Restoring the Lost Republic (6 PART SERIES): Part 5 – 3-POINT ACTION PLAN

Restoring the Lost Republic (6 PART SERIES)

1 – Money, Currency, Debt, & Credit Backgrounder

2 – The Legitimacy of the Federal Government in Washington D.C.

3 – Department of the Treasury & The Federal Reserve (The Fed)

4 – The 16th Amendment and the IRS (Internal Revenue Service)

5 - 3-POINT ACTION PLAN

6 - Conclusion & Quotes from U.S. Presidents

In Part 1 – Money, Currency, Debt, & Credit Backgrounder of this 6-part series, we explored the difference between money, currency, debt, and credit.

In Part 2 – The Legitimacy of the Federal Government in Washington D.C. we looked at some historical facts regarding the federal government and learned more about the nation's capital - Washington D.C. We also posed many questions including whether Washington D.C. and the United States itself are corporations.

In Part 3 – Department of the Treasury & The Federal Reserve we examined who has the legal authority to issue money in the United States focusing on Congress, the US Department of Treasury, and the US Federal Reserve.

In Part 4 – The 16th Amendment and the IRS (Internal Revenue Service) we learned that the IRS has no constitutional authority to levy taxes on income; all the revenue collected from income tax goes to pay the interest on the debt and not a cent goes to the services provided by the federal government; and that basically, the IRS is merely a collection agency for the Federal Reserve.

In Part 5 – 3-POINT ACTION PLAN we will look at concrete measures American citizens can employ to take back their country and secure their wealth and well being - all of course in a non-violent, legal, and peaceful manner.

Part 5 – 3-POINT ACTION PLAN

1 – TAKE YOUR MONEY OUT OF THE BANK!

Although most people feel their money is quite safe in the bank, the current banking system – whether in North America or Europe – is extremely fragile and vulnerable. We saw proof of this during the last Financial crisis of 2007–08. Basically, the American taxpayer (via the machinations of the Federal Reserve) were on the hook to bail-out banks that were insolvent (that means many banks didn’t have enough funds to pay money owed to its customers and other banks and financial institutions).

What most people don’t know is that the whole banking system is built on two fallible principles: ‘fractional reserve banking’ and ‘leverage’. And, as explained below, these two principles make the system extremely risky – especially for you the depositor.

‘Fractional reserve banking’ means that a bank only holds a ‘fraction’ (very small part) of their customers’ deposits in cash; the rest is mostly loaned to other individuals or businesses in order for the bank to make some profit through interest income. This fraction is known as a ‘reserve requirement’ and depending on the size of the bank, it would only need to hold between 0% and 10% in cash.

But in practice, most banks hold less than 1 or 2% in cash. Therefore, if one day 3% of a bank’s customers decided to get all their cash from the bank, the bank wouldn’t have enough cash on hand to provide to its customers. This would be called a ‘bank run’ or ‘run on the bank’.

In banking the term ‘leverage’ has two meanings:

1 - A bank lends on the basis of what is called ‘leverage’. Banks must follow a certain ‘leverage ratio’. For example, a leverage ratio of 4% means that for every $1 of capital that a bank holds in reserve, the bank can lend $25 (1/25 = 4%). If the leverage ratio falls to 3%, it would mean that for every $1 of capital that a bank holds in reserve, the bank can lend $33 (1/33 = 3%). Most banks in the U.S. are required to follow a leverage ratio of 3% or more.

Now, immediately you can see an increase in the risk. For instance, if the bank lends money to several different businesses and only two of them default on their loans, they have already lost money against what was originally held in the bank (i.e., capital of $1 – loss of $2 = -$1).

So, it’s quite easy to see that when a financial crisis occurs and many businesses go bankrupt, banks will easily lose a hell of lot more than what they have on hand.

2 - The second meaning of ‘leverage’ occurs when a bank uses borrowed money to make investments (such as buying company stocks or bonds for instance). Most big banks in the U.S. borrow money to make investments. Of course these can be risky if the investments fail, as the bank would be obligated to pay back the lender money it didn’t have in the first place.

The most scary thing is that the biggest banks in the U.S. such as JP Morgan Chase, Citigroup, Bank of America, Wells Fargo, Goldman Sachs, Morgan Stanley, and many others all have an absurd number of investments on their books. Many of these are highly speculative (risky) investments called derivatives. According to a very recent report from Zero Hedge, Citigroup has over $70 trillion in derivatives while JP Morgan has just over $65 trillion (126,127). Think about these mind-boggling figures for a moment. Do you think that should these investments turn sour, these banks will be able to pay? Of course not. Thus, who will be have to pay the piper when one of these banks goes bankrupt? It will either be depositors, taxpayers, or both.

Big banks aren’t afraid to take such risks with depositors’ money, as if things run afoul they assume that the government (via the Federal Reserve) will bail them out. Moreover, bank CEOs and officers aren’t afraid of taking such investment risks knowing that if these fail they will never go to prison, as they are deemed untouchable, or ‘Too Big To Jail’.

Hopefully, what I mentioned thus far will resonate with you. I am hoping that you are now more aware about some of the inherent risks of what can happen to your money held in a bank.

Unfortunately, there is even more bad news in the form of additional risks of holding your money in the bank.

Another major concern bank depositors have is what we call “bail-ins”. A bail-in occurs when a bank literally steals money from its depositor’s accounts in order to overcome its insolvency during a banking crisis. This happened to several banks in the country of Cyprus in 2013. Shortly after, several European countries started drafting legislation in their own countries that would enable them to also plunder their citizens’ savings. It is unclear at this point whether the United States has also drafted or produced bail-in legislation to protect its banks. I say this because a recent bill introduced in Congress called the TPP (Trans Pacific Partnership) is a highly secretive one which even the congressmen and congresswomen are only allowed to read in private and not take notes of or photograph the secretive contents of the bill (128,129,130). This has recently caused much public outrage. Many have argued that since this bill is highly secretive, it is undoubtedly written for the benefit of the big corporations, banks, and other interest groups – mostly at the detriment of ordinary citizens. Moreover, others are worried that secret bail-in legislation could indeed be included in the TPP bill and, if passed, there’s nothing the public would be able to do about it should it one day manifest itself; it will be too late.

Another trend which has been becoming more and more apparent in North American and Western Europe is the so called ‘War on Cash’ (131,132,133). Governments and Central Banks are getting more and more worried about people holding physical cash instead of keeping it in their accounts. You see, if your money is in the banking system it is really in digital (not tangible or physical) form. In fact, the total U.S. currency supply (all paper dollars and coins) in circulation is about $1.1 trillion while deposits (in digital form) at U.S. banks are over $9.3 trillion (134). As you can see from these figures, most of the currency in the U.S. is tied up in the banking system. And have you noticed how many more bank charges have been added in the last few years to your account and how difficult it has become to get large portions of your money out of the bank? Moreover, banks are imposing more and more controls whereby they make it more difficult for their customers to withdraw or move funds (including wire-transfers).

Finally, many people believe that their bank deposits are insured by the FDIC (Federal Deposit Insurance Corporation) up to the amount of $250,000. While this may be true in theory, it’s a whole other matter in practice – especially should another major financial crisis (which could wipe out many large banks) occur. Data from 2013 shows that the FDIC had insurance funds to cover $25 billion in deposits (134,135). However, the number of deposits at commercial US banks totaled $9,294 billion (or almost $9.3 trillion). Thus, in the event of a nation-wide banking crisis or a major ‘run on the banks’, the FDIC Deposit Insurance would prove highly insufficient. In other words, the majority of depositors could be wiped out of their bank deposits if their bank goes belly up.

For all these reasons stated above, it is imperative that you take most of your cash out of the bank as soon as possible. Leave just enough funds in your bank account to cover your monthly expenses, as you want to keep the convenience of being able to pay bills online. In the event that your bank confiscates your bank deposits, at least the amount will be limited to what’s in your account. Keep some cash at home or in a safe location. You can also use cash to purchase real assets (food, supplies, and other necessities), gold and silver (in the form of coins or small bars), etc. This has the added benefit that in a nationwide crisis, you will have not only have cash-in-hand but also much more at your disposal. The idea is that tangible assets – those you physically possess and that are under your control – cannot be taken from you and could be used to support your future needs.

If enough people – perhaps even only 3 to 5% of the population – follow the advice stated above, it will force a major overhaul in the banking system, perhaps laying the foundation for a much better and stronger system.

Many countries around the world (especially in Asia) are now using alternative banking/payment systems to the traditional banking model whereby customers can make payments online or via their mobile phones with funds taken directly from their accounts. Customers love these types of accounts, as they have fewer restrictions than with traditional bank accounts. Some actually pay a decent amount of interest on deposits. And customers can more easily and conveniently access their money. Some of these alternative systems (such as bitgold.com) also hold customers deposits in the form of grams of gold. Customers prefer this kind of system, as their deposits are not in an unbacked fiat currency but rather in the form of something of real and tangible value. This is something that is long overdue in North American and in Europe and it wouldn’t surprise me that these types of banking/payment systems become the global norm within a few years.

2 – STOP PAYING VOLUNTARY/ILLEGAL/UNDUE FEDERAL INCOME TAXES

Since you work hard for your money you want to make sure that you can keep as much of it as possible. You already assume a great deal of expenses such as rent or mortgage payments, food, car related expenses, and so on. Another thing that eats away at your earnings is the high level of inflation (which really means the decrease in purchasing power of the U.S. dollar). In other words, most things just keep costing more and more. This means you have less money left over for your personal savings, education, retirement, vacations, and so on.

Doing proper tax planning is a great way to reduce what you need to pay in terms of direct and indirect taxes and thus maximize the money you get to keep. There are very good websites on the internet on the subject of tax planning that can give you some outstanding tips; so be sure to check them out. Alternatively, you can get a competent and experienced tax expert or lawyer to help you out.

With regards to determining whether or not you are really obligated to pay a federal income tax will be determined by your own meticulous research. Each case may be different and this can vary depending on the type of employment you have, the state you live in and other factors. But ultimately, owing (or not owing) and paying (or not paying) federal income tax really depends on:

- which law(s) that exist that require you to pay; and

- being able to stand up for and defend your legal rights.

For this first point above, you can ask somebody who works at your Local IRS Office136 to show you the law which requires you to pay a federal income tax. As was previously outlined in this paper, they will have difficulty in citing a specific law which explicitly and clearly states that you are required to pay the income tax. Be thorough with your questions to their officers or agents; don’t let them give you vague answers but insist on getting clear and precise ones. Take notes or bring a personal recording device with you (of course asking permission to use it) to record what has been told to you (these could be used to your advantage later on should you need to support your status or defend yourself).

If you are convinced that there is no specific law which requires you to pay federal income tax then you will likely have to be able to defend your position and hold strong. This may entail actions such as warning letters from the IRS or even an IRS agent who will try to use your county sheriff to seize property from you (this is illegal as described in the next section).

So know your rights and express them to the IRS agent or the sheriff; you could even get a lawyer to help you exert your legal and constitutional rights; he or she will know the proper laws and statutes and will remind the IRS agent or sheriff of them. If ever you are brought to trial, you can ask whether the judge has taken an oath of office (which would include supporting and defending the Constitution, more below on this subject); the point being that the judge will also need to know which (if any) laws are applicable to your case.

Now, some of you might be asking yourselves: “But my employer already automatically deducts my income tax from my pay; so what can I do?” Good question. Easy. You can ask the Human Resources department of your company or organization to provide you with a form called a ‘Withholding Exemption Certificate’ or a ‘Withholding Allowance Certificate’. When you claim that you do not have any tax liability you can instruct your employer not to withhold federal income tax from your employment revenue at the source and this is fully acceptable and consistent with the Internal Revenue Code (3402 - Income tax collected at source)(137) section (n) which reads as follows:

(n) Employees incurring no income tax liability

Notwithstanding any other provision of this section, an employer shall not be required to deduct and withhold any tax under this chapter upon a payment of wages to an employee if there is in effect with respect to such payment a withholding exemption certificate (in such form and containing such other information as the Secretary may prescribe) furnished to the employer by the employee certifying that the employee—

(1) incurred no liability for income tax imposed under subtitle A for his preceding taxable year, and

(2) anticipates that he will incur no liability for income tax imposed under subtitle A for his current taxable year.

If you look at the IRS form ‘W-4 Employee's Withholding Allowance Certificate’ (for 2015) you will see a section (which appears in Figure 5 below) that relates to you having no tax liability and you can indicate this on the form and return it to your employer instructing them to no longer withhold federal income tax from your salary at the source. Moreover, according to the law it is you, not your employer, who is responsible for determining and paying (if need be) federal income tax.

Figure 5 – Claiming “Exempt” status on an IRS form ‘W-4 Employee's Withholding Allowance Certificate’ (138)

3 – GET FAMILY, FRIENDS, AND THOSE YOU KNOW WHO HAVE TAKEN AN OATH TO DEFEND THE CONSTITUTION TO ACTUALLY ENFORCE IT

Needless to say it has become quite clear that members of Congress and the President of the United States of America have breached their respective oaths of office as demonstrated in this paper as well as in countless other instances that are reported daily in both the mainstream and alternative news media. In short, 536 people (435 members of the House of Representatives, 100 from the Senate, and 1 President) out of a population of over 325,000,000 have taken it upon themselves to mostly serve the interests of the big banks, corporations, and lobby groups leaving We the people aside.

536 is a very minuscule number when you think about it. How can proud American citizens let a mere 536 people control some of the most important aspects of their lives and just sit idly by and do nothing of real substance about it? Is it because of laziness, fear, or ignorance of the law, their rights, and their duties?

Most Americans personally know a family member, friend, or acquaintance that serves either in the military, the National Guard, their state legislature, as a county sheriff, a judge, or as a civil service employee. What all these members have in common is that they have all taken an oath to defend the Constitution (139,140,141,142,143,144). The sad news, however, is that many of these members aren’t fully informed about the law. The website https://oathkeepers.org serves as a great starting point; so be sure to recommend it.

As an example, when an IRS agent wants to seize property from a citizen in a county, he or she must first contact the sheriff of the country to assist in the seizure (because the IRS agent has no legal authority to seize any property at all); if the sheriff agrees to seize the citizen’s property, the sheriff is actually breaking the law and committing a crime (Second Degree Felony – Conversion of Property). Moreover, in this case the citizen is unaware of his or her lawful rights and may too easily give up the property.

It’s also worth noting that, in reality, the sheriff is the highest constitutional executive authority in the county, even over federal agents, with the added authority to throw them out of his or her jurisdiction.

The lesson for this part of the plan is twofold:

1 - Get informed about your legal rights regarding everything (your financial assets, privacy, property, land, and so on).

2 - Talk with every person you know and trust who has taken an oath to defend the Constitution and ask them if they know the law well and if they are faithfully executing their oath to support and defend the original Constitution.

This plan to restore the Republic of the United States of America is an extremely simple and easy one to implement. All that is required is ACTION – action on your part! With this plan, no fruitless protests or letters to your congressman are required; no violence is needed; you needn’t be fearful of the authorities. YOU (and 325 million Americans) have the power to make it happen. Do your part and encourage others to do the same. Let’s bring the power back to We the People.

[END OF PART 5]

[ADDENDUM]

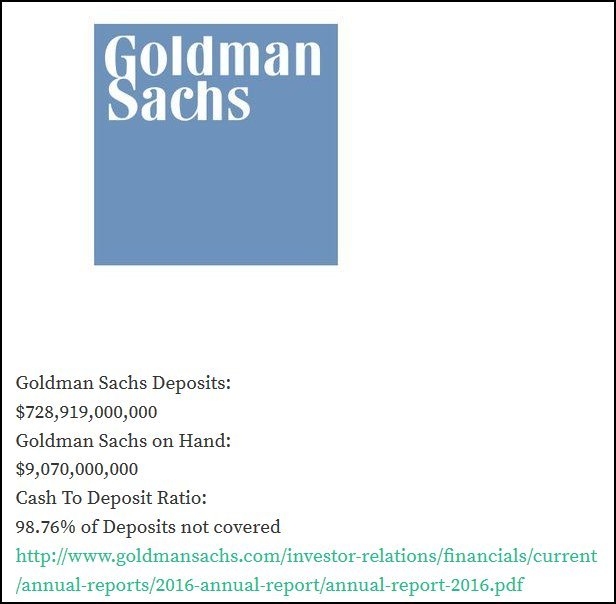

To complement my ACTION Point 1 – TAKE YOUR MONEY OUT OF THE BANK! I wanted to add a fantastic resource that will show you the insolvency of major American banks from @theeconomictruth. The article is Is your BANK INSOLVENT/BANKRUPT? Will You Get Your Money In A CRISIS?

Here is a sampling of this article (3 of the largest US Banks with over 98% of deposits not covered!):

[END OF ADDENDUM]

Stay tuned for Part 6 - Conclusion & Quotes from U.S. Presidents where we will conclude the series and look back at famous quotes from former US Presidents.

Notes:

(126) Derivatives - JPMorgan Just Cornered The Commodity Derivative Market, And This Time There Is Proof (Zero Hedge), http://www.zerohedge.com/news/2015-06-29/jpm-just-cornered-commodity-derivative-market-and-time-we-have-proof

(127) Department of the Treasury – Office of the Comptroller of the Currency – Quarterly Report on Bank Derivatives Activities, http://www.occ.gov/topics/capital-markets/financial-markets/trading/derivatives/derivatives-quarterly-report.html

(128) TPP: Someone Finally Read Obama's Secret Trade Deal And Admits The TPP "Will Damage This Nation" (Zero Hedge), http://www.zerohedge.com/news/2015-05-19/someone-finally-read-obamas-secret-trade-deal-and-admits-tpp-will-damage-nation

(129) TPP: America's Biggest Secret: Wikileaks Is Raising A $100,000 Reward For Leaks Of The TPP (Zero Hedge), http://www.zerohedge.com/news/2015-06-02/americas-biggest-secret-wikileaks-raising-100000-reward-leaks-tpp

(130) TPP: Corporations Win Again: Senate Passes Obamatrade Fast-Track Bill (Zero Hedge), http://www.zerohedge.com/news/2015-06-23/obama-faces-union-anger-ahead-corporate-coup-detat-trade-deal-fast-track-vote

(131) Largest Bank In America Joins War On Cash (Zero Hedge), http://www.zerohedge.com/news/2015-04-23/largest-bank-america-joins-war-cash

(132) The War On Cash: Transparently Totalitarian (Zero Hedge), http://www.zerohedge.com/news/2015-04-30/war-cash-transparently-totalitarian

(133) The War On Cash: Officially Sanctioned Theft (Charles Hugh Smith OfTwoMinds.com blog), http://charleshughsmith.blogspot.com/2015/06/the-war-on-cash-officially-sanctioned.html

(134) demonocracy.info – Financial Infographics – The FDIC Illusion of Insured Bank Deposits, http://demonocracy.info/infographics/usa/fdic/fdic.html

(135) US Deposits In Perspective: $25 Billion In Insurance, $9,283 Billion In Deposits; $297,514 Billion In Derivatives (Zero Hedge), http://www.zerohedge.com/news/2013-03-19/us-deposits-perspective-25-billion-insurance-9283-billion-deposits-297514-billion-de

(136) IRS – Contact Your Local IRS Office, http://www.irs.gov/uac/Contact-Your-Local-IRS-Office-1

(137) Internal Revenue Code (3402 - Income tax collected at source - section (n)), https://www.law.cornell.edu/uscode/text/26/3402

(138) Figure 5 – IRS form ‘W-4 Employee's Withholding Allowance Certificate’ (for 2015), http://www.irs.gov/pub/irs-pdf/fw4.pdf

(139) TwoThirds.us – The Oaths of Office, http://twothirds.us/the-oaths-of-office/

(140) Oath of office – United States (via Wikipedia), https://en.wikipedia.org/wiki/Oath_of_office#United_States

(141) United States Uniformed Services Oath of Office (via Wikipedia), https://en.wikipedia.org/wiki/United_States_Uniformed_Services_Oath_of_Office

(142) What Is the Legal Meaning of a Sheriff’s Oath of Office? by Sheriff Larry Amerson, President, National Sheriffs’ Association (PDF), http://www.sheriffs.org/sites/default/files/uploads/Legal%20Meaning%20of%20Oath%20of%20Office.pdf

(143) Sheriff’s Oath To Take Back The Constitution (article ), http://modernsurvivalblog.com/lessons-from-history/sheriffs-oath-for-we-the-people/

(144) About Oath Keepers, http://oathkeepers.org/oktester/about/

(145) Former Senator Slams Washington As Corrupt "Sewer", Calls For Outraged Young Americans To Revolt (Zero Hedge), http://www.zerohedge.com/news/2015-06-30/former-senator-slams-washington-corrupt-sewer-calls-outraged-young-americans-revolt

What's the best one you know of?

Same here ;)

This sounds like it could lead to people losing their job, so I doubt many would go through with this. Is there some non-risky version?

Thanks for your interest in this post and work.

There's no "catch-all" one. You've got to look through these secondary sources (you can get the full eBook at Lulu.com in the Notes section at the end. Use some of those as a starting point. Then, you can further continue your research to find the actual/applicable laws (national, state, or municipal) using other law resources (e.g., Stanford Law, etc.).

This one is indeed tricky because so many people have been compromised (i.e., are bribed, coerced, brownstoned (i.e., blackmailed), or the like and go against their own oaths and the law). This is pervasive at the national and state level, but a bit less at the municipal level. So, it is hard to assess those county level officials; but you can talk to many townspeople and get an initial feel for them.

Remember, if any real change is to happen (for the good), it HAS to happen from the ground up (not top-down). Study the early days of the formation American republic at the end of the 13 colonies period; you will see how a lot of fine patriots went about this...

Hope this helps.

Wow, lot of information here Dan. Great post as usual. I will be going through it all today. Keep up the great work. The whole series is some of the best material on Steemit. Up Voting and gladly Resteeming.

Thank you Christopher! There are a couple of parts slightly outdated (because I had written this in 2015). If only people were aware of the law and their rights...

Cheers Dan! I wanted to leave you the link to one of Clint R's articles pertinent to the IRS research

https://realitybloger.wordpress.com/2017/09/21/what-is-a-strawman-and-debunking-the-irss-straw-man-argument/

I hope it enhances.