FT Rebuttal: Part 8 - Non-Performing Assets (NPA’s)

Non-Performing Assets (NPA’s)

Authored by jain and govil - astute political observers

Modinomics is yet to deliver – was the Op-ed written by the Editorial Board of Financial Times published from London -(https://twitter.com/ft/status/1069894756929585152. They have raised the following issues in the article.

- Modinomics yet to deliver to many (https://steemit.com/financialtimes/@ajain/ft-rebuttal-part-1-assessing-how-modinomics-has-reached-the-poor)

- Failed infrastructure overhaul (https://steemit.com/india/@ajain/ft-rebuttal-part-2-assessing-failed-infrastructure-overhaul)

- Failed attempt to turn country into a manufacturing powerhouse (https://steemit.com/india/@ajain/ft-rebuttal-part-3-assessing-make-in-india)

- Demonetization ineffective (https://steemit.com/india/@ajain/ft-rebuttal-part-4-demonitization)

- Economic growth squandered away on symbolic projects (Statue of Unity) (https://steemit.com/india/@ajain/ft-rebuttal-part-5-economic-growth-squandered-away-on-symbolic-projects)

- Fudging statistics (https://steemit.com/india/@ajain/ft-rebuttal-part-6-fudging-statistics)

- NPA’s (Non-Performing Assets of Banks)

- RBI Fracas (Reserve Bank of India) (https://steemit.com/politics/@ajain/ft-rebuttal-part-7-the-rbi-reserve-bank-of-india-fracas)

We have initiated a series of eight articles where each issue raised in the Financial Times Op-ed as listed above, will be taken up and put under the microscope of facts and data to critically test the validity of the statements made.

In this article, we review the story of NPAs in India.

Bad debts or unrecoverable loans are an inherent part of the business risk for the banks, as well as for the entrepreneurs. The loans are taken in good faith by entrepreneurs and are sanctioned in equally good faith by the bankers. Of course, there are loan processing norms that the Banks follow. If thereafter the loan goes bad in due course, it is a fair business risk. And, the same is considered delinquent but not a fraud. In other words, it is an offense all right, but a much milder form of offense than a fraud. In banking terms, all these bad loans are termed as Non-Performing Assets (NPAs).

The problem of NPAs came to center stage within a short time span from the time the Modi government took charge in May 2014. This article is all about what were the causes that created large NPAs and how the government went about tackling the same. We study and analyze the problem through the prism of following subsections.

1. The Magnitude of NPA Crisis

2. Major Causes For Unprecedented Levels of NPAs

3. What the Modi government did to tackle the problem

Let’s begin in the right earnest and examine each section in detail through the microscope of hard-core data and facts.

1. The Magnitude of NPA Crisis – India’s Lehman Moment

If NPAs are a part of the inherent risk for Banks as well as Entrepreneurs, as mentioned in the opening dialogue, then what is this whole noise about NPAs in India? The RBI, the Government, the Banks, the Entrepreneurs, the Financial markets, all are worried. Even the authors of this article call it the ‘Lehman moment’ of India’s financial crisis (We used this expression in our previous article – RBI Fracas. Article 7 above.). So what is the ground reality? Let’s get an understanding of the same.

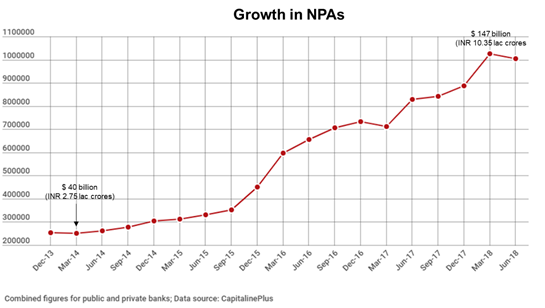

The problem has reached crisis proportions due to its sheer magnitude. The NPAs have ballooned to unprecedented levels. Modi government inherited this problem of NPAs when they were sworn in May 2014. As per the officially stated position in March 2014 the magnitude of the problem was supposed to be around $ 40 billion (INR 2.75 lac crores). Once the new government started to dig deeper and deeper into the NPAs, with a view to cleaning them up, the government realized it was a shifting goal post. In no time the figures started to balloon, and as of 31st March 2018, as per the Finance Minister, NPAs stood at $147 billion (INR 10.35 lac crores). It posed a serious challenge by threatening and undermining the entire Banking system. Any negligence or a misstep by the Government, and the entire faith on banking system would have collapsed. The following chart gives the story of how NPAs kept ballooning from March 2014 onwards until March 2018.

2. Major Causes For Unprecedented Levels of NPAs

Having understood the magnitude of the problem, it is time to understand what lead to the crisis and how it got precipitated. The causes of NPA crisis are multifold. Following are the reasons that lead to the crisis.

- i. Indiscriminate lending

- ii. Evergreening of Loans

- iii.Dereliction of duty on oversight by the regulatory body (RBI)

We take up these points one by one and examine what happened.

i. Indiscriminate lending

The phenomenon of indiscriminate lending happened primarily under the previous government - UPA 2. In wake of world financial crisis in 2008, the then Government run by Congress party (UPA 2) encouraged the banking industry to step up loans in order to push economic activity. If need be, even relax the norms here or there. In itself, this was not a bad move. However, due to the DNA of corruption, favoritism, nepotism of the government, the whole exercise degenerated into downright frauds in no time. The conniving and corrupt bankers, bureaucrats, politicians, and businessmen colluded to take loans even when there was no business case for the same. Smelling easy money, loans were taken and given like there was no tomorrow. The loans were given under political pressure (not in good faith). And the banking norms were not just relaxed, they were almost bypassed, disregarding common banking prudence. As a result, in a short span of five to six years (2008 to 2014), the loans of public sector banks ballooned from $260 billion (INR 18 lac crores) to $743 billion (INR 52 lac crores). Imagine, in the first sixty years of independent India (1947 to 2008), the banking industry evolved to a level of credit to the tune of $260 billion. And, in the next six years!, yes six years (2008 to 2014), this credit multiplies almost three times to reach a figure of $743 billion. No wonder, more than 20% of these loans became NPAs in due course.

ii. Evergreening of loans

As if the crisis in itself was not enough due to the sheer magnitude of the NPAs, the government adopted diversionary tactics of preventing the real picture from coming out on record. This was done through evergreening of loans, or ‘Restructuring of loan’ as the bankers would like to call it. For the benefit of the readers, restructuring is nothing else but relaxing the terms of payment – extended time for repayment, waiver of interests or lowering of interests or a combination. As a result, the loan no longer shows up on record as an NPA thereby artificially depressing the overall NPA number. Imagine, this was being done in full knowledge of, and, with the approval of government officials and political bosses. The Finance Minister in his budget speech in Parliament on 1st February 2019 made a statement that the actual NPAs on the March 2014 was probably double of what was shown on record (Shown $40 billion – INR 2.75 lac crores. Actual $80 billion – INR 5.5 lac crores). The figures were suppressed through the Restructuring schemes.

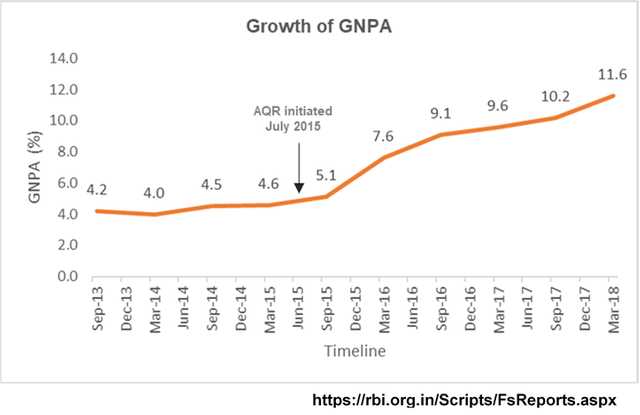

This point about ‘Evergreening of loans’ is proven beyond doubt when one studies the NPA data from a historical perspective. It would take a person to be blind to miss the data. The GNPA figure went up from 4.2% in September 2013 to 11.6% in March 2018. See the graph below. (All data in the graph has been taken from the six-monthly FSR's of RBI from December 2013 to June 2018. URL link for reports is given at the bottom of the graph)

The key point to be understood here is - why was the GNPA going up. It was obviously going up due to Asset Quality Review Exercise initiated by RBI at the behest of Modi Government. The data is very evident. See the graph showing a steady climb from July 2015 onwards. The AQR exercise was initiated in July 2015. From a level of 4.6% in March 2015 the GNPA goes up to 11.6% in March 2018 (a timespan of just three years). These were obviously the NPAs arising out of loans sanctioned and disbursed prior to 2014 (in fact during the period 2008 onwards up until 2012 or so). All these were brushed under the carpet by the banks and were not declared as NPAs. While all this was happening, the regulator RBI was either sleeping or working to the tune of the then government by deliberately looking the other way.

iii.Dereliction on oversight by Regulatory body (RBI)

The moot question then arises, how could the system be subverted with impunity. After all, there are checks and balances in place. There is a regulatory body RBI at the apex level. In this context, it becomes important to examine how well RBI discharged their oversight function? And, the follow-up question - what did the RBI do when the NPAs started going up? If one studies the Financial Stability Reports (FSR) prepared by RBI every six months then one realizes that data was available with RBI, the problem was crying for recognition, but for strange reasons, RBI did not take actions in a befitting manner. We study some of the data points below.

In the FSR of December 2013 RBI shows a sharp increase in the NPAs. The NPAs doubled from the previous FSR (June 2013). See excerpts below (reproduced from page 23 of the December FSR):

Looking at another data point in the same report (December 2013 FSR page 29) we find that the GNPAs went up from 3.4% to 4.2%. This was significant. But what was even more striking was the fact that the percentage of Restructured advances to Total advances in Public Sector Banks was more than 50%. The relevant section of the report has been reproduced below. (Remember the evergreening point above!)

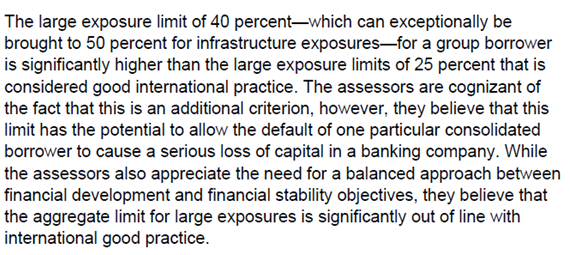

Another significant point emerging from the December 2013 FSR report was the observation made by the IMF and World Bank. These two world bodies had assessed India in 2011 – 12 under the ‘The Financial Sector Assessment Programme’ (FSAP). In their finding they assessed India to be “materially non-compliant” (MNC) vis à-vis the Basel Core Principle 10 related to “Large exposure limits” (See page 25 of the December 2013 FSR of RBI). The appropriate section from The IMF, World Bank Group FASP report is also reproduced below (8Source: https://www.imf.org/en/Publications/CR/Issues/2016/12/31/India-Financial-Sector-Assessment-Program-Detailed-Assessments-Report-on-Basel-Core-40891*).

The matter was set right after the elections by Modi government. It would be appropriate to know that RBI was requested by the Government (December 2014/January 2015) to do a detailed ‘Asset Quality Review’ (AQR), special emphasis on restructured loans, pursuant to the Annual retreat of head honchos of Public Sector Banks in December 2014 in Pune. The retreat was attended by Prime Minister Modi also. And, the government came face to face with the real magnitude of NPAs, and reasons for the same, for the first time.

The point was not lost on the Comptroller Auditor General of India (CAG) – Mr. Rajiv Mehrishi. He publicly questioned the slippage on part of the RBI.

It is evident from the above that data points were available with RBI indicating seriousness of NPAs with Public Sector Banks. Yet, no significant efforts were made towards mitigation of the risk or to initiate measures to tackle the problem. Such a faux pas may have been caused at RBI end by the fact that 2014 ‘General Elections’ were around the corner, and the political bosses may not have been much keen on tightening up the situation. But RBI is an autonomous institution? How come they never acted on it? Or is it that the RBI acquiesced under pressure from political bosses?

3. What Modi Government did to tackle the problem and the results thereof

Having understood the problem, and why it happened, it is time now to examine how the Modi government went about tackling the same and how effective they were in their endeavors.

The Modi government took a comprehensive view of the problem. The action was taken on the following dimensions:

- i. Reinforce the legal framework

- ii. Strengthen credit information availability

- iii.Diplomatic initiative to extradite defaulters from abroad

Each of the above three points and the actions taken thereof, are studied in details below.

i. Reinforce the legal framework

It was a well-known fact in India that the legal framework was extremely lax when it came to handling errant defaulters on economic offenses. In fact, the ease of doing business report 2019, brought out by World Bank, identifies ‘Enforcing Contracts’ and ‘Resolving Bankruptcy’ as areas for improvement in India. The worst was that the defaulters were fully aware of this lacunae and took full advantage of the same. Myriad of cases would get filed against defaulters but judgment and prosecutions would be rare if any. Litigation took years and recoveries would be very few. Ensconced in this comfort zone, the defaulters, in connivance and collusion with bank executives and politicians, played havoc with the system.

It was a do or die situation for Modi Government. Unprecedented levels of loan defaults, a group of defaulters not averse to taking the banks for a ride (many of these defaulters were large corporate houses of India), and facing the possibility of erosion of faith in the banking system among the average citizen, the Modi Government decided to act tough. As the saying goes – when the going gets tough, the tough get going. A legal framework was swiftly put into place by the government, and operationalized in double quick time as well. This took the defaulters and conniving officials by a complete surprise. As a result, while the errant were mocking the operations and time involved for action, many among them started to get notices and calls with proper legal sanctity.

The Government set up an ‘Insolvency and Bankruptcy Board’ (IBBI) in October 2016 and armed it with a legal framework in the form of ‘Insolvency and Bankruptcy Code 2016’ (IBC). IBBI is mandated to operate as a regulatory body for the entire ecosystem of insolvency infrastructure and mandated to evolve the entire insolvency set up in a smooth and efficient manner.

Another important step by the government was to set up a ‘National Company Law Tribunal’ (NCLT). This was set up in June 2016. The NCLT is the adjudicating body for insolvency cases. It is an empowered Tribunal and ranks equivalent to a Civil Court. Today NCLT operates through 12 Benches pan India. Each Bench has a set of States under its jurisdiction.

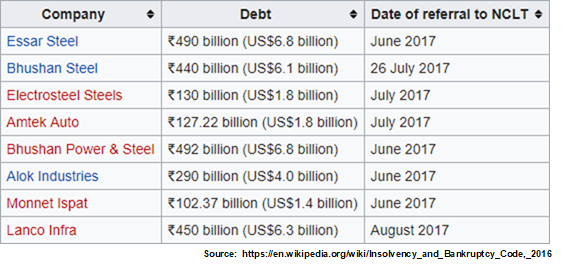

Armed with these provisions and an adjudicating body, with proper legal empowerment and extensive reach across the country, the government was firmly in the saddle to handle insolvency and bankruptcy. The IBC also provided for some stringent timelines for resolution. Things started to happen at a very brisk pace. The initial referrals to NCLT for insolvency proceedings came through RBI. Some of the high-value cases of NPAs referred by RBI for the resolution to NCLT are as below:

All this has instilled some fear in the defaulters and evoked in them a respect for the law. The defaulters realized they could end up losing their ‘Crown Jewels’ if they do not pay up and kept playing the hide and seek game. They were rudely shaken out of their lackadaisical approach and started to make efforts to settle their pending loans. Who would have thought that such a transformation could have taken place in India? And that too within a short span of three to four years. The following visual says it all.

ii. Strengthening Credit Information Availability

RBI maintains a central database on big borrowers - Central Repository of Information on Large Credits (CRILC). In view of unprecedented levels of NPAs, it was decided to strengthen the database. Based on the recommendations of Deosthalee committee it was decided to set up a comprehensive Public Credit Registry (PCR). The PCR will be an extensive database of credit information for India. It will capture all relevant information in one large database on the borrower, and in particular, the borrower’s entire set of borrowing contracts and outcomes. Further, the PCR will also gather information from entities like market regulator Securities and Exchange Board of India (SEBI), The Ministry of Corporate Affairs (MCA), Goods and Service Tax Network (GSTN), Insolvency and Bankruptcy Board of India (IBBI), Central Registry of Securitisation Asset Reconstruction and Security Interest (CERSAI), Central Fraud Registry, Utility Billers etc. Banks, Financial Institutions, and other bona fide stakeholders will be able to get 360-degree information of the existing as well as prospective borrowers on a real-time basis. Once implemented, PCR will ensure that credit would be provided to borrowers based on the study of exhaustive information on their profile and past history. This would go a long way in reducing the risk of loans becoming NPAs in the future.

The government has moved swiftly towards the implementation of PCR. Tenders were floated and after preliminary discussions and assessments, a short list of vendors has been drawn. The contract would be awarded to the finalized vendor from among the shortlisted vendors.

iii.Diplomatic Initiative for Extradition

The efforts by the government of India to bring the defaulters to book, and recover legitimate dues, extended beyond the frontiers of our country and our national borders. The government pursued diplomatic and legal initiatives to extradite defaulters who had escaped from our country.

Perhaps, the most high profile case on this front has been that of Mr. Vijay Mallya, the Chairman of the UB Group, a very well known industrialist in India. The case caught the imagination of people and has remained in the high visibility category all these years. Though the value of default is not so large compared to other large value NPAs – about $1.5 billion (INR 10,000 Crores) only, it remains high profile more due to the flamboyant lifestyle of the person concerned and his high voltage presence on social circuits in India and abroad. In connivance with ‘The Swamp’ in India, Mallya escaped from the country in the nick of time (days before he would have been arrested) leaving the government red-faced, and the rival political parties accusing the government of deliberately helping the industrialist escape from India. Mallya fled the country in February 2016.

Stung by the criticism, the government left no stone unturned in trying to extradite Mallya from the UK to India over the last three years. Not a very easy task. And, the efforts of the government paid dividends when they succeeded in getting the British courts to pass an order in December 2018 for the extradition of Mallya to India. (The following headlines have been reproduced from a leading Indian financial daily – The Economic Times).

Mallya has not been extradited as yet. There are some procedural formalities remaining and the possibility of him going into appeal. But going by the track record of Modi government, where they have extradited in the recent days, some of the people who were involved in criminal offenses and frauds, one is confident that the government will succeed in bringing Mallya to book.

By no means, Mallya is the only case to be followed up abroad. There are other cases also which are being pursued and are at differing stages of action. Nirav Modi, Mehul Choksi, Sandesara, etc. – are some of the other cases that are under pursuit. But suffice it to say it has had a salutary effect on defaulters wanting to opt for settlements rather than planning their escapes or playing cat and mouse games with banks or enforcement agencies. Mallya himself has issued statements that he would want to settle the loan and seeks a waiver of interest. The government, of course, has been cold-shouldering it.

As we can see from the above analysis based on data and facts, it is an order of magnitude achievement by the Modi government. In the wake of all odds, the government has pulled out a success story. The country has been pulled back from the brink of disaster. And all this while also going in for building a resurgent India, high GDP growth, huge infrastructure investments, a massive upliftment of the weaker sections of the society. It is salutary work by any yardstick. Even the Op-ed is unable to negate it. But in line with their prejudiced mindset, they call these enormous efforts and results as ‘Some Successes’ only. What a pity?

=====

We work hard to research the topic and collect data points to form a narrative. So, if you like the article please

Good analysis

Just as I finished uploading the article following news hit the wires:

UK home secretary approves Vijay Mallya's extradition to India

Read more at:

http://timesofindia.indiatimes.com/articleshow/67837731.cms?utm_medium=referral&utm_campaign=iOSapp&utm_source=WhatsApp.com&utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

Fixed a couple of typos and reposted.