The Valuation of Key ASX-Listed Gold Mining Companies by Operating Performance, Reserves and Resources

(This report is not to be considered as professional investment advice. Please do your own research.)

Summary

Analysing 21 ASX-listed gold mining companies, I consider the relative value of these companies using a variety of production, operation and reserves/resources metrics using the closing price at 14th June 2018. In particular, I introduce a new approach to valuing by adjusting the production volume by all-in sustaining cost (AISC) and this metric does highlight better which companies are of better value by factoring in operational efficiency.

The analysis shows that the market appears to prefer gold miners with higher production volume, production margin and lower AISC, in that order. The ore reserves and mineral resources are not significant factors in the pricing at this stage, perhaps due to the low level of interest from the market that sees more exciting opportunities in other sectors and industries.

Based on the results, I believe that the valuation should be considered on a shorter term basis and a longer term basis. The shorter term basis would place more weight on the AISC-adjusted annualised production metric, and the longer term basis would place more weight on the ore reserves and mineral resources. Thus, on a shorter term basis, the most undervalued miners would be Oceanagold, Ramelius and Silver Lake. On a longer term basis, the most undervalued miners would be Blackhams, Westgold, Perseus and Beadell. However, Red5, Perseus, Resolute, Westgold and Blackhams provide wildcard opportunities as long as they are able to show the market they can increase their production volume and stabilise their production costs.

Approach

21 ASX-listed gold mining companies are analysed based on their valuation relative to their operating performance, production, reserves and resources. In determining the company’s value, we use the enterprise value is used instead of market capitalisation as it also includes the company’s cash and debt, reflecting better the total capital that is used to fund the company’s operations and its underground resources/reserves.

Companies are divided into five broad categories defined by their annual production – major, large, mid-tier, junior and mini. A major mining company is one that produces at least 1.5Moz p.a., a large mining company 500 000-1.5Moz p.a., a mid-tier mining over 150 000-500 000oz p.a., a junior mining over 50 000-150 000oz p.a. and a mini is one that mines less than 50 000oz p.a. This categorical approach can vary with different people.

The production margin, annualised production and AISC-adjusted annualised production are metrics used for operating performance. The production margin is defined as the difference between the realised gold price and the AISC, approximating the margin between what the mining company receives for selling their gold and the cash cost on extracting the gold. The annualised production is straightforward. The AISC-adjusted annualised production is a metric I have developed to take into account the cost of production. This metric is simply the annualised production divided by the AISC divided by 1 000, so if a miner produces 144 000oz p.a. at AISC of $1 200/oz would have an AISC-adjusted annualised production of 120 000oz. If the AISC is $800/oz, then the metric gives 180 000oz. The advantage of this metric is to differentiate between gold miners that deliver higher volume but lower grades (usually implies costlier production) and one with similar volume but higher grades (thus, likely lower cost production). Clearly a lower cost miner is preferable and hence the market should ascribe higher value to it. This metric will incorporate this into the valuation to help guide investors in identifying undervalued mining companies more effectively.

Company Sample and Overview

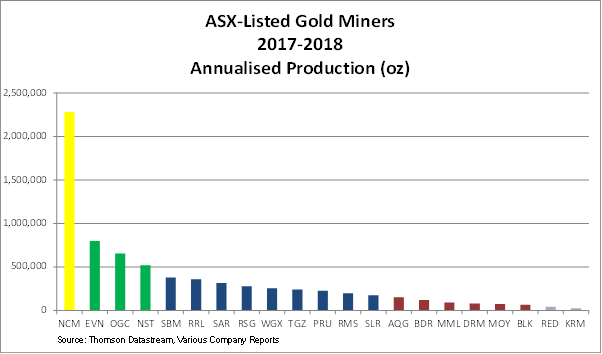

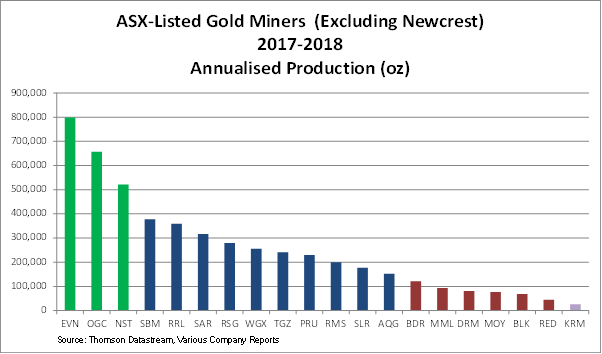

The 21 companies included in the analysis are given in the chart below, categorised by their annualised production for the year based on the production from the last three quarters. The major miner, Newcrest (NCM), is in yellow, large miners are in green, mid-tiers are in dark blue, juniors in red and the mini miner, Kingsrose (KRM), is in purple. Note that other ASX-listed gold mining companies exist, especially in the junior and mini categories.

As we can see, Newcrest Mining (NCM) is a major gold mining company with production that dwarves the other ASX-listed mining companies. ASX-listed gold miners tend to predominantly be mid-tiers and junior mining companies with annual production between 80 000-400 000oz.

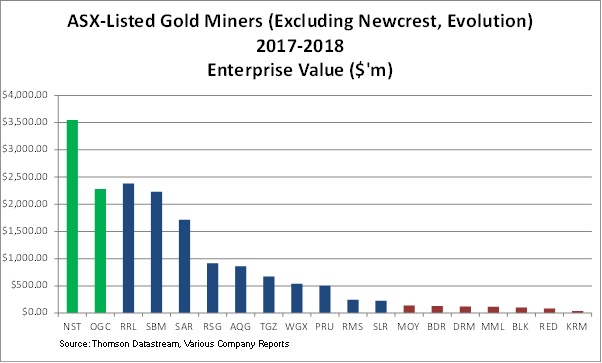

The enterprise value of these companies (excluding Newcrest Mining (NCM) that has an EV of $17.6 billion and Evolution Mining (EVN) with EV of $6.1 billion as at 14th June 2018) is given in the figure below:

The figure shows that the market investors seem to determine the value of the gold miners by their categories. We also recognise that Regis (RRL), St Barbara (SBM) and Saracen (SAR) appear to have been re-rated and their EV are in the same league as Oceanagold, though not quite in the league with the large gold miners such as Evolution (EVN) and Northern Star (NST). Ramelius (RMS) and Silver Lake (SLR) are marginally classified as mid-tiers, though the market prices them more like they are junior miners.

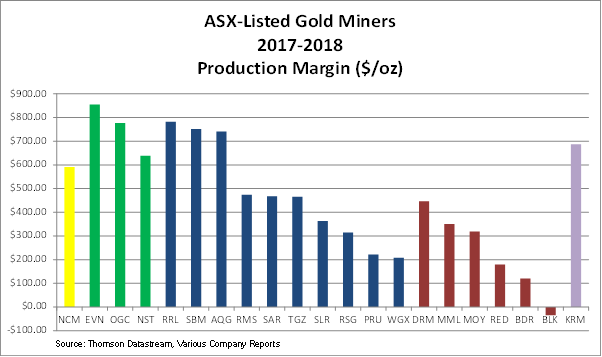

The current operating performance, reflected by the production margin, is given in the figure below:

The production margin is broadly correlated with the size of the mining company as there is economies of scale. Exceptions do exist, most notably that Kingsrose (KRM) has a substantially high production margin. However, this is due to the mining company’s significant turnaround since it was recapitalised mid last year. The market has not yet taken this into account as reflected by the EV. The trend here shows that EV is somewhat driven by the production margin, although Ramelius (RMS) appears to be priced cheaply relative to their production level. For Newcrest (NCM), the production margin is less than all the large mining companies and the best three mid-tier mining companies, as well as Kingsrose. For Doray (DRM), the closure of the Andy Well mine has caused investors to have little confidence in their company. For Ramelius, the 50% decline in the stock price last year shook investors sharply and they are only warming to the recent acquisition of the Edna May mine that is expected to deliver 100 000oz p.a. for four years. Blackhams (BLK) is the only mining company with negative production margin owing to the September 2017 and December 2017 quarters, although I note that Red5 (RED) and Westgold (WGX) reported high AISC in the most recent quarter, at $1 815/oz and $1 705/oz, respectively.

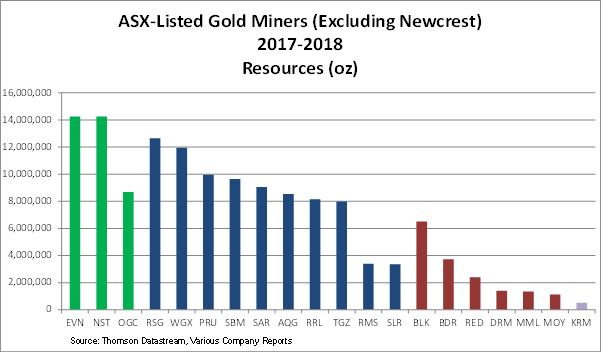

The longer term profitability and sustainability of the companies, as reflected by their ore reserves (economic reserves beneath the ground at current prices) and mineral resources (deposits underground that can be extracted), are given in the figures below. Newcrest (NCM) has been excluded to avoid distortion. Their ore reserves is currently 64.9Moz and mineral reserves is 129Moz:

The figure here suggests that the market does not classify the mining companies so much by their reserves and resources, since there are miners we classify as one group with similar reserves and resources as miners in another group. Evolution (EVN) has expanded substantially in 2015-2016, turning itself from being a mid-tier miner to being a large miner with 7 producing mines. They are undertaking substantial exploration and the Ernest Henry mine will catapult them even higher. Northern Star (NST) has lower reserves as they are more interested in acquiring mines rather than building them. I have also adjusted their reserves and resources for the acquisition of South Kalgoorlie Operations from Westgold (WGX). With Oceanagold (OGC), it is interesting to note that they have lower resources than Northern Star (NST) but more reserves. This is due to substantial silver reserves in their Didipio and Waihi mines.

Resolute (RSG) and Westgold (WGX) have large reserves and resources, but their production is substantially lower, but they are in the process of developing their existing mines to increase production. Regis (RRL) is in the middle of the mid-tiers, but they are in the process of developing their McPhillamys mine and possibly upgrading themselves to be a large miner.

St Barbara (SBM) has finally seen the worst in 2014 when their Gold Ridge and Simberi mines were burning cash and almost off-set their Gwalia mine, which is one of the highest grade and lowest cost gold mine in Australia. They are now generating substantial cash each quarter, and they may expand their reserves and resources with strategic acquisitions if they want.

With Ramelius (RMS) and Silver Lake (SLR), they may need to consider acquiring mines or developing their existing properties as they are substantially behind their group. Fortunately, they have sufficient cash reserves and are generating positive operating cash flows so this may be something to watch for.

Teranga (US:TGCDF) purchased Gryphon Minerals last year and are now in the late stage development of the Wahgnion Project, with production hopefully in the next 18 months.

Perseus (PRU) has engaged in aggressive acquisition but they have been plagued with unstable operations at their Edikan mine. At least 30% of their large resources is in the Yaoure project, acquired in 2016, that still needs funding before they can develop further.

Of substantial interest is also Alacer (AQG), with their development of a world class Copler mine. Their production is currently at the bottom end of the mid-tier but they have spent almost $600m expanding their mine. With low production cost and the financing already in place, they will be eventually heading towards becoming a large mine. Their current EV at $860m shows the market is anticipating this to happen soon.

In the junior mining group, the results are not as evident when looking at the figures only. Blackhams (BLK) has the highest reserves and resources by far, placing them comfortably in the mid-tier group. However, poor operations and near financial distress in the past two years have led them to raise equity and dilute shareholdings. Millennium (MOY) is replacing their reserves and resources and it is still growing organically without needing to raise equity or borrow. Beadells (BDR) is also in a similar situation as Blackhams (BLK) in that their larger reserves and resources are not being utilised due to operation and financial troubles. They have raised equity and debt to expand their current operations, with the potential in the medium term of increasing their production to over 200 000oz p.a.

Red5 (RED) recently acquired both the Darlot and King of the Hills mines, allowing them to resume production after the Siana mine in the Philippines was closed under government order. Their reserves and resources in the Australian mines are still subject to further increases, as the board is expecting to invest into exploration.

Kingsrose (KRM) has been spending more on fixing their waterlogged Talang Santo mine and will expand their Way Linggo mine. Both mines have high gold and silver grades that are mouthwatering by Australian mine standards. However, I believe the infrastructure is more underdeveloped in Indonesia, hence the high costs and unreliable operations.

Valuation Analysis

I now consider the relative value of the 21 companies using their EV against the annualised production, AISC-adjusted annualised production, AISC-adjusted projected production (based on management forecasts), reserves and resources. The production-based valuation metrics reflect more the short to medium term value while the longer term value is reflected by the reserves and resources. I discuss limitations in my valuation approach in the next section.

The annualised production is commonly used as a valuation basis. The EV/annualised production is given in the figure below:

The metric here shows that major and large miners are being priced at around $6 000+/oz, the mid-tiers are priced at around $2 000-5 000/oz, the juniors and mini companies are priced at around $1 000-2 000/oz. Anything outside of that range may suggest the mining company (defined by their annualised production) is overvalued or undervalued, or alternatively may be waiting to be re-rated because of changes expected to occur in a short time. Thus, Oceanagold appears to not be recognised as a large company but a mid-tier, despite its production being over 500 000oz p.a. and likely to expand further their operations with the Haile mine producing last year. Similarly, Regis, St Barbara, Alacer and Saracen are being perceived by the market as being potentially large miners in the near future. Silver Lake and Ramelius are being priced as if they are junior miners but this is also reasonable since they are not yet expected to consistently deliver 200 000+oz p.a. Perseus and Westgold are currently undervalued due to a combination of operating problems and expensive development programs. The production of Perseus’ Sissingue mine in the March quarter is still being evaluated by the market to see if it has taken the company out of its miserable checkered past. With Resolute, the reduction in their 2018 financial year production has been factored in by the market.

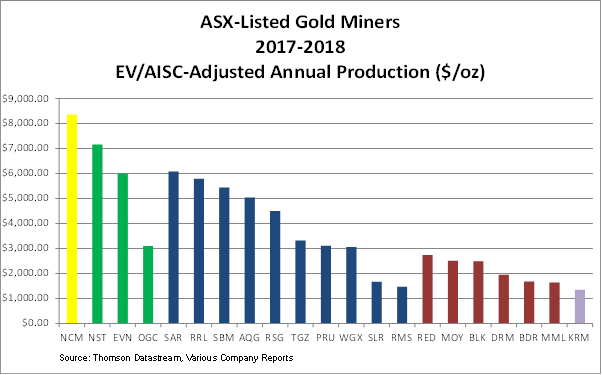

Markets value mining companies not only by their production volume but their efficiency. This efficiency can be seen in the production cost. Thus, I have decided to adjust the valuation metric to take this into account using the EV/AISC-adjusted annualised production. So, let us also look at the valuation using the EV/AISC-adjusted annualised production and see the difference:

When adjusted for the AISC, we see that Newcrest has a richer valuation while Evolution has become cheaper than Northern Star as Evolution has been delivering lower cost gold ounces. Oceanagold stands more forlorn among its group, and even among mid-tiers, as lagging behind in its valuation relative to its production. Oceanagold has delivered consistently low cost ounces due to Didipio being a significant copper mine so allows for production credits that offset the cost of producing gold and silver.

Among the mid-tiers, Saracen is slightly higher cost than Regis, St Barbara and Alacer, so it is the most richly valued gold miner of the group. That being said, Saracen is not overvalued by any measure since they have been growing their production significantly over the past two years. St Barbara has seen a stellar run since early 2015 when their Gold Ridge mine was handed over to the Solomon Islands government, thus jettisoning one of their albatrosses. Regis is fairly valued at this level as it is recognised as one of the most reliable low cost gold miners on the ASX. Resolute’s value is higher when adjusted by AISC due to their higher cost from their Syama Sulphide development project and Ravenswood expansion as well. With Teranga, the valuation appears to be more towards the lower side given the mining cost is of a moderate level. I expect that this will improve as Teranga increases their production when their Wahgnion project starts producing. The higher costs of Perseus and Westgold are reflected in this valuation metric as their EV/production metric increase 50% from the low $2 000 range to low $3 000 range. Silver Lake and Ramelius are valued more closely to the junior miners even under this measure. Perhaps the market is waiting to see their production level for the next few quarters to ascertain that they have graduated out of the junior miner group before re-rating them.

For the junior miners, this metric leads to greater differences in the way the miners are ranked. At this level of production, the economies of scale are starting to take effect so the cost of production is more volatile. Under this measure, Red5 and Millennium swapped places so Red5 is the most richly valued in the group, Blackhams leads over Doray while Beadell inches ahead of Medusa. Since the production volumes of these junior miners are quite similar, their AISC counts. Medusa is the most reliable in this group in terms of the AISC, although Doray is the lowest judging by the last three quarters.

Kingsrose is an interesting case as it has seen production volume reduce, albeit a low volume in the first place. They deliver these ounces at low cost although they did produce over ounces at over $2 000/oz in some quarters last year. Thus, the valuation metric for Kingsrose may point to undervaluation but the market has placed a substantial risk premium because at such production volume, AISC could swing higher all of a sudden.

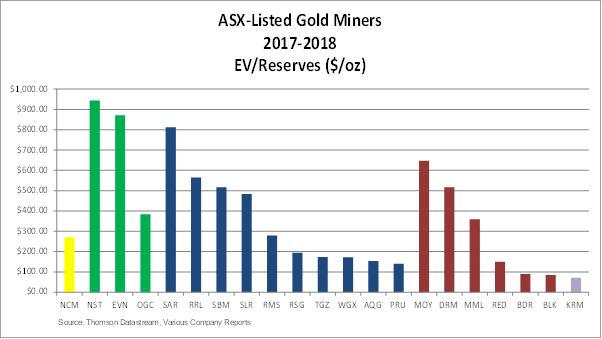

To measure the longer term growth and profitability potential, we consider the valuation based on ore reserves and mineral resources. The EV/Reserves is given in the figure below:

Based on this measure, Newcrest is significantly undervalued as it has 64.9Moz of reserves and its EV is $17.6 billion. Investors do not appear to give much weight on valuing major gold mining companies based on ore reserves. This is different in the case of the large and mid-tier gold miners where Northern Star, Evolution, Saracen are being valued at $800+/oz reserves. The reason could well be due to the consistently low cost ounces being produced by these mining companies and also the market expects or have priced in their acquisitions of other mines to expand their base.

Northern Star grew its ore reserves over ten-fold since 2013 through strategic acquisitions of the Jundee, East Kalgoorlie Joint Venture and South Kalgoorlie mines, while Evolution has expanded itself significantly since 2014 through multiple mine purchases. Saracen has risen rapidly through its expansion of its Thunderbox and Carosue Dam mines and they have proven to be low cost mines.

Regis and St Barbara both have over 4Moz of reserves but owing to their ability to generate $150 million in net operating cash each year, the market has priced them richly. Should they both make acquisitions of mine projects to add to their reserve base, this can lead to their valuation falling to being on par with their peers.

Oceanagold has a substantial ~6Moz of reserves, with potential to further expand this with their Haile and Waihi mines. The market appears to be undervaluing them on its reserves, perhaps due to the volatile environment of the Philippines and its significant debt level of $300+ million. The mines they own have relatively higher capital expenditure, thus leading to the market being slower to warm to them despite their annual production exceeding 0.5Moz.

Silver Lake is priced quite richly relative to its reserves as they currently have less than 0.5Moz reserves. They also have almost $80 million in cash with no debt, so they may benefit from making an acquisition of a small scale mine or a late stage development project to add their reserves and bring it to production.

Ramelius has close to 0.9Moz in reserves, with its purchase of the Edna May mine late last year. They are also working to expand their high grade Vivien mine and expand their flagship Mount Magnet mine. I have not factored a 100 000oz increase in resources and approximately 29 000oz increase in reserves as announced on 6th June 2018.

Resolute has a large 4.7Moz of ore reserves, with significant expansion in around August 2018 when they update their Ore Reserves Statement given the Syama Underground Development and Ravenswood expansion projects. These projects have consumed almost $150 million in cash and investors have been unhappy about this as production has reduced and AISC has risen.

Teranga has almost 3.9Moz of ore reserves and they are expected to grow further as the Wahgnion project is developed further. The valuation has substantially improved since the beginning of this year when the stock price was less than 50% of the current price. They are still at the stage of investing substantial cash to develop their projects, so the market is still pricing it more conservatively.

Westgold has 3.13Moz of ore reserves, down from almost 3.6Moz with the sale of the South Kalgoorlie Operations to Northern Star. Westgold has been priced below the peer average owing to unstable production and substantial cash investment on their Central Murchison Gold Mine and the Fortnum mine that has commenced production in the March quarter. I believe that Westgold is now undervalued but substantial risk remains, hence the discount.

Alacer is an interesting case as it currently has 5.6Moz of reserves, with over 4Moz in the Copler mine alone. The valuation is low as their annual production makes them a marginal mid-tier miner. I believe this company is undervalued based on the reserves as the market is waiting to confirm their Copler mine expansion will convert to much higher annual production.

Perseus has 3.6Moz of ore reserves, and is expected to see this rise as the Yaoure project is developed. However, their ore reserves have not converted too well into cash, with the Edikan mine delivering highly variable volume at similarly variable efficiency.

Millennium has the lowest ore reserves in this entire sample, with 0.22Moz. However, credit should be given in that they increased their reserves from the 2017 financial year after depletion from mining. They are in the process of aggressively exploring and developing the Nullagine underground mine, with some good grades coming through. The market appears to look upon them favourably and hence have priced it accordingly.

Doray is in the process of recovering from a nightmarish drop from mid-2016 to late last year, culminating with the Andy Well mine being placed on care and maintenance due to high cost and low gold prices. The Deflector gold mine has been a shining star, delivering lower cost ounces, with some excellent gold intercepts being reported regularly. The market anticipates that Doray will increase its ore reserves by August 2018. They currently have 259 000oz of reserves, having written off the Andy Well reserves.

Medusa has small reserves of 327 000oz while their production and lower cost have been seen favourably by the market. With increasing cash reserves, albeit from a low base, they may be able to engage in a more focused exploration program to convert more resources into reserves.

Red5 has expanded their ore reserves substantially after purchasing the Darlot and King of the Hills mines and making significant progress in converting resources into reserves. The two Australian mines now have in excess of 1Moz of resources. With some luck, the Siana mine may commence production. They also are looking to developing their underground mine at Siana. This could be a company to keep an eye out for in the medium term.

Beadell has a large reserve of almost 1.5Moz, the largest in the peer group. They have conducted a large expansion program on their Tucano mine. However, that came at a high price as the Tucano mine delivered lacklustre results and the company falling into substantial debt and declining cash reserves.

Blackhams is the least valuable junior gold miner when measured by its ore reserves, which they report at 1.2Moz. The Wiluna-Matilda mine has been a headache for the company, having experienced low gold grades, high costs and delays in operations. So, despite a relatively high reserve for a junior miner, doubts exist as to whether these reserves will eventually be converted into cashflow.

Finally, Kingsrose does not report reserves, but their high grades of resources with almost 9g/t of gold and 54g/t of silver, I believe that it would be economically viable to mine. However, it is stretching the long bow given their high operating costs over 2015-2016 that led to them needing to be recapitalised to pay off their existing debt. But the worst may be behind them, let’s hope!

Before moving to the next section, the EV/Reserves metric can be compared against the production margin. The EV/Reserves can reflect the market’s evaluation of the future profitability on what is below the ground while the production margin shows the realised profitability of extracting the ore.

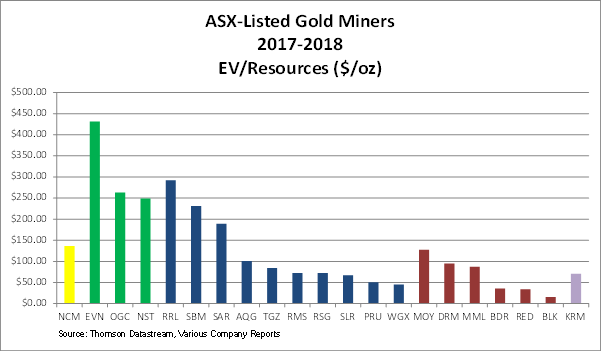

The valuation based on mineral resources is given in the figure below:

Newcrest appears undervalued by resources, similar to its value relative to its reserves. They have 129Moz of resources! However, Newcrest has written off over 15Moz of resources in the past two years, so it is very much far from being certain that their resources can turn into cash in the future.

For the large gold miners, Evolution and Oceanagold are valued more richly than Northern Star as Northern Star has over 14Moz after purchasing the South Kalgoorlie Operations. Evolution has over 14Moz as well while Oceanagold has less than 9Moz.

Among the mid-tiers, Resolute has the highest resources at almost 12.7Moz, followed by Westgold at 11.9Moz, Perseus at 9.9Moz, St Barbara at 9.6Moz, Saracen at 9.1Moz, Alacer at 8.5Moz, Regis at almost 8.2Moz, Teranga at almost 8Moz, Ramelius at 3.4Moz and Silver Lake also at almost 3.4Moz. Mid-tiers that are delivering over 300 000oz p.a. for the 2018 financial year are priced higher than the others. Note that Resolute is expected to deliver only 280 000oz for 2018, down markedly from 329 834oz last year. Perseus and Westgold are looking undervalued in this metric due to their large resources, but again the question remains on whether these resources will be convertible into cash, and how long?

For the junior miners, Blackhams has the highest at 6.5Moz, Beadell at 3.7Moz, Red5 at almost 2.4Moz, Doray at 1.4Moz, Medusa at 1.3Moz and Millennium at 1.1Moz. Again, the valuation appears to be favoured towards companies that are delivering lower cost ounces and higher volume. However, Millennium is the most richly valued among the junior miners as it the least mineral resources of the group. In fact, the valuation metric is almost inversely correlated with the resources of the companies in this group with Beadell and Red5 swapping places. The reason for this is since these junior miners have had a mixed history of production volume and costs, leaving investors unsure about holding them for a longer term.

Finally, Kingsrose is priced at just above $70/oz resources, which is low but this is because it is a mini gold miner and they are still largely neglected by the market given its past three years.

Based on this valuation metric, the following companies are being priced as being “dirt-cheap” (pun intended) – Blackhams ($15.61), Red5 ($34.37), Beadell ($35.59), Westgold ($45.27) and Perseus ($50.77).

Conclusion

The valuation shows the market ascribes premiums on pricing for mining companies by production volume, production margin and also lower AISC, in that order. Major and large companies can be priced at above $6 000/oz production adjusted for AISC, mid-tiers between $3 000-5 000/oz, juniors between $1 000-2 000/oz and minis are below $1 000/oz. The better quality miners are being priced at over $500/oz reserve and the poorer quality ones below $200/oz. If one can find well-run gold mines below these ranges, it may be rewarding.

Based on the results, I believe that the valuation should be considered on a shorter term basis and a longer term basis. The shorter term basis would place more weight on the AISC-adjusted annualised production metric, and the longer term basis would place more weight on the ore reserves and mineral resources. Thus, on a shorter term basis, the most undervalued miners would be Oceanagold, Ramelius and Silver Lake. On a longer term basis, the most undervalued miners would be Blackhams, Westgold, Perseus and Beadell.

Disclaimer

The author holds at least 50% of the stocks mentioned in this article, with a larger holding on the mid-tiers and juniors. The author does not receive any commission or payments from the companies mentioned.

You should join @investorsclub, this is the type of stuff that is shared.

Thanks mate! And so glad you dropped by...

Will join the club and over time contribute more to this forum. I will soon be collecting data on US and TSX precious metals mining companies so there will be more coming in time!

Congratulations @sydneycontrarian! You have completed some achievement on Steemit and have been rewarded with new badge(s) :

Click on the badge to view your Board of Honor.

If you no longer want to receive notifications, reply to this comment with the word

STOPDo not miss the last post from @steemitboard!

Participate in the SteemitBoard World Cup Contest!

Collect World Cup badges and win free SBD

Support the Gold Sponsors of the contest: @good-karma and @lukestokes