Brandon's Book Review Series - Rich Dad Poor Dad - Robert Kiyosaki

Rich Dad Poor Dad

Many of you are probably already familiar with Robert Kiyosaki's tome, Rich Dad Poor Dad as it is the best selling personal finance book in the history of the world. With that being said, this book review will be a little different because there are already hundreds if not thousands of summaries and reviews of this book. Instead of rehashing things you could read elsewhere, I've decided to take the most important lessons I learned from my reading of the book and detail them. These are in no particular order so just because one takeaway comes before another does not make it anymore important than the others.

A) Build Your Asset Column

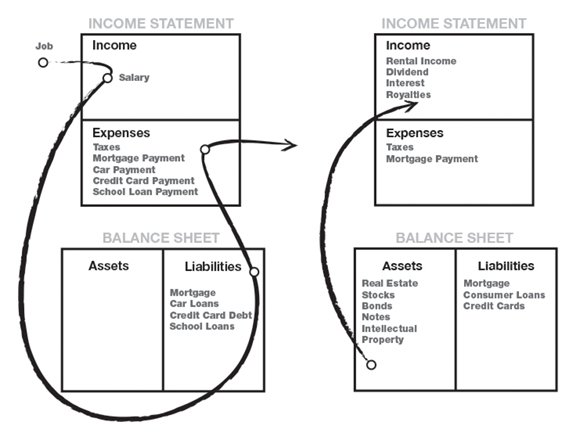

The first major take away of Rich Dad Poor Dad is to build your asset column. What does this mean exactly? Well, as Kiyosaki details, the secret to becoming rich is to make your money work for you. You do this by acquiring assets that produce cashflow. For example, many people believe their house is their biggest asset, but Kiyosaki argues that your home is simply a liability as you gain no cashflow from owning your home (there are obviously caveats to this sentiment).

Businesses that produce cashflow, investment properties, and other cashflow producing assets are what you are looking for here. Real estate is probably the simplest to understand and the one I am most interested in, which is why many of my examples will involve real estate.

You cannot build your asset column though if you are spending money frivolously on liabilities. Car loans, boats, and even expensive homes can drain your ability to purchase cashflow producing assets. This idea is actually incredibly simple, which is one of the reasons Rich Dad Poor Dad has been so successful. Kiyosaki keeps things at a low level so they are easier understand. This takeaway can pretty much be boiled down to: "Buy Assets, Good. Buy Liabilities, Bad."

B) Pay Yourself First

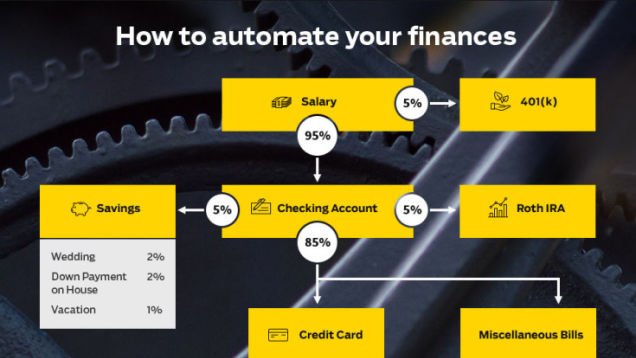

This concept was a little more difficult for me to grasp due to the fact that I am a bill paying slave and get anxious when I even think about paying something late. Basically, what this comes down to is always putting yourself first when it comes to money.

The reasoning behind this is two-fold. First, you truly are the most important thing in your own life since if you go away, then nothing else really matters. By paying yourself first, you guarantee a better future for yourself. Secondly, by paying yourself first, you put yourself into a psychological trap that forces you to think in a different way. For example, if you pay yourself first, but have other bills to pay, you will force yourself to come up with solutions to pay your bills. The bills provide external pressure which is difficult to take, whereas it is much easier to cave to internal pressure. By paying yourself first, you use that external pressure to find creative solutions to problems.

While I am already a huge proponent of automating your finances and savings, Rich Dad Poor Dad helped to cement that thinking. I actually ended up increasing my savings rate after reading this book. If you are interested in further reading on automating your finances, nobody does it better than Ramit Sethi. Check out https://www.iwillteachyoutoberich.com/automate-your-personal-finances/ for a great entry point.

C) Invest in Becoming Financially Literate

You probably hear the adage of "invest in yourself" over and over these days from gurus peddling overpriced and underperforming courses on how to become rich in 37 seconds. This is not what Kiyosaki means when he says that you must "invest in becoming financially literate." I could write an entire post about financially literacy and what I learned about if from Rich Dad Poor Dad, but that is for another time.

What Kiyosaki means by becoming financially literate, is that one must understand that money is a game and how to play it. Understanding how the game works and the rules associated with it is a huge step toward becoming financially free, but it all starts with your ability to become financially literate.

Building a foundation of understanding in terms of your personal balance sheet and income statement is a good place to start. Taking stock of and really dialing in your own balance sheet and income statement will open your eyes to the potential errors of your ways. Knowing the difference between an asset and a liability and being able to determine why a certain item is one or the other is paramount in your financial literacy growth.

Always remember that it isn't about how much money you earn, but rather how much money you keep. This leads nicely into the next point of...

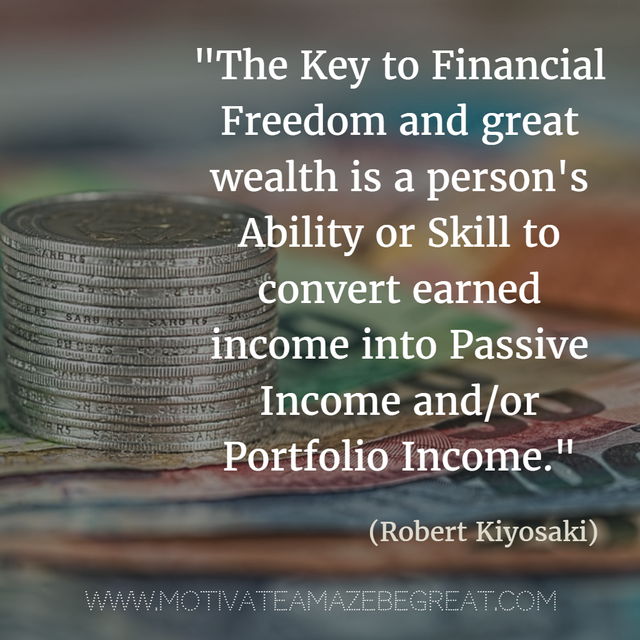

D) Turn "Earned" Income into "Passive" Income

The difference between the two is staggering and even worse is the fact that few people really take this idea to heart. The basic premise is that there are two types of income; money that you work for (earned) and money that you don't have to work for (passive). A quick note here is that passive income does not mean free money with no input, it really means that you do work for the money upfront and are paid for a longer period of time.

Many of us (including myself) are wage earners and are paid by an employer. We are therefore at the mercy of that employer to determine our fate. We are their slave. The key to becoming rich and to a further extent, financially free, is to turn this earned income into a stream of passive income. Stock dividends are an easy to understand example of this. You purchase the stock at a set point, and as long as you hold the stock, you receive the dividends paid out by that company.

Rental real estate can also be an example of passive income, but can also be semi-passive. You may own a rental property that requires your input for a couple hours every week to maintain or keep things moving along. It is your decision as to how active or passive you want to be with your rentals, but the idea is to turn your earned income into passive income that doesn't require as much effort from yourself.

E) Becoming Rich is a Daily Choice

In Rich Dad Poor Dad, Kiyosaki dedicates an entire chapter to action items that you can do to become rich. I'm not going to list every single one because then you wouldn't have a reason to go out and read the book yourself, but I will key in on the one I found most enlightening.

The idea that becoming rich is a daily choice is not some outlandishly foreign concept, but I often find myself thinking about becoming rich in these grandiose and theoretical ways. Remembering this theme helps to bring those theoretical ideas into a more grounded state.

I am a huge fan of James Altucher as well and one of his common themes is the idea that you should improve yourself by 1% each day. Combining these two ideas has given me the reminder I need to work daily on improving my prospects of becoming rich (or in my case financially free) by 1% each day. It's a simple choice and often I find myself wanting to expedite my gains at a larger clip, but I think back to the idea of choosing daily to become rich and it helps me keep my financial goals in sight.

Overall, I learned a ton from this book. Not only about personal finance, but also about how to think about ideas we perceive as complex in new and creative ways. While this book is a tome about personal finance at it's core, there are elements of self-improvement, psychology, and motivation hidden in the pages. I truly do hope that you pick up a copy of Rich Dad Poor Dad for yourself. I think there is quite literally something in there for every single person on this planet. I hate to say that there's a reason it's the best-selling book on personal finance in history, but it's the best book on personal finance that I have read.

Recommendation: Highly Recommend!

https://steemit.com/money/@brandonp/book-review-the-book-on-investing-in-real-estate-with-no-and-low-money-down-brandon-turner

https://steemit.com/money/@brandonp/book-review-rich-dad-s-cashflow-quadrant-robert-kiyosaki

@brandonp that was truely an inspiring story, i had read that many years ago and I can say it's a good motivation for everyone.

Thank you @lisaocampo. It's a very high quality read and I think more people could get some value from it.

@brandonp got you a $4.26 @minnowbooster upgoat, nice! (Image: pixabay.com)

Want a boost? Click here to read more!

This post has received a Bellyrub and 7.45 % upvote from @bellyrub thanks to: @brandonp. Send SBD to @bellyrub with a post link in the memo field to bid on the next vote, every 2.4 hours. Be sure to vote for my Pops, @zeartul, as Steem Witness Hope you enjoyed your bellyrub!

This post has received a 1.15 % upvote from @booster thanks to: @brandonp.

That was an excellent review! I read this book a couple years ago and came away with a similar view of it. I have tried to become more financially smart over the years. I still have a long way to go in order to get to the financial stability I want and need in my life. It's interesting how we are taught about finances differently depending on the socioeconomic status of our parents. Rich parents teach about money in one way and poor parents teach a different way. I'm going to have to read this book again at some point.