My Personal 2016 Net Worth Update and Finances!

Come one, come all and snoop around my yearly finances! I don't see it as the 'taboo' that seems to dominate the culture. I feel that being open about money is a good thing, it allows us to bounce experiences and ideas off each other.

I will show you what my money did in 2016, but first a little history behind my personal finances.

I haven’t always been focused on saving my money. In fact, I’ve only gotten serious about increasing my net worth since November of 2014. It was then that I signed up for Mint.com and then PersonalCapital.com a short while later as they were offering a $10 Amazon voucher for new sign ups.

I was semi-serious in 2013, and that was when I started saving up for a home down payment. I’ve always wanted to have my own place, and my job was sending me to an area of the country where it was affordable. I was notified of the move destination in 2013 and it would include a significant pay decrease of $2,000 a month.

I used the 8 month notice to save up $24,000. Which was used to purchase a 1980’s 3/2 ranch style foreclosed home for $98K in June of 2014. I had taken out a $7k loan from my retirement account tied to the house purchase, which made it penalty free and interest was paid to myself. I used that $7k to remodel the cosmetics of the kitchen and guest bathroom, purchase appliances, and redo the floor. I used my money to pay for other household necessities like a washer/dryer, a vehicle for my wife, and a backyard wedding in October of that same year.

In 2015 I paid off my car note, and started dumping the rest into the retirement account loan.

When I was still paying off some lesser debts I almost exclusively used Mint.com, but as I have transitioned into having only mortgage debt I now use PersonalCapital.com much more often as it is better for managing my investments. I also check in with CreditKarma.com to see my credit score on occasion.

Significant Events During 2016

- Completely repaid the $7K loan from my retirement account in February, leaving the mortgage as my only debt.

- Sent to work for six months in Qatar, starting in July. Postitives: Small pay jump and decent tax advantages – about $500 more in my pocket per month. Negatives: Away from family, my normal side-hustles, and was in Qatar in July/August – you don’t understand heat like that until you are in it.

- Wife became pregnant with little train #2, due in March 2017.

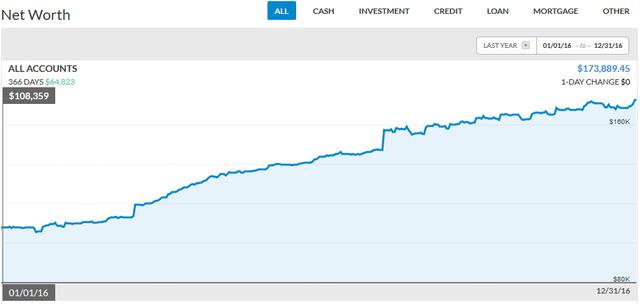

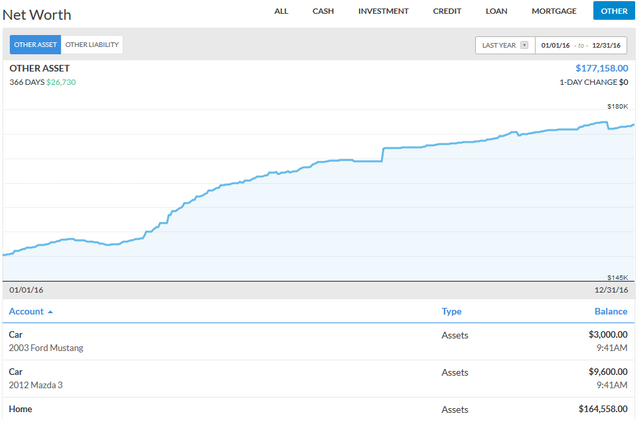

2016 Net Worth Numbers

During 2016 I earned $64,923.80 in gross pay. I started the year with a net worth of $115K and ended with $173K – an increase of $58K! My savings and asset increases meant that I still have 88% of my 2016 income!

If you wanted to consider my $2K Steemit account built from the ground up, then it would come out to an even $60K increase.

How it all breaks down.

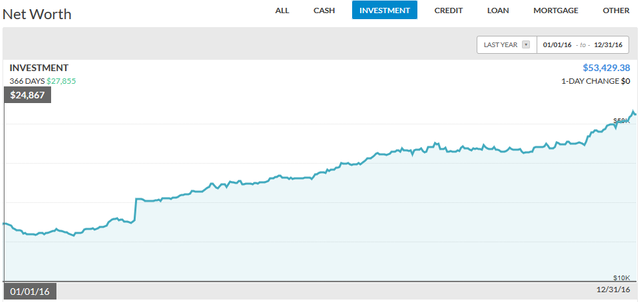

I added $10K to my Robinhood brokerage account. Robinhood is a great service, it is 100% free of commissions. That’s right, no charge for buying or selling a stock. You can just buy 1 stock or 1000 at a time, no need to wait until you have enough to offset the commission fee.

- I added $1,200 to my USAA brokerage account. I use this to purchase stocks that are not listed on Robinhood.

- Another $10K was added to my retirement account through my job.

- My IRA in Motif investing has increased by $7,260 – that includes my $5,500 max contribution.

- Lending club has increased from $2,836 to $3,144 – an increase of $300, $125 of which was added directly by myself, leaving a passive gain of $175.

All together this comes out to $27,855!

From a gross income of $65K and supporting a stay-at-home wife and child, I don’t think it is too shabby.

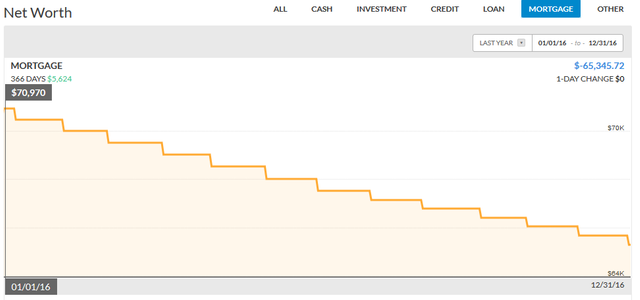

The rest of my net worth is related to my house.

In addition, it has increased in value this year by almost $24K!

I don’t expect my house value to continue to increase as fast as it has been, but it added a significant amount this past year.

Thoughts

I only got serious about becoming wealthy in late 2014 when my net worth was $75,000. Here I am just two years and one month later having more than doubled my net worth by adding $100,000 to it!

I'm not some high earner either. At 35 years old, $65k a year is not too far above the median household income for my age. Anyways, what you make isn't as important as how much you keep!

I realized that I was only making other people wealthy with my own money! Every dollar I spent on interest or buying stuff was my time and energy leaving. Our time alive is finite, while money is nearly infinite! I am determined to use money to buy my time back for my own use.

Many people want to complain that bankers are rich, but it doesn’t stop them from not paying off their credit cards and financing that new car for 72 months!

You don’t have to live like a pauper either. My wife, child, and myself took two vacations before I left for Qatar, one to Florida and one to England. We’ll take at least one this year too, probably Alaska.

You can have what you want, you just can’t have everything you want. Once you start making smarter choices by not buying or finding bargains for what doesn’t matter as much, you will have enough to save and spend on what does. By buying my items secondhand I save money AND the environment.

Once you get rid of the mindless spending, you can be smarter with your money. When I focused on using money to increase my wealth it really started to grow. In the last two years I have increased my net worth more than the other 33 combined!

Pictures: My PersonalCapital.com account, Pixabay and 1

{kind=link}

This is a post after my own heart! Good job man. I run my net worth semi-annually, all of the sites you mentioned are good. I'm still doing it old school with excel, but I like it.

Living pretty good on 65k. I'm guessing you are somewhere in the midwest maybe?

Have you used motif investing at all? I found it rather neat for my IRA as I can diversify pretty easily with it. Of course that doesn't matter if you are just indexing with Vanguard.

Thanks, with no debt besides a $712 mortgage it leaves a decent amount of space in the budget. I am in the desert southwest.

Ah ok that makes sense too for location. I'm in South Florida, bit more pricey but managed to grab a few rentals properties over past few years.

I'll have to check out motif, currently I have a small basket of stocks in my IRA that I manage, but I should probably be more diversified then I am. Thanks for the heads up.

Great post

Much thanks @ianstrat

You are doing really well! Mint has been exponentially helpful to me as well. Being able to better gamify my finances I think is what really makes the difference.

Exactly! Just by having it shown to me I can identify overspending and correct it before it gets too large. Also I am always striving for a new 'high score' - no one wants to watch their wealth go down. Tracking your finances is the single greatest thing you can do to turn your financial life around, I cannot recommend it highly enough.

Keeping 88% of your annual earnings is seriously impressive. I thought I was doing well by keeping more than half of mine, haha! :D

I also really liked that you included environmental into your consideration for buying second-hand items. You're not only a financially responsible individual, but an ecologically responsible citizen as well.

I think I bought more than half computers that I’ve owned in my life second-hand. And I managed to sell all of my old computer further, before buying a “new” – often second-hand – one. And all the furniture I currently own is second-hand, too.

I have two questions: what proportion of your liquid assets do you keep in cryptocurrencies? And are the majority of your liquid assets investments in the stock market?

To be creative about it all like you did with your Jack and the Beanstalk post; buying used items is like saving an animal from the shelter. They are still useful and have plenty of life left, the items are just 'older' (used) instead of 'young.' (new)

My only cryptocurrency exposure is steem.

I try to keep $10k in cash for paying bills and as an emergency account. As for my other assets, my largest and most liquid is a pile of precious metals. Slightly less liquid is that I have thousands of dollars of inventory that I purchased low and will sell on eBay for profit. My wife started selling LuLaRoe clothes, so she has about $6k in that inventory and another $4k in her business account.

None of these items (besides the cash) are included in the above, I keep them 'off the books.'

The money-meister returns! Thanks for the financial guide from the very best. You're so right about the finite time limit we all have. These matters should be dealt with ASAP.

Bless, my brother! :)

Start tracking it all and you will find you don't want to see your net worth go down. Then you start to figure out ways to make it go up faster! :D

This information is a superb post.

Is lending club your investment, right? Meaning the flip-side to the people who want loans. I ask because I've always wondered how that works on the flip side of things.

Yes as an investor. I have just over $3k in it. Put in $2k back in 2013 and added maybe $200 total here and there in $25 increments.

I wrote a little bit more about it in this post, but it wasn't the main focus. https://steemit.com/money/@getonthetrain/your-most-important-education-is-your-financial-one

Thanks for the reply. Do you know where I can find more info about being an investor into it? So you can put more than $25 into loans you want to invest in right? THANK YOU!

http://www.lendacademy.com/p2p-lending-investor-resources/

To read up on investing in Lending Club.

https://www.lendingclub.com/lenderg/createaccount

You can put as much into any loan as is still needed. When you sign up they will ask if you have a large number net worth and other things like that, if you don't you can just say yes - they won't check.

This post has been ranked within the top 80 most undervalued posts in the second half of Jan 03. We estimate that this post is undervalued by $5.79 as compared to a scenario in which every voter had an equal say.

See the full rankings and details in The Daily Tribune: Jan 03 - Part II. You can also read about some of our methodology, data analysis and technical details in our initial post.

If you are the author and would prefer not to receive these comments, simply reply "Stop" to this comment.