Philippines Tax Updates: Personal Income Tax (TRAIN LAW)

Amendments to the Tax Law and How it will Affect You

It has been clearly manifested in the past how income tax is so complicated making it hard to understand. The Tax Code of 1997 have several tax provisions and tax exemptions. It is so complicated that even an accountancy student ends up crying in taking taxation subject in their undergrad; how much more to an ordinary citizen. With this problem, the government strive to do its best to maintain a fiscal discipline and adhere to the true principles of taxation: Simple, Fair, and Efficient.

The Philippines, having the 2nd highest income tax in ASEAN, have amended its 20 year old Tax Code as promised by its current president during his electoral campaign. TRAIN law has come into existence. With this let us try to compare and understand this new amendments and how it will affect you (pure compensation earner, self-employed and professional, and mixed income earner).

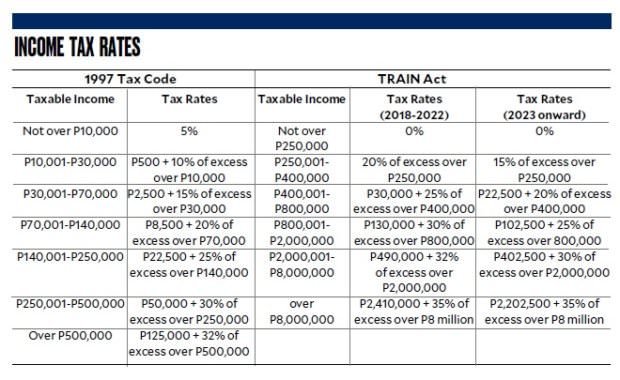

1. The Income Tax Table - Individual

What are the major changes?

The major change that can be seen between the old and the new tax table is the increased amount in the taxable income bracket and tax rates. The new tax table somewhat reflect the current value of the income of taxpayers compared to the 20 year old previous tax table.

Personal Exemption = Php 50,000

Additional Exemption = Php 25, 000/dependents limited up to four. (Max. of Php100,000)

In the Old Tax Code an individual may claim a personal and additional exemption but in the TRAIN Law such exemptions were removed. Moreover statutory deductions (SSS, GSIS, HDMF, Union Dues) are retained except for PPHHI1 (Premium Payment on Health/Hospitalization Insurance) has been repealed/removed. So what are its effects?

1 PPHHI can be claimed as a deduction (2,400 per Family per year) in the old tax law if the gross family income does not exceed Php250,000

A person that is:

Pure Compensation Earner can Claim

| Old Tax Code | TRAIN Law |

|---|---|

| Personal Exemption | None |

| Additional Exemption | None |

| Statutory Deductions | Statutory Deductions except PPHHI |

Example: Single Pure Compensation Earner with four dependents and Annual Gross Income of Php 200,000.

| Old Tax Code | Amount | Train Law | Amount |

|---|---|---|---|

| Gross Income | 200 000 | Gross Income | 200 000 |

| Personal Exemption | 50 000 | Personal Exemption | None |

| Additional Exemption | 100 000 | Additional Exemption | None |

| Statutory Deductions | 7 400 | Statutory Deductions2 | 5 000 |

| Taxable Income | 42 600 | Taxable Income | 195 000 |

| Income Tax Due | 4 390 | Income Tax Due | -0- |

2Statutory deduction of 7400 is a presumed amount. 7400 less 2400 annual PPHHI deduction equals 5000.

With the example you can now see the big difference brought by the new Tax Law. To fully understand, since I cannot make as many examples as it would be lengthy, is to simplify the comparison between the two.

Let us compare the two at their extremes

Maximum amount that can be claimed as Deductions

| Old Tax Code | Amount | TRAIN Law | Amount |

|---|---|---|---|

| Personal (H & W) | 100 000 | Personal | None |

| Additional (4 Dependents) | 100 000 | Additional (4 Dependents) | None |

| Statutory | xxx | Statutory | xxx less 2 400 |

*H & W stands for husband and wife

From this table you can now easily compare the two and tell what are the impact of this new tax scheme.

The old tax law enables both spouses to claim a maximum amount of deduction to their income at an amount of Php 200, 000 plus statutory deduction. While in the new tax law you might think that the only deduction is the statutory deduction if you failed to see that in the new tax law the first 250,000 is zero rated (0% tax). It is as if 250, 000 from both of them will result to a somewhat 500, 000 tax free earning (250 000 from husband and 250 000 from wife).

2. Tax of self-employed and professionals

Self-employed are individual taxpayers whose income are solely derived from his own business while professionals are those people that derive income from the practice of their profession.

In the old tax law SEP (self-employed and professionals) paid their income taxes based on normal tabular income tax only ( the tax table on the top). But this is not the case anymore with the amendment stipulated in the new tax law (TRAIN Law).

The major change that is newly introduced is that:

Self-Employed and Professional earning NOT more than Php 3 Million

Have the option to:

- Pay a flat rate of 8% tax base on gross sales/receipt and other non-operating income in excess of Php 250 000, in lieu of the graduated income tax rate and percentage tax (3%).

- Pay Percentage Tax and Regular Income Tax rate using graduate tax table.

Since SEP has now the option to choose as to how they will pay their income tax, the withholding tax for SEP had also adjusted. From 10% withholding tax for SEP earning below 720 000 and 15% withholding for earnings more than 720 000, the new withholding tax rate is now 8%. Flat rate 8%, Withholding rate 8% so now its balanced.

EXAMPLE: A person that is:

An SEP earning Php 500,000 annual sales with Php 100 000 Business expenses (single with 4 dependents)

| Old Tax Code | Amount | Train Law | Amount |

|---|---|---|---|

| Gross Income | 400 000 | Gross Sales | 500 000 |

| Personal Exemption | 50 000 | Personal Exemption | None |

| Additional Exemption | 100 000 | Additional Exemption | None |

| Taxable Income | 250 000 | Taxable Income | 250 0003 |

| Income Tax Due | 50 000 | Income Tax Due | 20 000 |

3500 000 less 250 000 = 250 000.. 8% tax rate based on in excess of 250 000.

3. Mixed Income Earners

Mixed income earners are those individuals who are deriving income from employment and doing business. He is a compensation earner and a SEP.

The Mixed Income Earner in the new tax law will be taxed accordingly:

A. His compensation income will be taxed based on the graduated table

B. His business or professional income will be taxed like that of the SEP having the two options if his business is earning NOT more than Php 3 Million.

4. 13th Month Pay and Other Benefits

13th Month Pay and Other Benefits increase from Php 82 000 to Php 90 000.

If the benefit and bonus totaling up to 90 000 is not subject to tax. Other de minimis benefits that exceeds their limits can be added as other benefits in the 90 000 ceiling. (See Revenue Regulation 10-2008)

Sources :

Open for corrections. Please comment any questions that you would like to ask. Feel free cause it is free.

My next post will tackle the impact of TRAIN to minimum wage earners and Amendments to Final Taxes.

Stay Tuned because my Internet Connection is back.. Oh by the way, Our landlord really sabotage us. He don't want us to have an internet connection. Though we secure to have an internet connection the problem again is that he don't want to see internet cable wires in the lobby so no choice we stick to WIFI.

Thanks! very informative!

Thank you for the appreciation :)

nice one

if I am doing crypto, then there will be no tax at all, i think

The general rule is that all income from whatever sources (legal or illegal) are taxable.

In the Philippines, there is no clear guidance as to the treatment of crypto income. But if someone is to claim that crypto is exempt from taxes one must prove that such exemption is clearly indicated in the law or executive pronouncements. As of the moment I think crypto income falls under regular taxable income (the tax table above applies). But since taxes are self assessing it is hard to trace and assess such crypto by the authorities so you can evade paying tax on crypto income hahaha

But then again we do not "earn". We are being "rewarded". I'm not an expert, I'm also curious. In my opinion, rewards are more like gifts than income. So if your mother gave you 300,000php do you pay tax for receiving the gift (being rewarded for being a nice child)?

The answer is yes. There is what we call donor's tax. A tax imposed on the transfer of property/rights over a certain thing whether it came from a relative or a stranger.

You are rewarded, its true. Gifts are given out of generosity and given without any consideration in exchange. But, I beg to differ that your rewards are being earned thru hard work and dedication. And try to define "reward" and you will see its just the same, look at its synonyms.

I see, thanks for the clarification. Do people above 18 who still receive "baon" in college have to pay the so-called donor's tax?

I know the synonyms. reward -> incentive/compensation -> pay

No. There is a difference between support and donation. Every parent has an obligation to support their children specially with their necessities. A gift like car, house and lot, and large sum of money that may prejudice other children are things that are somewhat subject to this donor's tax.

That's really helpful. Thank you so much.

I'm going to assume you're from the Philippines. Do you have any info/article/etc about how we're supposed to go about our steem "earnings"?

Maybe this can help.

https://steemit.com/philippines/@paulthebeloved/philippines-steem-and-steemdollars-sbd-taxable-or-non-taxable

since there is no law about cryptocurrency here, still it falls to non_taxable, hehe

20,000 php income a month will have 0% income tax in 2018 table, still I have no tax on it

IRS of America issued a ruling that cryptos are assets and is taxable. Here in Ph, the rule of taxation that all income are taxable applies. Crypto income are taxable but the problem is how to extract the taxes since blockchain is hard to understand hahaha and peoples are the one who file and pay the authorities will have a hard time assessing the proper amount of taxes. It is just like gambling winnings. Gambling winnings are taxable but the question is who wants his winning from gambling to be taxed? haahaha so do not declare it as other income.. BIR only need to move and bwalah maybe one day crypto will be taxed if the government cannot benefit or extract taxes then maybe one day it might be banned hahahah.

Is it true that there is a Crypto Trading Platform (like Bittrex, Binance, Poloniex etc.) in the Philippines in cooperation with coins.ph?

Congratulations! Your post has been featured!

I am deeply honored :)