The Push For A One World Digital Currency

Satoshi Nakamoto's original vision described in the first sentence of the original whitepaper for Bitcoin called for a purely peer-to-peer version of electronic cash [that] would allow online payments to be sent directly from one party to another without going through a financial institution.

Financial institutions easily ignored Bitcoin when it was first introduced, but as it grew in popularity and became increasingly impossible to ignore, major financial players ridiculed and dismissed Bitcoin as a pipe dream, a delusion, a fraud, and later a bubble.

Jamie Dimon, chairman and CEO of JPMorgan Chase, the largest of the big four American banks who previously served on the board of directors of the Federal Reserve Bank of New York, was labeling Bitcoin a fraud last year, going as far as to say he would fire any employee trading bitcoin for being “stupid”.

In early 2018, however, the big bank is now taking cryptocurrency very seriously—acknowledging the blockchain-based technology as a veritable threat to its future, as reported in Fortune

In JPMorgan Chase’s annual report, released Tuesday afternoon, the bank counted cryptocurrencies such as Bitcoin and Ethereum as “risk factors” to its business for the first time, recognizing the digital currencies as new forms of competition that could, quite literally, give the bank a run for its money.

“Both financial institutions and their non-banking competitors face the risk that payment processing and other services could be disrupted by technologies, such as cryptocurrencies, that require no intermediation,” the bank wrote in the report.

Already, the bank added, new technologies have required the company to invest in adapting or modifying its products to draw and retain customers, and to compete with new offerings from tech upstarts, a trend it expects to continue. “Ongoing or increased competition may put downward pressure on prices and fees for JPMorgan Chase’s products and services or may cause JPMorgan Chase to lose market share,” according to the report. source

If it's a fraud with no intrinsic value, as Jaime Dimon has repeatedly said, and people who trade it are stupid, how can it also be a threat to large banking institutions and what are they going to do about it?

So what does one of the largest banking groups do when encountering what it sees as a potential threat to its market share? Historically, they crush their competition while positioning themselves to either take it over or create their own digital coin network and it would appear that is exactly what world banks are aligning to do.

A global digital currency for international transactions completely traceable with verified ID's sounds like a conspiracy theory or plot in a futuristic sci-fi movie, but is it? G20 leaders who gathered this December in Buenos Aires, Argentina have called for “a taxation system for cross-border electronic payment services.”

As Cointelegraph reported in October 2018, the CEO of the company behind the cryptocurrency investment app Circle had called for “normalization at the G20 level” of the crypto industry.

In July, France’s finance minister Bruno Le Maire also called on the G20 to have a public debate about cryptocurrencies at this weekend’s summit.

Le Maire said that leaders will “have a discussion altogether on the question of Bitcoin (BTC)” since “there is evidently [the] risk of speculation.” He then concluded that France needs to “examine this with other G20 members” to see how “we can regulate Bitcoin.” source

“Normalization at the G20 level” means they want to regulate crypto on a global scale, essentially passing laws that no jurisdiction could escape from. There wouldn't be any country that exchanges and blockchain developer talent could gravitate to that are crypto friendly and all countries would have to follow the rules they create.

They want a payment system for cross-border electronic payment services. What's interesting to me is this has never happened before. We have remittance systems already. We have Western Union, MoneyGram, applications like PayPal and Square and Venmo, but now there's this big push for cryptocurrency.

Did this just occur? 2018 has been the worst year for cryptocurrency price action. We've seen the worst November since 2011. Where's this newfound interest all of a sudden? Wouldn't 2017 have been a better year to start talking about these things? We did hear some talk of mainstream adoption in 2017 but 2018 really seems to be the year that the SEC is moving in, the U.S. is moving in on regulation and now there's this serious talk about how do we tax this globally.

There were digital currencies that existed in the early 2000s that were shut down with the help of Western Union and MoneyGram because they had almost a monopolistic, cartel-like grasp on the entire market of sending money internationally for people who didn't have bank accounts. Even right now we have roughly 2bil unbanked people on the planet.

I think this is very interesting that G20 countries are now coming out with wanting their own version of bitcoin only two weeks after the head of the IMF addressing an audience in Singapore at Fintech. Fintech has a big piece of all this digital currency game.

At the Fintech Festival in Singapore, Christine Lagarde, IMF Managing Director talked about how there needs to be an international digital currency.

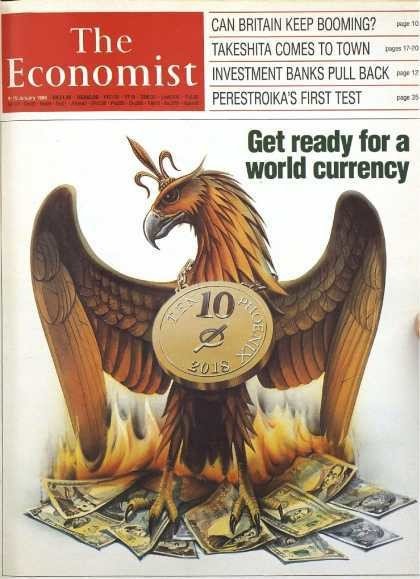

She wasn't the first to talk about this. In 1988, long before bitcoin was even a thing and right after the global stock market crash in 1987, the cover story for The Economist shows a picture of a Phoenix, with a coin that resembles the look of today’s most popular cryptocurrency, Bitcoin. What's even more intriguing about the picture is the fact that the year on the coin reads 2018. It’s also interesting to note that the article is discussing a completely new type of currency, a global currency, one that emerges from the ashes of cash.

Was this 1988 article a prediction or writing on the wall warning us what they're doing? Depending on how fringe you want to get we also have George Soros who has talked about this New World Order where part of that is this one world currency. You can't have a one world paper currency because it would be incredibly hard to keep track of, you'd have a one world digital currency. Plus, digital currency, being digital, would make it much easier to control compared to a paper or fiat currency.

Christine Lagarde's speech went on to say in part:

A new wind is blowing, that of digitalization. In this new world, we meet anywhere, any time. The town square is back—virtually, on our smartphones. We exchange information, services, even emojis, instantly… peer to peer, person to person.

We float through a world of information, where data is the “new gold”—despite growing concerns over privacy and cyber-security. A world in which millennials are reinventing how our economy works, phone in hand.

What role will remain for cash in this digital world? Already signs in store windows read “cash not accepted.” Not just in Scandinavia, the poster child of a cashless world. In various other countries too, demand for cash is decreasing—as shown in recent IMF work. And in ten, twenty, thirty years, who will still be exchanging pieces of paper?

Bank deposits too are feeling pressure from new forms of money.

Think of the new specialized payment providers that offer e-money—from AliPay and WeChat in China, to PayTM in India, to M-Pesa in Kenya. These forms of money are designed with the digital economy in mind. They respond to what people demand, and what the economy requires.

Even cryptocurrencies such as Bitcoin, Ethereum, and Ripple are vying for a spot in the cashless world, constantly reinventing themselves in the hope of offering more stable value, and quicker, cheaper settlement.

Let me now turn to my second issue: the role of the state—of central banks—in this new monetary landscape.

Some suggest the state should back down.

Providers of e-money argue that they are less risky than banks, because they do not lend money. Instead, they hold client funds in custodian accounts, and simply settle payments within their networks.

For their part, cryptocurrencies seek to anchor trust in technology. So long as they are transparent—and if you are tech savvy—you might trust their services.

Still, I am not entirely convinced. Proper regulation of these entities will remain a pillar of trust.

Should we go further? Beyond regulation, should the state remain an active player in the market for money? Should it fill the void left by the retreat of cash?

Let me be more specific: should central banks issue a new digital form of money? A state-backed token, or perhaps an account held directly at the central bank, available to people and firms for retail payments? True, your deposits in commercial banks are already digital. But a digital currency would be a liability of the state, like cash today, not of a private firm.

This is not science fiction. Various central banks around the world are seriously considering these ideas, including Canada, China, Sweden, and Uruguay. They are embracing change and new thinking—as indeed is the IMF.

Today, we are releasing a new paper on the pros and cons of central bank digital currency—or “digital currency” for short. It focuses on domestic, not cross-border effects of digital currency. The paper is available on the IMF website.

I believe we should consider the possibility to issue digital currency. There may be a role for the state to supply money to the digital economy.

This currency could satisfy public policy goals, such as financial inclusion, and security and consumer protection; and to provide what the private sector cannot: privacy in payments. Winds of Change: The Case for New Digital Currency By Christine Lagarde on the IMF website

This sounds encouraging but ignores some very critical benefits of a true purely peer to peer digital money system envisioned by Satoshi Nakamoto.

- It's issued and controlled by the state and not decentralized so it's value can be manipulated. When she mentions AliPay and WeChat in China, to PayTM in India, to M-Pesa in Kenya, she forgets to mention these are all centralized solutions.

- There is no limited supply and could be issued indefinitely leading to inflation and erosion of its value, just like fiat money is today.

- There's still a third party involved who could charge for transactions and trace its use, just like banks do now.

- With custodial control, they could withhold your money much as a bank can today.

Basically, a digital currency with everything that makes decentralized digital currencies cool stripped away from it. And say what you will about the pieces of paper we call cash, even though it can be printed to the point of making it almost worthless, at least you can retain your privacy using it.

It is clear that world banks and leaders like the idea of a world digital currency, but one they can control and regulate. We already have a world digital currency in bitcoin, but bitcoin's decentralization is at the core of major financial institutions reluctance to use it. They're coming to the realization that they can't actually regulate bitcoin, only the exchanges where crypto meets fiat, and only according to the local laws those exchanges reside under, which creates obstacles for having a world currency.

Sensing that BTC, this competing monetary system that is difficult to regulate completely, is not going away, central banks and the IMF are simultaneously trying to stunt its growth until they can come up with their own version of a world currency where they hold the reins and guide its course, clever little banksters that they are.

I believe one of the reasons the SEC keeps dragging their feet about bringing cryptocurrency to Wall Street, bank CEO's spread FUD, and mainstream media emphasizes cyber-security risks, criminal activity use, and crypto hackers is to stall the growth and development of competing crypto networks who often don't have the funds to withstand such bad publicity, while it simultaneously conditions people who could benefit from a such a network to seek a more secure, centralized solution the banks will soon offer.

I mean, if crypto is such a risk and has so many downsides to it then why are major financial institution positioning themselves to capitalize from it? The not so subtle implication is that blockchain is good as long as it is centralized and controlled by a bank or government.

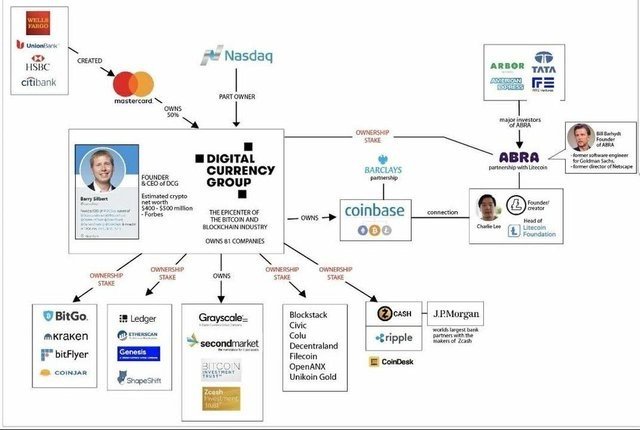

In a recent post by @meno called, Nothing to see, move along..., he illustrates clearly how the big players are moving in to take over a large percentage of the cypto space.

Let's put some things into perspective, and remove the veil of pleasant naivety. If there is a company, a gigantic behemoth of the size of the Digital Currency Group, who is partially owned by MasterCard at that, we can certainly place bets on two fronts:

Cryptocurrencies are not going anywhere and will continue to grow, they are the future.

Manipulation has always been part of the strategy.

The swings of the market then, without a doubt, are literally a mechanism of funneling retail investors, dumb money as they are often referred to, towards the big guys, the ones that have always owned the building. This is not to say swings should not happen, or that there is even a system that lacks them because of course, that would not be accurate, but the irrationality of the markets is not irrational at all, but more designed to seem this way. source

Big institutions like central banks who seem to have a monopoly on the flow of money and can shape the future of government policies through how they choose to loan that money are known for being slow to move when new innovations come along. But when they do they do it through a myriad of regulatory bodies, interlocking corporations, and complexity that creates a barrier to entry that only well-funded, large players can compete with.

Perhaps they didn't see bitcoin coming or didn't perceive it as a threat to their business, but now they seem to be positioning themselves to have their hands in every piece of the crypto pie, much like Bill Gates and Mark Zuckerburg who bought controlling interests in every new promising startup during the internet boom so as to have controlling influence on not only its direction but whether it lives or dies. If it competed with similar products they were rolling out it either got bought out completely and incorporated into their product or put on a dusty shelf and defunded.

Or perhaps this was the central banks plan all along.

Knowing the people were not ready for a world currency when they were first talking of introducing one back in 1988, they anonymously released a white paper written by Satoshi Nakamoto, perfectly timed after a world financial crisis when trust in central banks were at an all-time low, that presented a peer to peer cash system that would allow online payments to be sent directly from one party to another without going through a financial institution, a trusted third party, a bank.

This started a revolution from the bottom up, with the people not only accepting digital currencies in favor of cash but demanding it. Those clever little banksters that they are.

My conspiratorial mind may be working overtime, but think about it. Once the people accept digital currency like bitcoin, believing they were the ones who started this revolution, banks could easily and pseudonymously inflate the price through manipulation until everyone is talking about it and tempted to speculate on the potential profits.

Then infiltrate the development communities with proponents of competing proposals on how to address the scaling problems they were experiencing causing divisive factions within those networks until they fork the coins into smaller and weaker competing networks. Now your competition is easier to eliminate or at least it slows them down.

Then, pseudonymously deflate the price through manipulation until all the weak hands fold while creating hundreds of companies you hold a controlling interest in to further its development by hiring away all the best developers even as you stoke people's belief that it will ever take off and become a mainstream thing which causes pushback and gets the people wanting it even more. Ever tell a child not to do something or tell them they can't do it? It's a sure way to get them to want to do it even more.

Tie up the regulatory process so bad that all the different regulators can't even define it as a commodity, security, or asset, let alone regulate it until you issue your own bank-backed, government approved, and more importantly, government-issued digital currency, forgoing the need to even have a difficult to regulate exchange at all.

Now that you employ all the best developers you can begin funding new easier to use apps, innovation mushrooms and, miraculously, digital currencies become widely accepted around the world at every store, as easy to use as sending a text, replacing hard to trace cash as the means of transacting value.

To make sure no other competing crypto network rears its ugly head and competes with you in the future, stop funding all development except for your one world coin, hire all the best devs away from them to come work for you, buy a controlling interest in any promising new startup and disguise it as venture capital, and eventually people will either stop using it, except for criminals, in which case you make it illegal and no store will accept it anymore. Why would they when there's a globally accepted, easy to use, and price stable digital coin instead?

It's also interesting to note the timing of that 1988 Economist article talking for the first time about a world currency which was also after the global stock market crash in 1987, has similar timing to the release of the original bitcoin whitepaper which was also timed right after the latest financial crisis of 2008, when people's confidence in our current financial institutions are lowest. Coincidence?

Think it couldn't, or isn't happening right before our eyes? Think again. Greed is a powerful aphrodisiac and when you just lost your life savings it could act as a powerful motivation for change. Never let a good crisis go to waste, right?

When I was a boy I had a dog that followed me around everywhere. The most loyal dog you could ever have. But if you had a piece of meat in your pocket, he would drop me like a hot potato and start drooling at your feet, wagging his tail for that delicious morsel.

The crypto drama being played out right now with the SEC baiting Wall Street and institutional investors suggesting they are poised to invest is just the thing that could wag that tail. They can't regulate bitcoin as they can fiat, this is becoming more clear to regulators. And they can't centralize it. So, their next best option is to buy it, shelf it, or come out with their own better product.

You didn't really think that central banks were just going to accept the competition and share a slice of the financial sector's profits, did you?

There's an old saying from a popular slogan among the 1960s Black Power movements in the United States that says, "The Revolution Will Not Be Televised". Historically, revolutions that threaten the status quo are not funded either and if they grow to be uncontrollable they have traditionally been infiltrated, co-opted, and derailed in one form or another.

There are individuals whose net worth is a fraction of the entire crypto market cap. A handful of billionaires with multiple wallets, let alone banks acting pseudonymously, could easily buy the crypto space out or affect the price movement at will, especially if they are incented with a promise of a seat on the board of directors of a new global digital currency able to draw tax revenues on a global scale.

Wile Johnny Hodl is biting his nails waiting for the moon, and speculators pitch their investment schemes to low hanging fruit flies, the average Joe doesn't give a damn about how decentralized his digital coin is as long as he can buy a Starbucks and a cold beer with it.

I'm not saying Bitcoin is dead, but it does appear the buzzards are circling. I still believe in and use bitcoin. I'm not a speculator or HODLer, but use it as money more than a store of value, and before you think I've given up on it let me point out some fundamental principles of why I still use it.

Bitcoin is not susceptible to inflation. There are a finite, determinable amount of bitcoins that will be issued over a known period of time. That means as long as the demand for it exists and continues to grow the value can only go up over the long term. And the demand is growing. Sure, the people who bought just because they thought they could make some money from investing in it are leaving the space and is one reason why we see the recent price plunge, but usage overall is growing.

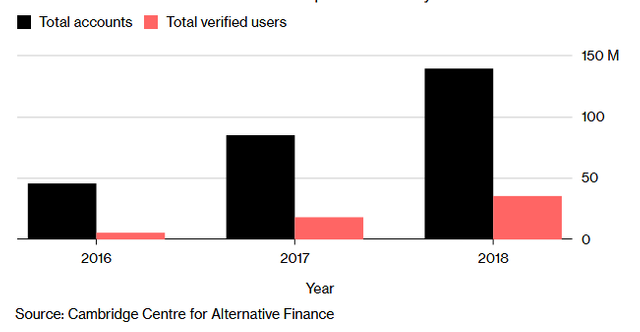

The University of Cambridge Center for Alternative Finance says the number of verified cryptocurrency users has increased in 2018 despite the year-long bear market that has seen prices tumble more than 80 percent. The study shows that there were 35 million authenticated cryptocurrency users as at the end of September 2018. source

More bitcoin users plus less bitcoin means the price goes up, but that's not why I bought bitcoin. I use it because I don't like banks. I don't like the wars they fund, the economies they manipulate, the unserviceable debt they create, or the control they have. To me, bankers are legal money counterfeiters putting future generations under debt they will never be able to pay back which enslaves us to work forever just to survive. The endgame in that scenario is the rich get richer and will eventually own everything.

I don't want a world digital currency but it looks like we're going to get one eventually

Bitcoin is an alternative, competing money system that cuts the banks out of the loop, so when I see huge financial institutions getting involved in Bitcoin it doesn't make me excited or make my tail wag to the scraps they offer. I don't even think of Bitcoin as a store of wealth. Gold has stood the test of time and is a better choice, bitcoin is, after all, digital. Have you ever had your computer crash or lose a file?

What I find attractive about Bitcoin is it moves away from supporting such control similarly to cash without the inflation. A favorite saying of Alex Spanos was "Cash Is King". I think of bitcoin as cash 2.0 and treat it like cash. Call me old-fashioned. Central banks are moving countries towards a cashless society for a reason. Cash doesn't give them total control like your credit card or debit card does. They can't charge you a fee for using it or turn it off when it suits them and they can't do that with bitcoin either.

A global digital currency may come along that offers convenience, but decentralized currencies are more than that. They offer sovereignty and you don't need anyone's permission. No amount of profit or convenience can replace that piece of mind that your coin is truly your coin.

Hey Luz, thanks for this well written and carefully considered post. I don't think what you've outlined here is far fetched at all. The bait and switch, crash to buy model of control has been in place for a very long time. The question in my mind is: which will it be? Adoption/cooption or marginalization/assassination? Either way, those with the resources to do so will find a way to use crypto to consolidate their power base rather than be undermined by it. It would be foolish to assume otherwise.

Posted using Partiko Android

Hey Luz, thanks for this well written and carefully considered post. I don't think what you've outlined here is far fetched at all. The bait and switch, crash to buy model of control has been in place for a very long time. The question in my mind is: which will it be? Adoption/cooption or marginalization/assassination? Either way, those with the resources to do so will find a way to use crypto to consolidate their power base rather than be undermined by it. It would be foolish to assume otherwise.

Posted using Partiko Android

Agreed. It's naive to think otherwise. Banks have been playing the money game for centuries and they're not about to let some new technology get a slice of their pie, not when they're on the verge of consolidating the entire world's finances.

nice graphs, cool post /// let's decentralize the shit out of monetary sytems, various at each scale, local-regional-global ... just deactivated my FB , hell yeah ! paz

It's funny to think that deactivating your Facebook account is a bold move. That's the first thought I had when reading your message. On second thought, I remember the days BFB (Before Facebook). Life moved along just fine without it. Good move.

I hear that, ty, for me it was just for seeing some family pics, for others they are totally dependent on it. It is scary that one has to hesitate and think twice before cutting off from a silly website ... life can be insidious like that.

Selling or buying for cryptocurrency people by and large play the lottery, as these coins can be very expensive or very small tomorrow. Given the business world are buying and selling in the mass is stupid and unnecessary. I am a supporter of classic purchases and transactions, and everything else is very risky. I can't even imagine when I would buy a car or a hamburger for Google shares... for me, the cryptocurrency is a bit similar to shares and purchases for the crypt are absurd for me.

Everyone comes to crypto for a different reason and in different ways. If I were to purchase Bitcoin to speculate on its price rising in the future, then buying things with it would be absurd indeed. But when one earns their crypto through working it is a different story. In that scenario, cashing some out for covering your monthly expenses makes no difference what the price is. The price only affects the balance that remains.

Hi @luzcypher!

Your post was upvoted by @steem-ua, new Steem dApp, using UserAuthority for algorithmic post curation!

Your UA account score is currently 6.683 which ranks you at #125 across all Steem accounts.

Your rank has not changed in the last three days.

In our last Algorithmic Curation Round, consisting of 216 contributions, your post is ranked at #40.

Evaluation of your UA score:

Feel free to join our @steem-ua Discord server