FT Rebuttal: Part 1 - Assessing How Modinomics Has Reached the Poor

Authored by jain and govil - astute political observers

FT Rebuttal: Part 1 - Assessing How Modinomics Has Reached the Poor

Modinomics is yet to deliver – so screams the headline of an article (opinion editorial : Op-ed) written in a respected international financial daily ‘Financial Times’ published from the hub of probably the most influential financial capital of the world, London. How professorial! Is it a surprise that FT publishes such Op-ed? Not at all.

https://twitter.com/ft/status/1069894756929585152

Reading through the article one is left to wonder whether it is an assessment or a wish. And you can’t blame them. The author of the article is after all the ‘Editorial Board’ of the esteemed ‘Financial Times’. The creme la de crème of the financial world. The people constituting the Editorial Board are probably so used to a rarefied view from their ivory towers that ground realities are often either not visible or they ignore them because it does not support their narrative. Let’s get to the bottom of the facts and data, and, see how meritorious the Op-ed opinion is.

The terms Modinomics really needs no introduction. However, for the benefit of the uninitiated, the term Modinomics is coined by the financial experts for the economic policies of the current Prime Minister of India, Mr Narendra Modi. By definition therefore the time period of review starts from 26th May, 2014. A period of 4.5 years till date which is also the reference point for the Op-ed.

Let’s begin with some basic observations on the article before we get into detailed facts and data. First, the Op-ed starts with a statement that is absolutely unrelated to the subject of the editorial. It points out some errors in a history text book of one of the states in India. And goes on to make sweeping judgement which is quite erroneous too. To ascribe an error that crept in one of the textbooks of one of the states (which incidentally got rectified also) as a major policy blunder or a mala fide intention (‘Changing history’) of the Central government smacks of a prejudiced mindset (Remember India has 29 states and seven union territories). Second, the authors do not seem to be clear whether they want to make an economic case or a political case. No wonder the Op-ed is low on data and facts, and, is high on sweeping statements, more political than economic. And finally, a political statement in the Op-ed that a win for the ruling party in upcoming general elections next year, if that happens, will be due to fragmented opposition rather than work done by current government over the last 4.5 years. Not only is the judgement of the Editorial Board absurd, it also reveals a mindset that they consider the Indian electorate naïve and incapable of making the right choice. This group of people (The Editorial Board), sitting thousands of miles away, with little or no touch to ground realty, believe, they know it all. How very presumptuous!

What are the statements made in the Op-ed (issues raised). They are as under:

- Modinomics has yet to deliver to many in India.

- Failed infrastructure overhaul

- Failed attempt to turn country into manufacturing powerhouse

- Demonetisation ineffective

- Economic growth squandered away on symbolic projects (Statue of Unity)

- Fudging statistics

- NPA’s (Non Performing Assets of Banks)

- RBI Fracas (Reserve Bank of India)

Starting with this article we would bring out a series of eight articles where each issue raised in the Financial Times Op-ed as listed above, will be taken up and put under microscope of facts and data to critically test the validity of the statements made. This article would examine the statement ‘Modinomics has yet to deliver to many in India’. This also happens to be the title of the Op-ed. Lets get on with the analysis.

At the outset, one wonders what is their underlying data to make a statement, that is to say the least, so way of the mark. The Government of India, in the last 4.5 years, have launched a number of schemes primarily targeted towards the people below poverty line or needy people. Though, many of these schemes impact the middle or upper middle class as well. And, some of them impact even the upper class. These schemes have been highly successful in the field, and, have brought benefits, respite, and, succor to a large number of people. We examine below some of the prominent schemes that have touched the lives of people across India.

i. Ujjawala Yojna http://www.pmujjwalayojana.com

India’s population of 1.30 billion plus consists of about 250 million households. Approximately 40% of these households i.e. about 100 million households were without any proper facility for domestic cooking fuel.

The Ujjawala Yojna is a scheme announced to tackle this problem and in a short span of 4.5 years almost 58 million plus connections have been released in the field and are operational. Buoyed by the huge success of the scheme the Modi Government has revised the target upwards and is now targeting to achieve 80 million by 2020 instead of 50 million as was targeted originally.

This is what has been said by the World LPG Association about the domestic clean fuel plan of Modi government. Not just the statement, but also look at the statistics therein.

**‘India has become the second-largest domestic LPG consumer in the world due to the Narendra Modi government’s rapid rollout of clean fuel plan for poor households and fuel subsidy reforms. This has resulted in the domestic distribution sector having the highest consumption of LPG (88%).

India produces about half of LPG for domestic consumption and has almost 18,000 LPG distributors and 182 million state- and company-wise customers. State-owned oil marketing companies (PSU OMCs) have a total of 188 LPG bottling plants all over India, and a total of 677 Auto LPG Dispensing Stations for catering to LPG demand in the automotive sector ’. **

Source : https://www.wlpga.org/key-india/

ii. Pradhan Mantri Gramin Awas Yojna

https://rhreporting.nic.in/netiay/PhysicalProgressReport/YearWiseHouseCompletionReport.aspx

One of the key facilities sought by people is a roof over their head – Shelter. Modi government took it up as a mission with their scheme - Pradhan Mantri Gramin Awas Yojana (Launched in 2015). The government has been highly successful in implementing the scheme, as revealed by the data. The target set by the government was to have 20 million houses by year 2022. And, within a span of 2.5 years they have reached almost 6.5 million plus houses. Contrast this with the period before Modi government came to power. From 1985 to March 2014 only 4 million houses were built. See the contrast – 4 million in about 20 years and 6.5 million plus in 2.5 years. This government has also made sure that they tone up the implementation. As a result, the benefit today actually goes to the ones who deserve it – i.e. those who actually do not have a concrete house and live in a mud house. Further, the government took a 360⁰ view to ensure that the houses are complete with electricity connection, and cooking gas. The picture on your left shows a house under construction, and, the next one, a finished house with its proud owners.

Encouraged by the success of the scheme the government has enhanced the vision to encompass ‘Housing for all by 2022’. Not just rural, but urban areas as well. The mission applies to the country as a whole.

iii. Electricity for All http://saubhagya.gov.in/

Modi government set about this ambitious plan - ‘Electricity for All’ - in 2014. According to World Bank report out of about 1.06 billion people without electricity across the globe, about 270 million were from India i.e. about 27% (As per WB ‘Sustainable Energy for All mission’). Meeting the objective of Electricity for All from an Indian context entails the following:

a) That electricity must reach every village – this is Grid availability

b) That every household must have an electricity connection at home – this is last mile connectivity

c) That there should be power available in the grid for every household – this is power availability in the grid.

In addition to the above mentioned three hard issues, there are softer issues like affordability of taking an electricity and on-going affordability to pay for the electricity consumed.

Modi government took up this challenge in right earnest. As a first step (point a. above) the government worked towards making sure that every village in the country must have Grid availability. There were 19679 villages in India which were without electricity (Grid not being available), as of mid 2014, when Modi came to power. In his Independence Day speech in August 2015 from the ramparts of Red Fort, PM Modi announced that in 1000 days the government will electrify all remaining villages. The villages were electrified ahead of the schedule. The schedule was 1st May 2018. The number of villages electrified were 18,374. There were 1270 villages that were uninhabited and there were 35 places that were classified as villages but were grazing land and hence were de-electrified. (http://garv.gov.in/dashboard).

The next stage (point b. above) was even more challenging – providing electricity connection to every household. It was challenging because of multitude of factors:

- The numbers were astronomical – 212 million Households

- The task was to be carried out by state governments and many of them were not under control of ruling party BJP.

- The connection required that not only the household pay for the one time connection fee, but they should be able to foot the on-going electricity charges – howsoever subsidised they may be.

This was a daunting task even for a person like Modi. But undeterred, Modi government plunged into the task, and, went ahead to announce that all households will be electrified by 2019. Bear in mind that the World Bank had themselves set a target of 2030 to achieve this milestone worldwide -Electricity for All. And here was India proposing to complete their part by 2019. Some nerve and commitment, one must say. Result – as of Dec 2018, almost 99% plus task has been completed with only about less than a million households remaining to be electrified (752,828 to be precise). And even these households are concentrated in only four states out of 29 – Rajasthan , Assam, Chattisgarh and Meghalaya. Hats off to this stupendous achievement. No wonder, both the International Energy Agency and World Bank appreciated and recognized India’s tremendous effort. The World Bank report quoted below is dated May 2018. In the period since then, about 7 months, the figure of 85% has moved up to 99% plus, well on path to achieve the target of 100% by 31st March, 2019.

And, finally to the last point in Electricity to All (point c. above). Availability of power in the grid. It is for the first time in the history of the country that power is almost available on tap in the grid. Gone are the days when people had to suffer 15-16 hours of power cut (some places as high as 20 hrs plus minus). Today this is no longer the case. The dark days of ‘no power’ are receding from the memory very fast. See the power availability data including the peak time power availability.

With the data we have seen above – cooking fuel for All (Ujjawala scheme), Housing for All (Awas Yojna), and, Electricity for All (Saubhagya Yojna) - for Editorial Board to conclude, or, even remotely suggest, that ‘Modinomics is yet to deliver….’ is nothing short of hara-kiri. And, it is hara-kiri with the people who buy and read their paper, hara-kiri with their profession, and perhaps above all, hara-kiri with their own professional skill and knowledge. Having said that let us move on to further see what all Modinomics has delivered to the bottom half of India’s population

iv. Ayushman Bharat

https://www.india.gov.in/spotlight/ayushman-bharat-national-health-protection-mission

https://www.pmjay.gov.in/

This scheme has been designed to provide Universal Health Care to the bottom half of the country’s population. It is by far the most ambitious scheme worldwide, launched by any country, towards health care safety net for its citizens. The scheme is going to provide health care facilitation to about 100 million families covering about 500 million people – almost 40% of the country’s entire population. Imagine covering the entire population of USA, UK, France, Germany and Italy, in one go.

The scheme was launched on 23rd September, 2018 and has already gained considerable momentum in the country. As of 10th Dec, 2018 almost 16,000 hospitals have been empanelled. The scheme is already showing promising results with more than half a million people having availed of hospitalization benefits.

We now move on to examine how the Modi government went about providing financial inclusion to the vast population who were denied the same all these years. Bear in mind, that the banks in India were nationalized almost 50 years back (half a century back). The avowed objective was to take banking to the needy people. To make credit available to them on priority and preferential basis. To enable them to make a better living and define better livelihood for themselves. Yet, it all remained a mirage for the majority of them. This task of Financial inclusion was taken up by Modi government in the right earnest and within three months of their taking oath of office the PMJDY scheme was announced. Six months later the MUDRA scheme was announced. Let us examine how these schemes fared.

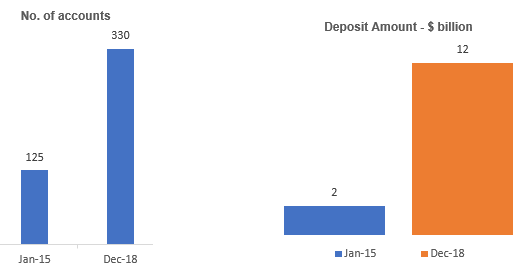

v. Pradhan Mantri Jan Dhan Yojna (PMJDY) www.pmjdy.gov.in

This is one of the largest financial inclusion actions taken by any government across the globe. Recognizing that a very large cross section of the population in India were unable to participate fully into the economic activities of the country due to lack of access to banking, the Modi government took up the challenge in right earnest. Wasting no time PM Modi announced PMJDY from the ramparts of Red Fort in his Independence Day speech on 15th August, 2014 (less than three months from taking oath of office). And, set out a very ambitious target for getting people from the lower strata to open bank accounts. Results – by 26th Jan 2015 (India’s Republic day) i.e. in less than six months, more than 125 million accounts were opened with deposits of more than $ 2 billion then. Today, as of Dec 2018, the number of account holders has gone up to 335 million plus with deposits in excess of $ 12 billion.

The story gets much more impressive when one looks at the reduction in numbers for zero balance accounts, and, the increase in average deposit per account. It would be of further interest to know that almost 200 million of these accounts have been opened in Rural / Semi Urban areas of the country, and, some 50% plus (178 million) are female account holders. From a Financial Inclusion perspective, the government could not have asked for anything better.

One can drool over a lot more statistics on PMJDY, but, this data is sufficient to rebut the canard of Op-ed. And if one were to go a step further and examine the stellar role played by this singular step in reaching the benefits of the government schemes to the nook and corner of the country, then, the Op-ed title ‘Modinomics is yet to deliver……’ will not find any cover anywhere. Riding on the success of PMJDY, Modi government came up with announcing the DBT (Direct Benefit Transfer) implementation.

The announcement meant that all government subsidies, benefits to the beneficiaries under various government schemes would be directly transferred to the bank account of the beneficiary. It meant extreme convenience, almost zero leakage (no corruption), and, almost instant transfer of money. Many vested interest groups, middlemen, and commission agents were upset as it disrupted the entire corruption network. Needless to mention, many of the political parties were also upset as they were hand in glove with these vested interests and the corruption network.

vi. Micro Units Development & Refinance Agency Limited (MUDRA)

https://www.mudra.org.in/

Launched in April 2015, the scheme was designed to provide loan to the non-corporate, non-farm small/micro enterprises of individuals from the bottom of the pyramid. The scheme has been a runaway success. Since its launch, a sum of $ 105 billion worth of loans have been sanctioned and almost 95% plus have been disbursed also. Bear in mind that the maximum loan amount under this scheme is $15,000 (compared to big loans that are normally $ 250,000 upwards). There are 150 million plus beneficiaries who have so far taken loan under MUDRA scheme. Most of the beneficiaries are for small and marginal sums. Who are these people? They are the ones who were deprived of bank loans hitherto, despite bank nationalisation in 1969 – almost 50 years back (half a century back). Result, these people had either given up their dreams or were forced to go to local money sharks who often charged astronomical interests – 40% plus per annum, thus falling into debt traps. Modi governments Mudra scheme brought them right back into the

mainstream of economic activity. Empowered them and gave them hope. And mind you this was no freebie. Loans were given to them on regular banking terms and they were very happy about it. It is a bit strange that the Editorial Board does not see this hugely successful scheme as touching the lives of poor or needy people.

We have seen in the forgoing part how the Modi government provided the basic conveniences of domestic cooking fuel, housing for all, electricity for all, financial inclusion, financial facilitation, and perhaps the most important – Medical coverage for self and family members. For the purpose of proving the hollowness of the article these data points would suffice. But we move on to now see how the Modi government touched the lives of people in many other different ways. Here are some of the other schemes launched by the government.

Social Security

https://financialservices.gov.in/new-initiatives/schemes

- Pradhan Mantri Jeevan Jyoti Beema Yojna (Insurance scheme covering life of an individual at nominal annual insurance premium)

- Pradhan Mantri Suraksha Beema Yojna (Insurance scheme to cover accidental death or disability. Nominal annual insurance premium)

- Pradhan Mantri Vaya Vandana Yojna (A pension scheme with death coverage for senior citizens – 60 years or above. Available in many sum assured categories to suit individual needs)

- Atal Pension Yojna (Pension scheme predominantly for workers in unorganised sectors. Premium based scheme with Co-contribution from Government.)

Upgradation of skills to enhance employability.

- National Apprenticeship Training Scheme -

- Stand up India Scheme

Women and girls benefits

- Beti bachao beti padhao (woman education and empowerment)

- Pradhan Mantri Matru Vandana Yojana – Pregnancy Aid Scheme (benefits available to all Pregnant Women and Lactating Mothers)

Minority Community Development

- Pradhan Mantri Jan Vikas Karyakram

It is more than clear from the above facts and data how misplaced the Op-ed is in terms of their statement – Modinomics has failed to deliver.

In fact, Modi government takes a holistic view. It is no surprise for those who are familiar with the philosophy of the Modi government. Their guiding principle is ‘Antyodaya’ a word of Hindi language written here in English script. The word means – rise of the last person. In context, it means upliftment of the poor till the poorest person is able to stand on feet. This word was given by Pandit Deen Dayal Upadhya who was one of the founding leaders of the ruling BJP party. He had a unique measurement basis. “The measurement of economic plans and economic growth cannot be done by counting those who have risen above on the economic ladder, but, by counting those who are at the bottom and have been left out”. Inherent in this measurement principle is the fact that a scheme is not successful unless the last man in the queue has been uplifted.

We have seen above how Modi government has implemented this measurement in their goals and evaluation parameters. No household without electricity, no home without domestic fuel, no household without a bank account, no person without healthcare coverage, no person without social security, and so on. But while all this is happening on the ground in India, the Editorial Board of Financial Times, cocooned in their Ivory Towers, used to a rarefied view of their world, are unable to see the ground reality. Or is it that they do not want to recognize all this as it does not suit their narrative. Or perhaps some sinister political motive. The Editorial Board would know it best.

We work hard to research the topic and collect data points to form a narrative. So, if you like the article please upvote, resteemit and leave a comment.

A must read!

very nice

Added the "politics" tag

@ajain, thank you for supporting @steemitboard as a witness.

Click on the badge to view your Board of Honor.

Once again, thanks for your support!

Do not miss the last post from @steemitboard: