Is Financial Planning All One Big Lie? Part 2

In yesterday's post, Is Financial Planning All One Big Lie? I showed the numbers behind what traditional financial planning's results were if you invested 10% of your income in stocks or half stocks/half bonds for 40 years.

I showed the effect of a 1% fee as a drag on performance as well.

In this post, I am showing you a slightly different, more realistic scenario:

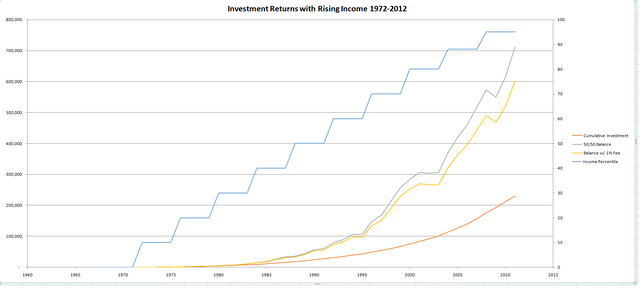

This chart addresses one of the main objections to the kind of analysis I presented yesterday. Namely, that you don't make the median income your whole life. Early in your career you lack skills and experience. Later in your career you have skills, experience, and seniority. So the typical career path is one of rising income.

Of course we are ignoring periods of potential unemployment, health problems, and other adverse events that can derail this train.

Let's look at this rosy scenario.

Methodology

We are looking at the same 40-year time period as yesterday's post in order to keep things as similar as possible. And instead of taking 10% of the median income each year as the proposed investment, we are stepping up where this person falls in the income distribution every 4 years. You can see this in the Income Percentile that is a stair-step function. Years 1 through 4 of the career are at the 10% level, 5 - 8 at the 20% level, etc all the way up to the 95% range (the highest I have data for) in the last 4 years of the career. Each year, 10% of the income is saved and invested in the 50/50 stocks/bonds portfolio.

I chose the 50/50 portfolio for simplicity since we saw it had better performance in yesterday's analysis.

I also included the numbers for the 1% fee drag as well.

Results

So what do we see?

Well, because of the later years' higher income, the cumulative investment is higher than in the constant median income scenario. But the overall returns are 260k less! You only end up with 711k in total assets compared to the constant median income scenario's 971k in assets!

In the 1% fee version, returns go from 758k down to 600k.

Let's think about this in a retirement perspective for a second. In this scenario, the highest earning years are at the end of the career. So imagine you are making that 95th percentile income, which in 2011 was 186k. And then you plan to retire with a nest egg of 711k? Plus some social security? That either means cutting your lifestyle from 167k down to 50k (28k from 4% of investments + 30k from social security) or blowing through the whole balance of in a few years.

From my observations with clients, it's the latter case that people tend to choose. Very few 401k balances, such as they are, survive past the first few years in retirement.

In the 1% fee scenario the numbers are just that much worse.

Objections

The supporters of this kind of traditional financial planning have some objections ready to go like:

Taxes will be lower in retirement because of lower income

First off, we don't know what tax rates will be. We do know that deferred compensation plans like 401ks and IRAs count as ordinary income. Plus a portion of your social security income will probably be taxed.

It's OK to earn less because your expenses will be lower

This is basically an admission that it's a plan to be poor.

People just need to invest more than 10%

Let's get real. Very few people even manage to save 10%, much less more than 10%. Part of that is Parkinson's Law (aka lifestyle inflation), part of it is rational economic choice. We all know that the financial markets are very volatile. It's a scary thing to see swings up and swings down in the market and have that increase your confidence to invest more money.

They should have used a Roth

This one I kind of agree with. If you have the choice, a Roth 401k or Roth IRA is a better choice because of the tax treatment. The flip-side is that it's not an even comparison because the tax deferral means you can invest more in traditional 401ks and IRAs in the current year than you can in a Roth. So if you were to invest 10% of your income in a 401k, you might only be able to do 7.5% in a Roth 401k.

Also, while most people have Roth IRAs available to them, Roth 401ks are relatively rare.

What about the company match?

Over the course of history, company matching contribution funds was rare. It's more common now, and up to 40-something percent of companies that offer a 401k offer some sort of matching. So that will boost your returns.

But again, let's be real. Where did that money come from? That's money that the company could have otherwise paid you. It's all part of your compensation as far as the company is concerned. It's more advantageous for a company to offer a big match than to actually pay you more because a large chunk of employees will not maximize that benefit. So the employer can keep the difference.

People should just make more than the median, or start off higher in the distribution

Well that's changing the goal posts, isn't it? The promise of the story is that anyone, if they save and invest diligently, stay the course, etc etc can amass a comfortable retirement account and live in comfort and dignity.

So yes, if you make than average all through your career you will do better than average. Duh! It still doesn't solve the lifestyle inflation problem or the fact that it's a plan to be poor relative to where you end up in your career at retirement age.

You only looked at one 40-year period

That's true. We could look at a rolling 40-year window to get a better global view. But here's the thing, the numbers aren't THAT different. Yes, we've had a hell of a bull market the last few years that would make starting in 1975 better than 1972. And you don't get to pick when you're born, when you come of age in the work force, and when you retire (for the most part). So cherry picking starting in one year over another is just luck of the draw from when you were born.

If you start this analysis in 1972 you end up with 711k. Start it in 1975 and you get 879k without fees or 600k vs. 742k with a 1% fee built in. So you should have been born in 1950 instead of 1947 to reach age 25 in a slightly better economic climate.

The Bottom Line

The traditional line of get a nice job, save 10% of your income, invest for the long term does not yield the results that people are promised.

Upvoted ($0.19) and resteemed by @investorsclub

Join the Investors Club if you are interested in investing.

Great insights and experience. The world is changing. How much should our investment strategy change to match?

Upvoted by the growing TIMM trail and resteemed. Soon you'll be able to post these articles on TIMM, a new Steem based interface designed especially for traders, investors and analysts, complete with tools to help you monetize your expertise. Check out our recent announcement.

That’s the million dollar question

Here's our new Discord channel invite, so you can join us there.

Great insights, @nealmcspadden. Let me speak about the idea that taxes will be lower in retirement. If you rely on your retirement savings, such as a 401(k) or IRA, there's a large chance that your taxes will be more in retirement than they were when you were working. Here's why:

As you mentioned, those 401(k) and IRA contributions that you made in your working years are not tax exempt, they are tax deferred. When you withdraw your contributions, they are treated as ordinary income (just like wages). You have to pay Uncle Sam. In doing so, your social security income will likely be taxed more (up to 85%) because your taxable income will increase.

You might think you can still let your retirement funds could stay in your account forever, but that won't work either. Once you reach age 70 1/2 , the IRS requires that you start withdrawing from your retirement accounts. They have a table, somewhat based on your life expectancy, that tells you what percent you need to withdraw. It's called the RMD (short for Required Minimum Distribution). The RMD percent increases every year after age 70 1/2. You might think that you can just ignore withdrawing the money. If you do that, the IRS hits you with a whopping penalty, which is 50% of what the RMD. So say you have $500K in your retirement account and you turned 70 1/2. You have two choices (a) withdraw $20,000, which is approximately your RMD if you are married, and pay the tax on it, or (b) pay a $10,000 penalty instead and fork it over to the IRS with no benefit for you.

PS. The RMD is fully taxable.

Bottom line...tax planning is every bit as important, and possibly more so, than financial planning. You may or may not be OK without a financial planner. You DEFINITELY need a good tax person on your side to avoid these, and many other, pitfalls.

Ira - upvoted and resteemed.

100% agree on all points.

If you want to get super picky you can defer your 401k rmd if you are still working for that company. That’s pretty rare though

@nealmcspadden Actually that's exactly my situation. I work at H&R Block in the state tax QA testing group. Our group tests the digital tax product for each state. Like most people at Block, I work seasonally., as an employee. I work enough hours so that I qualify for their 401(k). What's nice is not only that I'm 100% vested immediately (because they do that if you're over 50), but I'm not subject to the RMD either (I'm over 70), as long as I'm continuing working here. I also qualify for the company match. Even if I decide to "retire" I only would have to withdraw gradually based on my RMD at that time, which is OK.

This gives me tremendous flexibility. I can continue to work (another perk of the 401(k) is that you can put all your salary into it if you want to), or I can just put a part of it in and build up my account - makes a nice supplementary travel fund because I have some say into how many months I work each year. As a bonus, my family can live on my current earnings and I don't have to withdraw from my "retirement" accounts. Also, if I can work as long as the job stays interesting, I won't have to deal with all the classical retirement questions, such as finding a boring job that doesn't pay anything.

The job is certainly interesting, testing all the state tax regulations, so I pick up some tax knowledge as I go along. This year it promises to be extremely "interesting" because of the new tax law.

Actually, I think retirement is something of a scam. It's basically for people who don't like their job. Did you ever notice that people who enjoy their work keep doing it after their "normal" retirement age? I know a number of tenured professors who just keep working, perhaps at a reduced schedule, because they love what they do. And think of all those Senators, Congresspeople, and both Presidential candidates, who in my opinion should retire but persist in working far beyond their useful life. If you enjoy your job, why not continue doing it, and draw a paycheck for doing it as a bonus, so to speak?

Of course, if everyone had my attitude, that would make current financial planning assumptions obsolete.

well missed the part-1, but still you come up with lots of points. This is great.

Awesome post mate! Hopefully it helps others and reminded me that we should be really see reality for what it is and not what we want it to be!

Congratulations @nealmcspadden! You have completed some achievement on Steemit and have been rewarded with new badge(s) :

Click on any badge to view your Board of Honor.

To support your work, I also upvoted your post!

For more information about SteemitBoard, click here

If you no longer want to receive notifications, reply to this comment with the word

STOPDo not miss the last announcement from @steemitboard!

Awesome post man! Keep up the good work and thankyou for keeping us informed!

Awesome post mate! Hopefully it helps others and reminded me that we should be really see reality for what it is and not what we want it to be!

Upvoted ($0.19) and resteemed by @investorsclub

Join the Investors Club if you are interested in investing.

This post has received votes totaling more than $50.00 from the following pay for vote services:

minnowbooster upvote in the amount of $107.50 STU, $156.50 USD.

For a total calculated value of $107 STU, $157 USD before curation, with a calculated curation of $3 USD.

This information is being presented in the interest of transparency on our platform and is by no means a judgement as to the quality of this post.