other investment choices with a similar level of risk (rates of return investors will expect), or the costs associated with borrowing money needed to finance the project.

For example, if a retail clothing business wants to purchase an existing store, it would first estimate the future cash flows that store would generate, and then discount those cash flows (r) into one lump-sum present value amount of, say $500,000.

If the owner of the store were willing to sell his or her business for less than $500,000, the purchasing company would likely accept the offer as it presents a positive NPV investment. If the owner agreed to sell the store for $300,000, then the investment represents a $200,000 net gain ($500,000 - $300,000) during the calculated investment period. This $200,000, or the net gain of an investment, is called the investment’s intrinsic value.

Conversely, if the owner would not sell for less than $500,000, the purchaser would not buy the store, as the acquisition would present a negative NPV at that time and would, therefore, reduce the overall value of the larger clothing company.

Let's look at how this example fits into the formula above. The lump-sum present value of $500,000 represents the part of the formula between the equal sign and the minus sign. The amount the retail clothing business pays for the store represents Co. Subtract Co from $500,000 to get the NPV: if Co is less than $500,000, the resulting NPV is positive; if Co is more than $500,000, the NPV is negative and is not a profitable investment.

-- Net Present Value Drawbacks and Alternatives:

One primary issue with gauging an investment’s profitability with NPV is that NPV relies heavily upon multiple assumptions and estimates, so there can be substantial room for error. Estimated factors include investment costs, discount rate and projected returns. A project may often require unforeseen expenditures to get off the ground or may require additional expenditure at the project’s end.

Additionally, discount rates and cash inflow estimates may not inherently account for risk associated with the project and may assume the maximum possible cash inflows over an investment period. This may occur as a means of artificially increasing investor confidence. As such, these factors may need to be adjusted to account for unexpected costs or losses or for overly optimistic cash inflow projections.

Payback period is one popular metric that is frequently used as an alternative to net present value. It is much simpler than NPV, mainly gauging the time required after an investment to recoup the initial costs of that investment. Unlike NPV, the payback period (or “payback method”) fails to account for the time value of money. For this reason, payback periods calculated for longer investments have a greater potential for inaccuracy, as they encompass more time during which inflation may occur and skew projected earnings and, thus, the real payback period as well.

Moreover, the payback period is strictly limited to the amount of time required to earn back initial investment costs. As such, it also fails to account for the profitability of an investment after that investment has reached the end of its payback period. It is possible that the investment’s rate of return could subsequently experience a sharp drop, a sharp increase or anything in between. Comparisons of investments’ payback periods, then, will not necessarily yield an accurate portrayal of the profitability of those investments.

-- Net Present Value vs. Internal Rate of Return:

Internal rate of return (IRR) is another metric commonly used as an NPV alternative. Calculations of IRR rely on the same formula as NPV does, except with slight adjustments. IRR calculations assume a neutral NPV (a value of zero) and one instead solves for the discount rate. The discount rate of an investment when NPV is zero is the investment’s IRR, essentially representing the projected rate of growth for that investment. Because IRR is necessarily annual – it refers to projected returns on a yearly basis – it allows for the simplified comparison of a wide variety of types and lengths of investments.

For example, IRR could be used to compare the anticipated profitability of a 3-year investment with that of a 10-year investment because it appears as an annualized figure. If both have an IRR of 18%, then the investments are in certain respects comparable, in spite of the difference in duration. Yet, the same is not true for net present value. Unlike IRR, NPV exists as a single value applying the entirety of a projected investment period.

If the investment period is longer than one year, NPV will not account for the rate of earnings in way allowing for easy comparison. Returning to the previous example, the 10-year investment could have a higher NPV than will the 3-year investment, but this is not necessarily helpful information, as the former is over three times as long as the latter, and there is a substantial amount of investment opportunity in the 7 years' difference between the two investments.

Your Friend in Liberty, Barry.

Trading Candle Cheat Sheet:

--

Further Reading/Source/Resources

Friend of the People -- Enemy of the State.

--

Bitshares 101 Focus/Resources Section:

for New Crypto Folks.

https://bitshares.org/

--

-- Bitshares is a Trading platform, and a LOT more.... designed by blockchain wizard here Dan Larimer - @dan / @dantheman.

I've blogged on him, and BTS many many times.

It's a place you can use that is decentralized, with an active community, to use trading lessons like this, that we are learning together.

Just a few of my past $BTS blogs....

to help you apply lessons today!

--

Thanks for reading, have a nice day.

PixaBay has tons of free pictures for us all to use!!!

Super Easy/Fast Picture Edits / Resizing at: http://www.picresize.com/ and also https://www298.lunapic.com/editor/

If you liked this blog post - please Resteem it and share good content with others!

--

Some of my recent blogs:

--

--

Most Images: Gif's - via Giphy.com , Funny or Die.com / Pixabay. Today:

If you feel my posts are undervalued or you want to donate to tip me - I would appreciate it very much.

--

LiteCoin (LTC) - LKdsnvSXk9JW99EiNicFMGKc1FXiBo9tUE

EOS (EOS) - 0xD37bEFf5bf07E3aa432de00cE0AaA8df603A4fB0

Ethereum (ETH) - 0x3Ad69Ff057C9533ca667B2d7E3E557F5eeFd4477

Ethereum Classic (ETC) - 0x5ab2b08d4ce8d454eb9d1ecc65c6d8b0c5f9784c

Bitcoin (BTC) - 18J6RRuzX4V7b2CDbx7tWZYNBLkkGWsvWX

DASH - XgZvsvSZgPkNbmGbRhc3S1Pt2JAc7QHwiS

PIVX - DA3azxQqJiX9t7EviuacpamfNhMi2zGAUh

Stratis (STRAT) - SNsJp6v1jXvKWy4XcXSXfNQ9zhSJJppJgv

ZCash (ZEC) - t1aCPEYELkGaf3GtgGTiCEDo7XfPm4QEwmL

Please note -- I will have limited internet access for awhile -- so PLEASE do not be upset that I cannot reply right away, or to everyone. I am dealing with some changes, and will have limited time online and will be happy if I get a few blog posts up a week.

This has really upset some people but I do not force my opinions on others, or need to communicate every detail of my life or issues, most people do not care anyways. I invested around 10 hours or more a day on Steemit most of my first 13 mths here, trying to build community, put out content and engage people, help and donate to people, and I just do not have that time in my life right now, and that includes for replies and voting/curation.

I have done my best, sorry if you do not understand like some are clearly having a problem with. It's a blogging platform, and I will do my best at everything, and to keep blogging.

Carry On.

--

LiteCoin (LTC) - LKdsnvSXk9JW99EiNicFMGKc1FXiBo9tUE

EOS (EOS) - 0xD37bEFf5bf07E3aa432de00cE0AaA8df603A4fB0

Ethereum (ETH) - 0x3Ad69Ff057C9533ca667B2d7E3E557F5eeFd4477

Ethereum Classic (ETC) - 0x5ab2b08d4ce8d454eb9d1ecc65c6d8b0c5f9784c

Bitcoin (BTC) - 18J6RRuzX4V7b2CDbx7tWZYNBLkkGWsvWX

DASH - XgZvsvSZgPkNbmGbRhc3S1Pt2JAc7QHwiS

PIVX - DA3azxQqJiX9t7EviuacpamfNhMi2zGAUh

Stratis (STRAT) - SNsJp6v1jXvKWy4XcXSXfNQ9zhSJJppJgv

ZCash (ZEC) - t1aCPEYELkGaf3GtgGTiCEDo7XfPm4QEwmL

Please note -- I will have limited internet access for awhile -- so PLEASE do not be upset that I cannot reply right away, or to everyone. I am dealing with some changes, and will have limited time online and will be happy if I get a few blog posts up a week.

This has really upset some people but I do not force my opinions on others, or need to communicate every detail of my life or issues, most people do not care anyways. I invested around 10 hours or more a day on Steemit most of my first 13 mths here, trying to build community, put out content and engage people, help and donate to people, and I just do not have that time in my life right now, and that includes for replies and voting/curation.

I have done my best, sorry if you do not understand like some are clearly having a problem with. It's a blogging platform, and I will do my best at everything, and to keep blogging.

Carry On.

Excellent information. I am not an expert in economics but it has helped me to understand more about this field.

As for your phrase "friend of the people, enemy of the state" you are right and I support you in that.

It is unfair that a small group manages all the riches of the world causing enormous inequality. This in turn brings poverty, unemployment, lack of education, etc.

The cryptocurrencies are the alternative and through them this fiduciary system will be ended.

Thanks for your post, they really are of great help.

Thank you for the knowledge and the lesson may be useful for us all

Tr eyshob bal borbe k?

although I do not like maths, but I will learn this formula by heart

The biggest disadvantage to the calculation of NPV is its sensitivity to discount rates. After all, NPV computations are really just a summation of multiple discounted cash flows - both positive and negative - converted into present value terms for the same point in time (usually when the cash flows begin). As such, the discount rate used in the denominators of each present value (PV) computation is critical in determining what the final NPV number will turn out to be. A small increase or decrease in the discount rate will have a considerable effect on the final output.

Let's say you were trying to value an investment that would cost you $4,000 up front today, but was expected to pay you $1,000 in annual profits for five years (for a total nominal amount of $5,000), beginning at the end of this year. If you use a 5% discount rate in your NPV calculation, your five $1,000 payments are equal to $4,329.48 of today's dollars. Subtracting the $4,000 initial payment, you are left with an NPV of $329.28. (To learn more about calculating NPV, see Understanding The Time Value Of Money and Anything But Ordinary: Calculating The Present And Future Value Of Annuities.)

However, if you raise the discount rate from 5% to 10%, you get a very different NPV result. At a 10% discount rate, your investment's cash flows add up to a present value of $3,790.79. Subtract the $4,000 initial cost from this amount, and you're left with a negative NPV of $209.21. Simply by adjusting the rate, you have gone from having an investment that creates $329.28 of value to having one that destroys $209.21 instead.

Of course, you'll want to undertake the investment if 5% is the correct rate to use, and reject it if 10% is the correct rate. But how do you know which discount rate to use? Accurately pegging a percentage number to an investment to represent its risk premium is hardly an exact science. If the investment is very safe, with low risk of loss, 5% may be a reasonable discount rate to use, but what if the investment harbors enough risk to warrant a 10% discount rate? Bottom line, since NPV calculations require a discount rate, there is no way to get around this issue; therefore, it is a big disadvantage to the NPV methodology.

Making matters even more complex is the possibility that your investment won't have the same level of risk throughout its entire time horizon. In our example of a five-year investment, how would you handle a situation in which the investment had high risk of loss for the first year, but relatively low risk for the last four? You can try to use different discount rates for each time period, but this will make your model even more complex and require a lot on your part to peg not only one discount rate accurately, but five. This is another disadvantage to using the NPV model.

Finally, another major disadvantage to using NPV as an investment criterion is that it wholly excludes the value of any real options that may exist within the investment. Consider again our five-year investment example - suppose this is a startup technology company, which is currently losing money but is expected to have the opportunity to expand greatly in three years' time. If you know the company has this valuable real option of expansion in the future, shouldn't you incorporate the value of that option into the total NPV of the investment? Clearly, the answer is "yes", but the standard NPV formula provides no way to include the value of real options. (For further reading, see An Introduction To Real Options.)

Thus, NPV is a useful starting point to value investments, but certainly not a definitive answer that an investor can rely on for all investment decisions.

This is very useful information

Awesome

Very first reader you!!

Nice post,true talk. Are you a mathematician

https://busy.org/@rizvy/good-night-all

What does this comment have to do with my post?????