Dark Clouds Are Looming – Australian Property Market Update for the Week Ending 25 June 2017

I write a weekly property market update for PropertyInvesting.com, and after the positive feedback I received on last week’s update, I’ll keep these coming on Steemit for the time being.

The Latest Preliminary Auction Activity

In Sydney and Melbourne, it’s common for homes to sell at auction. Sometimes hundreds of people will show up on auction day at the property to watch bidders battle it out to pay top dollar for their dream home.

If you’ve never experienced an Aussie property auction, it's quite a sight to behold. Check out just a few minutes of this video, where the opening bid started at $690,000, but thanks to the auctioneer’s persistence, ended up over $900,000.

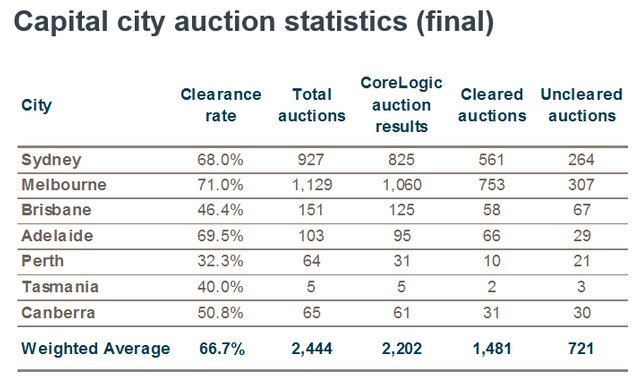

In the following table, you’ll find the preliminary count of successful auctions from a property data collecting company called CoreLogic. It includes both the auction clearance rate, which is the percentage of all auctions in the city that found a winning bidder, and the total number of auctions.

Here are the latest preliminary results for the Australian capital cities:

Source

These stats provide a weekly snapshot of both supply and demand in the housing market.

You can see from these latest preliminary results that both Melbourne and Sydney had a clearance rate in the low 70s, which tends to be a show of moderate strength and indicative of rising home prices.

That said, the Sydney agents tend to inflate their results for a show of optimism in the headlines. When the final numbers are reported later this week, I expect Sydney’s result to be in the high 60s.

Brisbane posted some unusually low results this week. It’s too early to say whether that’s a sign of things to come or a one-off bad week.

Last Week’s Final Auction Results

Last weekend was the first week back after the Queen’s Birthday long weekend. That meant supply was down, but as expected, sellers flooded back into the market last week. There were twice as many auctions as the previous week, but demand declined. Melbourne was the stand out performer and helped to lift the nationwide clearance rate average.

Here are all the final capital city results for last week:

Source

Recent Changes in House Prices

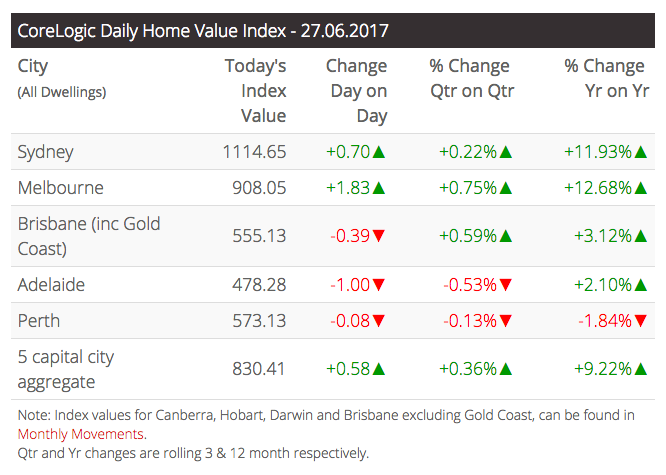

Sydney and Melbourne home prices peaked in April and then took a breather for a month or so, but now it looks like prices are back on the rise.

As of Monday, Sydney had seen 17 straight days of growth, and Melbourne was on a 13-day run. Both cities rose 2 percent over those respective time periods and wiped out most of their recent losses.

As you can see in the following chart from CoreLogic, home prices are almost at the same level they were three months ago, just a little higher. Adelaide and Perth are the notable exceptions, having pulled back slightly.

Source

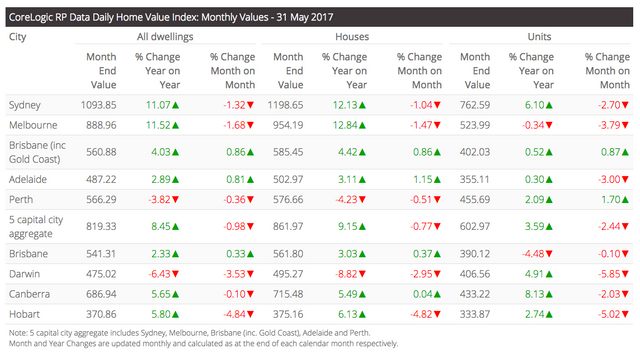

Looking at CoreLogic’s monthly data, you can see that houses have performed better than units. You can see that units and apartments have moved backwards in Melbourne and Brisbane over the past year. In both cities, we have significant supply gluts emerging.

Interestingly, the opposite has been true for Perth, which has really struggled due to the end of the mining boom. There units have performed much better than houses. I think that’s in part because Sydney and Melbourne investors are looking for cheaper properties, and they perceive Perth to be at the bottom of a growth cycle.

Source

Market Summary

Source

I’ve been following auction clearance rates in Sydney and Melbourne for year, and while they are stronger than they were at this time last year, we’re seeing a noticeable trend down. This week was the fourth week in a row where the nationwide result was below 70 percent.

In Melbourne, last week was a record low, and this week was almost as bad as last week.

That said, there are still plenty of buyers out there willing to pay top dollar. One of my clients just sold her 2 bedroom Sydney apartment for $1 million. She would have been happy with $950,000. Actually, when we discussed selling three months ago, she would have been happy with $850,000.

I’m not sure what to make of the recent price rises in Sydney and Melbourne yet. They’ve bounced back strongly over the last two to three weeks, but it’s too early to tell if this is a renew bullish trend. I’m inclined to think not, as there are some major headwinds to deal with from some dark clouds on the horizon, which I’ll cover below.

Dark Cloud #1: Population growth ain’t all that.

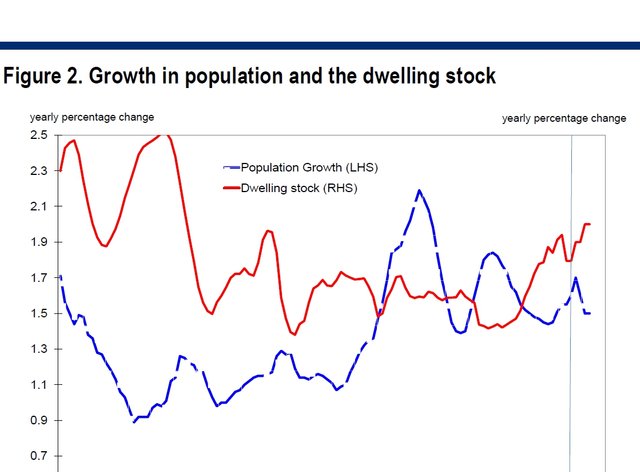

Citibank released analysis this week comparing the current supply of new homes with trends in population growth. Here’s their chart:

Source: Citi via Business Insider

The housing market perma-bulls in Australia like to jump up and down about the massive undersupply of housing stock compared to the mass influx of people moving into Sydney and Melbourne. But Citi’s latest analysis doesn’t match up with that.

As indicated in the chart above, population growth peaked back in 2009, but has mostly been trending down since then. With supply set to outpace population growth, that looks more like a bearish indicator to me.

Dark Cloud #2: APRA is sticking it to investors.

Population growth isn’t the only source of demand for homes. As I wrote about here Aussie real estate is so expensive because of the supply of cheap credit over the past few years.

The Australian Prudential Regulation Authority (APRA) is the banking industry regulator in Australia. They are supposed to keep banks from taking on too much risk, but we all know that’s a joke. They are already leveraged beyond any hope of survival in a SHTF scenario.

The true purpose of APRA is to collude with the Reserve Bank of Australia (RBA) to slow down or speed up the supply of credit. Because the RBA has been suppressing interest rates by printing money to buy short term bonds, property investors have been encouraged to mindlessly speculate on never ending capital growth in the real estate market.

The result has been a massively inflated housing market. Young people trying to buy a home today in Sydney and Melbourne are pretty much screwed. This is putting pressure on politicians to do something. The problem is, they all own real estate and don’t want prices to fall.

At the same time, the Australian economy is only growing at 2 percent per year and the Keynesian economists can hardly sleep at night. They really need to cut rates again to further manipulate the economy and inject some monetary heroin into the system, but doing so would drive property prices even higher, and further piss off those who can’t buy a home today.

That’s where APRA comes in. They have recently been tightening up on banks, making them hold more capital and lend less money. They obviously don’t want to make it harder on first homebuyers or the general home owning public, so they’ve directed their macroprudential measures at investors. The result is higher borrowing costs to investors.

Nearly half of all demand in the housing market has come from investors over the past few years. As APRA continues to cut into this market, it’s hard to remain too bullish on home prices growth.

Dark Cloud #3: The Aussie lending market is on shaky ground.

People can’t afford homes in Australia at current prices unless interest rates remain low. Since 2012, Australian households have taken on an enormous amount of debt, which now amounts to 189% of disposable incomes.

If interest rates start to rise, Australian households will feel it immediately because all mortgages here are set at a variable rate. There is no 30 year fixed rate mortgage here.

Most of the money Australian banks lend out to homebuyers comes from the overseas lending market. They sell bonds to investors in the USA and Europe and then lend that money back out to Aussies here in the form of mortgages.

If bond prices fall and yields rise, these banks will be forced to pay higher interest rates on their debts. Who do you think will pay for that? It certainly won’t be shareholders. Mortgage rates will rise.

Ratings agencies have already started cutting the credit ratings of most of Australia’s banks because of risks in the housing market. That alone makes it more expensive for them to borrow, leading to higher mortgage rates.

When things get ugly, which they always do given enough time, then interest rates will rise, and home prices will fall.

Aren’t you glad you’re earning STEEM?

Jason Staggers

Congratulations @jasonstaggers! You have completed some achievement on Steemit and have been rewarded with new badge(s) :

Click on any badge to view your own Board of Honnor on SteemitBoard.

For more information about SteemitBoard, click here

If you no longer want to receive notifications, reply to this comment with the word

STOPBy upvoting this notification, you can help all Steemit users. Learn how here!

With the government raising wages standards a few weeks ago, which will go into effect in the new financial year. Do you think the banking industry will see that as some extra money to grab by raising interest rates. I know already that prices of goods and services will increase, due to the wage increase as companies need to raise prices to keep profits.

Another informative read Jason. Nicely written and laid out. I agree that we're in for a bit of a shock. I saw it a little while back and have made the necessary adjustments. I hope other's have also. Thanks for a great read.

Thanks mate. It will be interesting to see how it all unfolds. I think there's a chance property prices flatten out for a while, but unless wages rise a lot in a short time, it's hard to see how we can't have a correction of some kind.

Every time you post this info I can't help but have the same reaction of "wow, this is the US market in 2008!"

When all those ARM loans go variable rate it will be real interesting how things play out.

So true. Aussies underestimate the interest rate risk they carry. It will be fine until rates rise because they don't automatically adjust higher, but any changes by the RBA or in the bond market have an immediate effect.

Another great update. Interested to see how this will unfold.

Thanks, me too. Hopefully they'll somehow orchestrate a soft landing.

These prices are out of this world and the fact that the one girl would have been ok with $850,000 3 months ago and got $1,000,000. That is nuts!!!!!

Tucson real estate went up 8.9% last month but I don't expect results like that. Jeezzzzzzz

It has been some crazy growth, although this girl probably underestimated what she could have sold the property for several months ago. Believe it or not, the buyer paid $1m to rent it out for about $2500 per month. About a 3% gross yield.

Hahahhaha, That is terrible. Has anyone ever told them about something called inflation?

I guess if their main play is capital appreciation they think they are going to rent it out and then resell it for a lot more but I just expect a lot of these people to get blown out of the water.

Good point about inflation. But as you say, when you assume infinite annual 12% growth, who cares?

"assume" is the key word. Hahahah

hmmmm, sensing another executive appointment here Jason - you interested?

With the exception of my wit and personality, my home is my largest asset... by a mile - house, large flat block, 30 minutes to CBD - so you think would be happy wouldn't you? Well no - because I simply can't believe how ridiculously stupid the Sydney market is and the participants within.

There is going to be a lot of pain this time round! SK.

Haha! Another title? I don't know, my ego is already pretty big :)

What did you have in mind?

Regarding your home, we talk in our investor training about the difference between an investment asset and a lifestyle asset. It's always tougher to sell the family home to realise a gain. Although sounds like it could be ripe for a subdivision.

No way mate - newly built - will suit for the rest of my life - so market value means nothing to me.

Executive Manager - Property Research and Markets - is the first title to come to mind.

SK.

Happy to serve any way I can. I've been thinking about organising a Melbourne Meetup. It would be good to connect more personally and it seems like there's a pretty good group of Steemians here. I tried it a year ago, but only one other person showed up. It was early days.

Great read Jason, it's quite refreshing to hear someone in the industry who's not afraid to tell it the way it really is. Do you feel comfortable throwing out any dates to when you think this charade will start to pick up some pace to the downside. Cheers, upvoted and resteemed.

I'm surprised they've kept it going this long. Australia is at the mercy of the Fed, ECB, and the PBoC. I don't expect a property correction here until something crazy happens overseas - maybe European bank / derivitives related. When the bond market deflates, shares fall, derivitives unwind and banks fail it could be very bad. If we make it through 2018 business as usual I'll be amazed. But I've learned to never underestimate the power and resolve of central bankers. It could be years still.

I agree with what your saying, there are so many black swans circling it's ridiculous, any of these could blow it all up. I think we have a few domestic problems that could blow up pretty quickly as well, like a government downgrade, sharp rise in unemployment etc etc. I guess time will tell my friend, thanks for the reply. Cheers

thanks for this great article :) i have a very poor understanding of how the housing market actually works and found this really informative and interesting. keep up the good work!

Thanks, I'm glad you found it helpful.

Feel warmly welcomed. Just upvoted you.

If you are interested in investing in new sciences, feel free to follow my blog.

Best,

Alex