Are Tesla Shares Overvalued?

Many people have theories of money (though few are particularly good) but it's rare you hear about any "theory of shares." The most popular theory is that the share price of a company should be roughly correlated to some combination of profits, revenue, and future profits based on an assumed incremental increase in sales. Though calling this a theory seems to be an obvious overstatement. In fact, it's much more akin to an ideological belief.

These are my personal opinions and should not be interpreted as representing the views of Steemit Inc. or any other member of the Steemit Team.

Investment Ideologies

This is not to say that these numbers are irrelevant, it's more about properly characterizing the nature of these beliefs. These are far closer to culturally-originated assumptions or "cultural norms" (that culture being the culture-of-people-who-trade-stocks) than a conclusion that follows a process of logical reasoning.

Amazon

A good case-in-point is Amazon. For years people were saying that Amazon's shares were overvalued because Amazon has no profits. Those who still hold this belief are doing so in opposition to the market and years of consistent share price increases. When people refuse to recognize reality, you can be pretty sure that the underpinning of their beliefs is based on ideology. To be fair, all of our beliefs are intimately intertwined with our ideologies, so I'm not judging. But when a belief conflicts with reality it demonstrates that the ideology is a pathological one.

With respect to Amazon, since its model was incredibly original, it was perfectly reasonable to think the stock was "overvalued" in 2010 at $121. And again in 2011 at $212. And again in 2012 at $218. 2013: $312. 2014: $324. 2015: $529. 2016: $744. And finally today: $955. Now I'm not saying you should invest in Amazon. Not at all. This isn't intended to be investment advice. I'm just saying that if instead of believing that Amazon was overvalued in 2010, you had believed it was undervalued and bought the stock, you would have made an almost 800% return. In other words, we can say that with the benefit of hindsight the belief that Amazon was undervalued in 2010 would have mapped far closer to the reality of the subsequent 7 years even if that belief was irrational. On the other hand, the belief that it was overvalued consistently ran contrary to reality and that belief cost anyone who held it a lot of money to the extent it prevented them from purchasing Amazon stock.

Replacing Profits with Vision and Growth: Scott Galloway

So what is going on with Amazon stock? In the following YouTube video Professor Scott Galloway (Professor of Marketing at NYU Stern School of Business) lays out a compelling case that what Amazon has pioneered is a "new relationship between investors and companies. Simply put, vision and growth have replaced profitability... This gestalt around capital formation has moved all the way down the ecosystem. Small companies now pursue leadership over profits. Why? The market doesn't seem to demand profits from 'innovators.'"

The Myth of Value Investing

But if the market can change the manner in which it valuates companies so dramatically, what does this tell us about how it was valuating companies before? What's especially interesting is that this dramatic change isn't a novel occurrence. The last fundamental shift like this was back in the 1960s and is exemplified in the story of Warren Buffet. Buffet studied under the investment guru Benjamin Graham who developed the "Intrinsic Value Formula" which he outlines in his book "The Intelligent Investor." That equation was: Value = Current (Normal) Earnings x (8.5 plus twice the expected annual growth rate).

According to this article in Seeking Alpha, Graham admitted his "formula is only intended as an illustration, and that such projections of growth rates are never reliable... Graham also wrote extensively about the unreliability of estimates in finance. His actual framework only uses objective figures from the past - including checks for past growth rates - and requires no assumptions about the future." In other words, Graham was perfectly clear about the limits of his formula.

Buffet, being an admirer of Graham's, found that by simply applying this formula one could find plenty of stocks that were "undervalued." But what's never discussed is, "Why?" For me, understanding "capital" is the key to answering this question, as well as understanding economic systems more generally. I define "Capital" as essentially "the fruits of your productivity." When you create something of value, and you know it, you do your best to convert those fruits into something stable and useable. The most common way to store your Capital is in a currency. Currency is a monetary technology that combines Authority, Monopoly control, and anti-counterfeiting technologies to offer a stable way to store your Capital. But currency is not the same as Capital. It is simply an attempt to physically represent a totally abstract concept: Capital. Who's to say what is valuable? We do. Not me. Not you. All of us determine what is valuable by wanting it.

A Brief History of Capital

At first, refining our monetary technologies was the #1 priority. Currencies weren't especially stable and so storing your Capital in them wasn't nearly the "no-brainer" many now find it to be. It wasn't until the beginning of the 20th Century that we started to have stable currencies (due to the American adaptation and evolution of England's Central Banking technology) and it wasn't until AFTER World War II that we effectively had a global currency: the Dollar. By leveraging its position as a surplus producer as well as simply being the last man standing the US Dollarized the world creating the most cohesive global economy in history.

But it's important to remember that until 1945 most of the developed world was preoccupied with murdering one another and/or ruminating over their seemingly imminent demise! Who is going to invest their Capital in private companies when none of them, none of ANYTHING might exist in the very near future? It makes sense that it might take 10-15 years for people to start thinking, "You know what, we might just make it!" And that's when Warren Buffet came along with Graham's book in hand.

The Buffet Era

Buffet started using Graham's formula during the Golden Era of American economic growth. The world was no longer experimenting with currencies, hoping for a stable way to store your Capital and use it to buy other things. They were using the Dollar to do precisely that. So people, including the VERY newly formed American Middle Class, could now start thinking about ways to store their Capital that were inherently unstable but in a good way. They wanted a way for their Capital to be productive; for it to produce wealth all on its own. And so they turned to a form of money that had already been around for a long time (and so was trustworthy), but which had only been available to the super rich: shares in companies. Stocks.

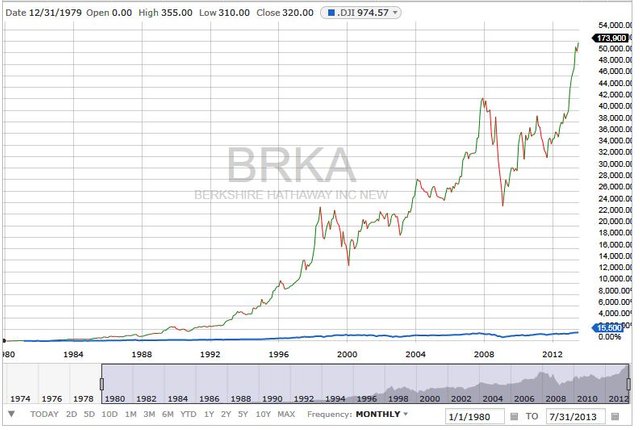

The reason Graham's formula worked was not because it was "right." He admitted as much himself when he said it was only intended as an "illustration," and that growth rate projections were both "unreliable" and "subjective." It was only meant as a guide, but for the last 40 years it has been an incredibly good guide. Performance of Warren Buffet's fund Berkshire Hathaway are a testament to that.

The Graham Delusion

But when something proves to be a reliable guide for that long of a period (a big chunk of most people's lives) it's hard for it not to become enshrined as dogma. I believe this enshrinement is beautifully illustrated in a subtle revision of Graham's book found in its newer and more popular edition. In it Jason Zweig replaced Grahams commentary and his footnotes with his own. Because of this, Graham's footnote stating, "Note that we do not suggest that this formula gives the "true value" of a growth stock, but only that it approximates the results of the more elaborate calculations in vogue," no longer appears on the same page as the equation, appearing instead at the very end of the book.

A very similar phenomenon has taken place in the related field of Economics. Most of the models which form the backbone of modern (i.e. neo-classical, neo-liberal) economics were created by people who admitted that they were based on totally unjustified assumptions. But after years of forming the foundation of a discipline, the original caveats are forgotten under a pile of new work all of which could never possibly be processed by a single person.

For specific examples, check out this great lecture by Professor Steve Keen:

I'm not suggesting that Zweig moved the footnote intentionally. I'm merely pointing out that he certainly did not think that the content of that footnote was valuable enough to include in his own footnote. Whether the change is meaningful or not, it's an interesting metaphor for the dissappearance of this information from popular thought.

Back to the Future: Tesla

All of which brings us back to the question at hand: Is Tesla overvalued? My answer to that would be, "That depends on how likely people are to view Tesla's shares as a safe and productive place to store their Capital." Now we can see why companies like Amazon and Tesla are capable of achieving high valuations despite not being profitable in dollars. This is such an important distinction. Both of these companies have lots of revenue and it's not difficult to imagine what slight changes they could make to increase their profit margins. Tesla, for example, has far more demand for its cars than they can supply, and yet they choose to keep their margins too low to generate a profit. In other words, when you store your Capital with Tesla, they put it toward building electric cars that are as cheap as possible as well as investing in other projects (e.g. the Powerwall, Solar City, etc.) so that they can create a global ... technological ... ecosystem ... built around IT.

Unprofitability is the Secret Sauce

What this all means is that the valuations of companies like Amazon and Tesla are not high in spite of their unprofitability, but because of it. They store all of the value they create in their own shares (in their own private paper) instead of dividing it up into dividends and reserves. Up until the 1950s we were mainly preoccupied with creating stable money and not dying. From there we turned our attention to "putting our capital to work for us" by giving it to companies who could leverage it to improve their productivity even further and deliver some of that additional Capital back to you as compensation for access to your funds. The most obvious implementation of this was to either return some of those profits to investors in the form of "dividends" or just store them in the bank in reserve as a reason to justify a higher stock price. But Capital stored in a bank is equally as productive for the company you invest in as when you store it in a bank: barely productive at all. Therefore, this model is still "currency focused." The company is using the fact that it either stores currency or gives some back to you as a reason for you to store your Capital with them. But in so doing they sacrifice the additional productivity that would come from using that Capital to become even more productive. Still reeling from the fallout of two World Wars, this wasn't an unreasonable sacrifice to make.

Recycling Profits

But this also created an opening for companies that were willing to challenge this norm. In another video Galloway explains it this way: "... they've figured out that they don't need to run the company for profits and once it becomes profitable it's like getting an addict hooked on heroin and there's no taking it away. So they never let the company get very profitable. Why? They don't need to. Investors don't demand it of them. As long as they can take all of that money and pile it back into the company then what's the point of being profitable? And as a result, Amazon just plays by a different game. Amazon has this reputation for being so innovative, and I would argue that all of you, if your bosses said you no longer needed to make 20% profit on every dollar you bring in, you can be break even, you'd be incredibly impressed with how innovative you can be."

Imagine it this way. Which University do you think is going to be more innovative, one with a $1 Billion endowment, or one with a $10 million endowment?

Post WWII

After WWII relatively widespread stability and middle-class growth enabled the most productivity in history to go to non-War efforts, and stocks eventually became one of the most attractive places to store all of this Capital. Adherence to formula's like Graham's were reliable for decades, but that doesn't make them "right" at least not for every stock. Out of this New Economy erupted a new kind of company. One that said, "Our goal is NOT to make an incrementally better product which will enable us to generate a sufficient profit to both compensate all of our employees and either store surplus currency in our bank account or return it to you." Instead they said, "Our goal is to alter the course of history by offering technology so powerful, that it will become a fundamental part of the future ... and you can own a piece of THAT.

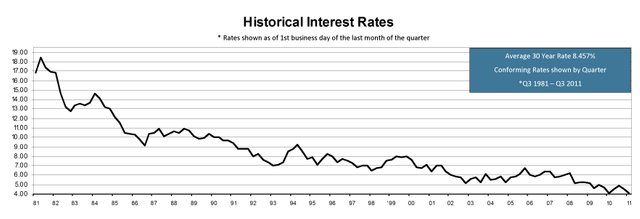

After WWII we saw unprecedented demand for both government paper/money (i.e. storing your capital in government bonds) and private paper/money (storing your capital in stocks and bonds) as confidence in both the private and public sectors were higher than ever. However, ever since then confidence in the public sector has been steadily declining as is reflected in interest rates ...

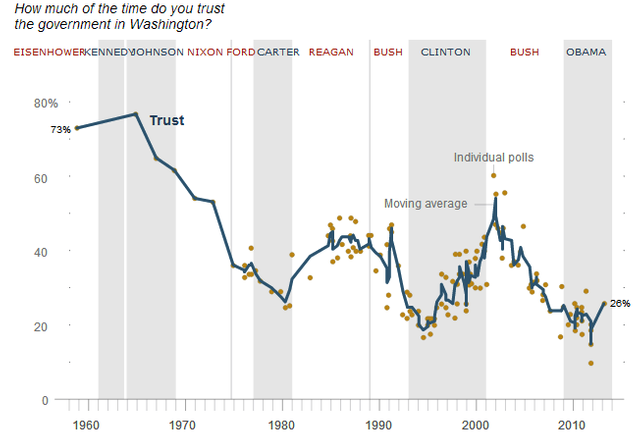

as well as more direct measures like polling ...

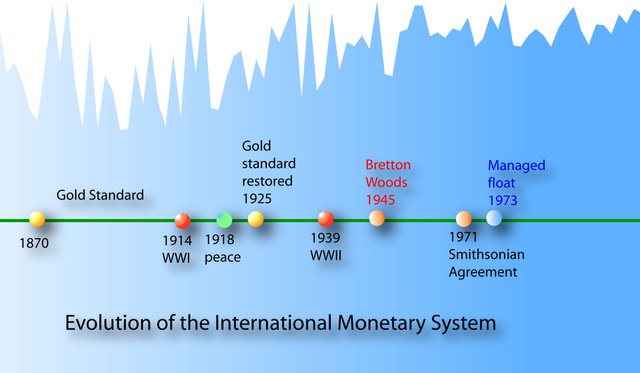

Add to this the fact that the US Dollar hasn't been able to go much longer than 30 years without requiring major structural reform ...

{kind=link}

{kind=link}

{kind=link}

{kind=link}

... the mounting deflationary pressures across the world like China's slowdown, the inevitable disintegration of the European Union, technological disruption (AI leading to mass unemployment), a looming Pension Crisis, and it should come as no surprise that people are starting to look toward private companies as long term stores for their Capital. Especially those companies which are 1. in pursuit of a grand vision of the future in which they play an integral part, and 2. who have a track record of successful execution.

For the first time in 40 years it's perfectly reasonable to expect some companies to outlast some governments

Light at the End of the Tunnel

Scary as this may be, what excites me the most about this time period (and periods like this in history) is that these are the times when the most innovative technologies emerge and take root. Many people are concerned about the potential consequences of the technologies we are about to unleash, and they are right to be fearful. But this concern is, ironically, itself a part of the cycle. The fear of adopting new technologies (thereby destroying old business models) prevents companies from embracing their innovative potential, which eliminates their ability to realize the improved productivity that would result from doing so. Instead, they fixate on incrementally improving their products which are built on old (and cheap) technology and extracting every last ounce of profits they can. This creates an opening for startups who are forced to embrace these risky, but potentially massively productive, technologies. These startups don't attract mainstream attention until a very specific event unfolds: when the old model becomes so unproductive that we find ourselves in an Economic Recession. It's then, out of desperation, that people's fear of potentially negative consequences becomes outweighed by the very real negative consequences they have delivered onto themselves.

Cryptocurrencies: The New Private Paper

The reason this is so fascinating to me, and the reason I have allowed this article to run so long, is because the conversation has very important implications for the cryptocurrency sphere. Put another way, this is why cryptocurrencies have such important implications for the world.

Cryptocurrencies are, in fact, a brand new form of private paper that merge the benefits of currency (some might list these as fungibility and liquidity, but I prefer simply "useability") with the benefits of shares in a corporation. They are shares in decentralized autonomous organizations whose goals are to create the protocols that will power the future. So the question of, "Is Tesla overvalued?" is actually the same question as, "Why do cryptocurrencies have value?" Because they're going to be around for a long time. Because they are ownership rights in a grand vision. Because they represent a stake in a better and more prosperous future.

STEEM

This is also why I have chosen to invest so much of my time, energy, and Capital into STEEM. It's why I believe personally (this is not investment advice) that STEEM certainly deserves its current valuation, and in fact a much higher one. Because I want to live in a world where everyone who shares valuable information with the public, information that enables people to be more productive, receives a fair reward (as well as a stake) in return, and I know that STEEM has already solved most-if-not-all of the technical difficulties which stood in the way of doing that. As far as I can tell Steemit Inc. in concert with the STEEM Blockchain are the only ones seriously pursuing this future, which not only makes them the ideal choice for personal investment, but also the most likely to succeed at accomplishing the task.

And I want both a stake and a say in that future

While most choose to ignore Graham's warning about the subjectivity of predicting growth, I embrace it. It is not a fact that STEEM or Tesla will grow dramatically in value, it's my subjective opinion. But I believe it nonetheless and invest accordingly.

As Steem continues to grow and spread, more and more people will be coming to this realization. More and more people will be realizing the potential of many of these decentralized-information-storage-and-access-protocols we refer to as "cryptocurrencies." While bull markets and bear markets are an inevitability of all markets, capital will continue to move increasingly toward these new and innovative assets.

The darkest hour is just before the dawn. - Thomas Fuller

Thanks for reading!

Incredible insights and connections you have drawn here. The way I look at the Amazon and Tesla valuations is that capitalism and the stock market are obsessed with short term gains. Critics need to step out of their boxes for a better view. Look just a little further down the road and you'll see something far greater than immediate gratification. Steem also is worth the wait!

Oh right! That reminds me of another thought I had the other day about this. Everyone assumes that all of the people who in invest in these companies and drive up the price are "all the stupid people." ... But what if it's the exact opposite? It's all the smart people. People who DO have long term vision. There's no way to know, but I think that's exactly what's going on. Great point, thanks for commenting DP!

Great post! I think that big part of high Tesla stock value is directly related to the founder and CEO of Tesla Elon Musk. This guy is genius! He always over deliver. He is doing what other folks think is impossible. So, in my opinion, many investors in Tesla are actually investing in CEO Elon Musk. What do you think?

100% agree. In fact, I kind of meant to include a portion where I talked about how, "Because companies like SpaceX and the Boring Company are not publicly traded, Tesla shares are actually a way for people to invest in Elon Musk himself." Something like that. So yes, agree completely.

Very insightful and intriguing post, and much appreciated. Valuation, especially in today's market can be quite a challenge. There are so many factors involved today that it's very difficult to ascertain what is the true "free market value" of a company. You're very right bringing up the flaws of Graham's basic equation for finding value in a company. I consider myself a "value" investor and have read countless books on the subject, this style fits my personality and preference to a T, but have struggled mightily over the last decade finding value in this market, everything seems to be overbought, and hence have missed out on quite a few investments that would have been profitable. Amazon and Netflix both offered great opportunities but the numbers just didn't make sense. I've waited for pull backs, as history has shown they always happen to make a more economical entry point, but this market seems to know only one way, and that is up.

I agree, after Tesla I was convinced I'd never find another opportunity like that. Fortunately crypto came :)

Couldn't agree more. Crypto is a game changer.

Excelent post, I think that there is a small bubble in equity

I agree we could see as much as a year long pull back, but longer term I don't see many other places for capital, especially institutional capital, to go. Great comment!

In longer term is difficult that the money cashflows not to go to equities, but in short and medium term, even some companies could disappear because of the capital outflow of them

Just in time. At the moment writing about money as a consumer product that's ripe for innovation. It's been a dead thing ever since it was created so long ago :)

Another thing to consider is Tony Hsieh's concept of Return-On-Community instead of Return-on-Investment

Yes, great point. Most people fail to appreciate that money is just another technology. When people forget that something is a technology that can be improved, that's usually a sign that it's ripe for disruption.

Love this. As usual your blog posts are excellent. I remember a couple years ago I was reading an article about Amazon in which the author was calling for Bezos' head (along with some activist investors I believe) and I thought out loud in the comments section, "anyone who thinks they can replace Bezos at Amazon is severely deluded." The author deleted my comment lol. But it's exactly what you illustrate here that caused me to have that thought. Bezos sees the future and takes everything he makes and puts it back into his business to create that future. Investors who are constantly looking at quarterly reports don't get why that's good because they've never actually run a growing business before, not even a failed one. It's sort of like the old "you've gotta spend money to make money" adage, but slightly more nuanced of course.

Thanks so much for the kind words. Yeah, I've had very similar thoughts with respect to Tesla. People would make these arguments that basically implied that Musk was an idiot and I was like, "You think YOU'RE smarter?!" That's a self-defeating argument right there! There are many valid criticisms of Musk, that he isn't incredibly competent and intelligent just isn't a credible claim.

Good post @andrarchy! After having recently heard about Steem I'd definitely buy this over the bigger names out there - especially Tesla. Just read this article over at BI (http://www.businessinsider.com/wall-street-is-wrong-about-ford-stock-price-2017-5) and it's amazing the comparison b/w Ford vs Tesla. Tesla is a disruptive technology but is it sustainable, compared to a heavy-weight like Ford...and WallStreet looking for quick profits in this up-down economy is starting to make some erroneous oversights. Let's see how that turns out but I gotta learn more about blockchain now!

Welcome to Team Steem! ;) No businesses last forever and Ford is living on borrowed time. They won't survive the next technological revolution. Tesla is better positioned for that and I think in 10-20 years it could be a trillion dollar company. That's what I look for, companies I believe could become a trillion dollar company. Even if the odds aren't especially high. Great comment! Thanks for reading! Welcome to Steemit!!!

I like your viewpoint! Yep, all these older stalwarts look like they might just "maintain" the lower end of the market with the boom growth coming with new-age tech (about friggin' time personally! I mean flying cars anyone?)...looking forward to your future pieces - especially looking towards this new blockchain environment (I'd honestly thought it was strictly for programmers when bitcoin first came out), hope to get involved this time around!

Yep, got to bet on the "coulds" and "mights", that's where the biggest potential ROI lies. Love it!

Might be your greatest article. Maybe because I love reading more than listening to video but I learned a lot and it's a nice perspective here.

But buffet took graham to a whole different level and his theory is much more sophisticated and based on 50 years of experience [ that graham did not have].

You can read stuff that buffet said and munger said...10-20 years ago and find nuggets of truth, even prophetic i'd say. Also, Buffett really walks the walk.

I'm only saying this becaue IN FACT all those companies would probably be berkshire investments if they did tech - amazon especially - because the fundamentals are right, the team is right, the vision is there, the product etc...

Also, AMAZON is about to kill it.

I hope it can still grow, it's hard to grow and innovate when you kill it, as we've seen from apple how is kind of stagnant for now [ maybe the apple car will give it a new breath of fresh air ].

Cryptos will be as good as the team behind them. Fundamentals, man :)

It's good that Steam is partly ...well, you.

Walk the walk.

I got nothin' against Warren, in fact I own some Berk.B :)

Glad you liked it. You're too kind! [:blushing:]

:) I'm surprised of your level of knowledge too.

keep it up!

A recent report about Elon Musk conveyed the message that he was overworking his employees. They have been working along side robots and having work related injuries and sickness due to high productivity demands and long hours. Bad management kills.

inspire info...thanks