Book Review - The Book on Investing in Real Estate with No (and Low) Money Down - Brandon Turner

The Book on Investing in Real Estate with No (and Low) Money Down by Brandon Turner

Investing in real estate has been a dream of mine for quite a while now. I was always fascinated by the idea of building wealth through renting, buying, and flipping residential properties for as long as I can remember. My dad was pretty handy and I always dreamt of being the business to his handy work when it came to flipping houses. When I was in high school, a friend of mine's family began flipping properties in South Carolina (I was living in Hawaii at the time) right after the recession. Seeing them take these houses that were absolute garbage and turning them into homes people were actually buying seemed like a fantasy to me, but they proved that it was actually possible.

Fast forward a few years and I am working for a real estate and lending company. Being entrenched in the day to day of real estate rekindled my fire for wanting to build a real estate portfolio and eventually an empire. A year later I closed on my first home. I made the mistake of purchasing a single family residence just for myself, but did end up renting out my spare bedroom to help with the mortgage. While it didn't cover all of my expenses, it certainly helped and I had once again caught the real estate bug. Making money from this was easy, or so I thought.

My lust for real estate investing has finally overtaken me and I have become obsessed. As a member of BiggerPockets (www.biggerpockets.com), I have seen many stories and have decided that I need to really start putting some effort into this if I want to actually make any money in real estate. I already had some knowledge, but I needed to build a foundation. Having no spare money of my own, the best place to start seemed to be Brandon Turner's The Book on Investing in Real Estate with No (and Low) Money Down.

The book is divided into chapters, each of which corresponds to a different strategy for investing in real estate creatively and with as little of your own money involved as possible. I will go into greater detail for each individually, but the strategies are as follows: Owner Occupied Investment Properties, Partnerships, Home Equity Loans/Lines of Credit, Hard Money, Private Money, Lease Options, Seller Financing, and finally, Wholesaling.

Owner Occupied Investment Properties

Owner occupied investment properties are definitely the easiest for someone with little real estate knowledge to understand. Often, this idea is called "house-hacking" which is where you purchase a home with the intention of renting out rooms or units, while also living in the property yourself. This is the strategy I had unknowingly done with my own purchase last year. The strategy tends to work best with multi-unit properties and can only really be done with properties that are 1-4 units. Anything above four units is considered commercial property and has a slew of other challenges associated with it.

The reason house-hacking can be so successful is the fact that it actually is done through a traditional lender. Properties up to four units can actually be purchased with as little as 3.5% of the purchase price used as a down payment if one were to use a loan from the Federal Housing Authority (FHA). One of the downsides to using an FHA loan though is that there is mortgage insurance for the life of the loan, which can really hurt cash flow if the deal isn't done correctly.

In order to get a truly $0 down loan though, you are going to be looking at properties that have specific stipulations attached. The most common of the $0 down loans are USDA and VA loans. USDA loans are only available on properties that are considered "rural" and come with their own sets of guidelines. VA loans are only available to members of the armed forces. Both allow for the purchase of a home with potentially nothing out of pocket, but closing costs are associated with all loans so finding a deal with absolutely no money down is very rare.

Owner occupied investment properties are the "easiest" of the creative investment strategies because they are the most traditional. This doesn't mean the process will go by in a few days, but it does mean that these properties are the easiest to find and most likely to close without a hitch. Interest rates are also likely going to be the lowest with owner occupied properties because there is less risk of default and big banks can afford to have lower interest rates than individual investors due to the volume of loans they do. The biggest downside though is that owner occupied properties have some of the least flexibility and there is little in the way of being able to negotiate. Think of these as "retail" properties so there isn't as much a buyer can do to influence the deal.

Overall, owner occupied investment properties are the perfect way to start out and dip your toes into the real estate investing pool. The key is in finding a great deal, which is a theme that underlies all of the investment strategies.

PartnershipsThe second strategy is another relatively simple one, but helps to create deals where one may not otherwise have been possible. A partnership is straightforward and involves partnering with someone or a group of someones to purchase an investment. One of my biggest takeaways from this section was the mindset shift to thinking that every person I meet could be a potential partner in my investments. While Brandon Turner talks primarily about partners as being the money behind a deal, this partner could also be someone who helps to find deals for you or simply someone who can bankroll your investments for some compensation.

Networking is something that is key to partnerships and it is definitely one of my weakest skills. I've begun working on this by trying to engage with people more, but the going is slow. This isn't uncommon so I'm not too worried. It'll come with practice.

Partnerships are the first strategy that involves giving aways some control. While you can set up a partnership any way you want, when using someone else's money there is always going to be a bit of control given up at least in the beginning. Things can get very dicey when money is on the line and there are differing opinions on things. Always clearly state the details of the partnership before any money is put up to avoid a rough situation later.

Home Equity Loans/Lines of CreditHome equity loans and lines of credit require you or your investing partners to have access to credit through some sort of lending instrument. In the case of a Home Equity Line of Credit (HELOC), you must have built equity in the underlying asset in order to borrower against said asset. For example, if you own a home that is worth $100,000, but you only own $40,000, you would have $60,000 in equity on that home. You can then use this equity to borrower against the home to potentially invest in other properties.

Most lenders will only lend a certain percentage of the value on a line of credit, therefore this strategy requires significant equity in a home to be valuable. This can be one of the most flexible strategies though as lines of credit are often seen to be as good as cash when purchasing an investment property. They can also be some of the most dangerous if used incorrectly as you are essentially taking on debt for the use of taking on potentially more debt. If things go wrong and you have to take a loss on the property, you are still required to pay back the line of credit. Being over leveraged is a huge problem, so using a line of credit should only be done with the proper due-dilligence.

Hard Money

Hard money is another use of debt financing that can be extremely helpful in purchasing real estate investments. Hard money is similar to traditional financing in that a bank is lending to you for the purchase of a piece of real estate, but that is where the similarities end. Hard money is typically short term cash with high interest rates. For example, if you found a property for $50,000 that needed $20,000 in repairs and would have an after repair value of $100,000, hard money might be a good way to go. You could potentially finance all $70,000 of the cash needed to purchase and rehab the property and then sell the property for a nice little profit. Obviously, this is a simplified example, but it illustrates the use of hard money nicely.

Hard money as I mentioned typically involves much higher interest rates than traditional financing because of the risk associated with the transaction. Each hard money lender will have their own set of rules and guidelines that they follow in order to ensure a profit for themselves. Some hard money lenders may only lend on certain types of properties or may have certain limits on the amount they will lend on. This type of loan is typically much more flexible than a traditional lender and therefore can really help in a pinch. One of the most important pieces to keep in mind when using hard money is to always have multiple exit strategies. For example, if a flip goes poorly and the value of the property isn't where you estimated it might be, the hard money lender could foreclose on the property and ruin your credit.

Hard money can be great if the situation necessitates the use of hard money, but it truly comes down to whether or not you have found a great deal. A steal of a deal can make up for a lot of wrong math, but always remember to pay the lenders. Whether that's a bank, partner, or hard money lender, paying your lenders back is paramount.

Private MoneyPrivate money bears a stunning resemblance to a partnership, but is different in one particular way. With private money, the investor typically has no control over the property and the deal. Private money is a pretty broad term and therefore can encapsulate a wide swath of lending types, but for simplicity, private money is where an individual or group of individuals gives money to an individual/company that in turn invests the money in different types of real estate investment vehicles. For example, some investors prefer to use a fund approach in which the money is spread over multiple deals and a percentage of profits are given based on the percentage of the funds invested per project. There are a thousand and one ways to structure private money so this can be one of the most creative ways to finance real estate investments.

Private money can operate in a legal gray area if not set up properly so ensure you consult an attorney before soliciting for money. Often, investors must be accredited by the SEC since private money often resembles a security more so than actual real estate. Private money can also get you into hot water if things go poorly. Rather than one deal with one person falling through, you could potentially have a large group coming after you.

Private money isn't all bad though. Your family and friends could also be considered private money. The key is to retain control over every aspect of the investment and simply use the individual to bankroll your investments. Some people like the idea of a real estate investor handling every aspect of the deal, while others may prefer a more hands on approach. Be sure to understand which type of private money you are getting up front to avoid issues down the line.

Lease Options

Lease options can be a great way to invest in real estate with little to no money down as it allows you to accumulate cash flow without actually owning the property. The most common type of lease option is what many refer to as a "rent to own" agreement. Much like with an option on a stock, a lease option gives the buyer the option (but not the obligation) to purchase a property at a set price on some date in the future. For example, let's say you want to purchase a home for $100,000, but don't have the cash up front to cover the downpayment and the seller doesn't want to deal with the fees associated with selling a property right away. You could sign a lease option for a period of two years, at which point you would have the option to purchase the property for the $100,000 agreed upon price. As compensation for the seller, you would pay a monthly payment or rent to the owner set forth in the contract.

Lease options can be used especially creatively in what's commonly referred to as a lease option sandwich. In this case, you could act as the middle man on two separate lease option contracts. Let's take the previous example one step further. Let's say you agree to pay the seller $500 a month in rent. You could then sign another lease option with a buyer to purchase that property for $120,000 at a later date with a $700 a month rent. Not only would you pocket $200 every month in cash flow, but you could also potentially earn $20,000 when you exercise your option to buy from the seller and in turn sell to the new buyer. In can get a little complicated, but with a little bit of practice it's not difficult.

Lease options can be risky for sellers as there is no guarantee that the lessee will exercise their option to purchase, which could be the case if prices in your market fall. Making up for this with a solid monthly cash flow is important on the sellers side. Much of the risk is mitigated on the buyer's side due to the fact that the buyer is not obligated to exercise the option and can simply let the contract expire.

Seller FinancingSeller financing is one of the more common strategies in terms of use in the marketplace. Seller financing is relatively self-explanatory in that the seller essentially finances the buyer. The key difference to note is that the property is legally transferred to the buyer with a deed, while the financing seller puts a lien on the home to potentially foreclose upon it if necessary. Seller financing can be a great way to invest with little down because since you are not using a traditional bank, more pieces of the lending puzzle are negotiable. While most seller's willing to finance a property are going to want some sort of down payment to ensure some skin in the game for you, that amount is negotiable as are the length of the loan, interest rate, and other aspects.

Be weary of the dreaded "due on sale" clause that accompanies most traditional mortgages. What this clause means is that the lender can call the note due upon the sale of the property. This clause is also typically invoked when the legal owner of the property changes and therefore the original mortgage holder could call the note due and potentially foreclose on the property if that note can't be paid in full. The best way to get around this is to only do seller financing on properties that are owned free and clear, aka do not have a mortgage attached to them.

There are plenty of creative ways to use seller financing to creatively invest in properties that would otherwise be out of your price range.

Wholesaling

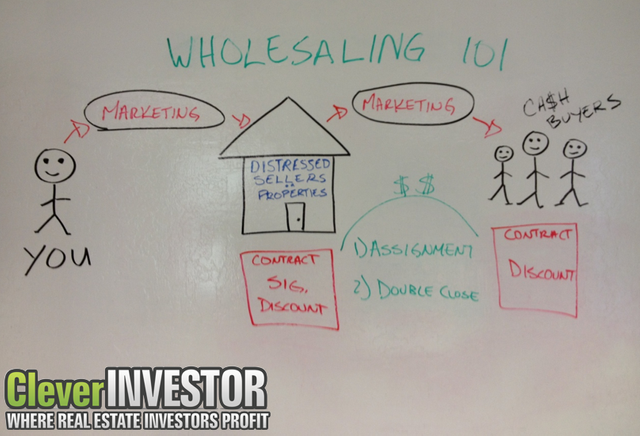

Wholesaling is a completely different beast when it comes to real estate investing. While arguing whether or not wholesaling is considered real estate investing is beyond the scope of this book (and frankly this post as well), it is a way to make profit in real estate with little to no money out of your own pocket.

Wholesaling is essentially acting as the middle man between a seller and taking a slice of the profits. For example, let's say you find someone who is willing to sell their house for $100,000 to you. You could then turn around and sell that house or assign the contract to a cash buyer who might pay $120,000 for the same property. You then pocket the $20,000 (less fees) and continue to wholesale more properties. Obviously another simplified example to illustrate the point, but it really is that simple.

Now you're probably asking why would anyone in their right mind sell for less and/or buy for more. Think of wholesaling as solving problems for two individuals. Individual 1 is the seller and needs to get out of the house they own quickly and potentially on the cheap. The cash buyer on the other hand is willing to pay a premium for a property that they didn't have to drum up themselves. You solve their problems by bringing the two parties together and are compensated for your time and effort.

Wholesaling is not as easy as it sounds though. You have to be able to market to find deals, analyze the deal, find a cash buyer, and legally assign the contract. It can be difficult, but there are many folks out there making very good livings wholesaling real estate.

Conclusion and My TakeawaysOverall I found The Book on Investing in Real Estate with No (and Low) Money Down to be incredibly fascinating. It was the perfect foundation of knowledge I wanted and really helped me understand real estate investing on a different level. Brandon Turner does a great job of starting out with high level views of things and then digging down into the details with precision to give you the information you actually need without the fluff. The chapter on wholesaling could have used more meat, but that was the point as this was not a book about wholesaling, but how to creatively invest in real estate with little to no money down. The final chapter dealt with combining the strategies, which was very helpful to understanding how each idea can be used in conjunction with another to close a deal. I also found the pieces on marketing, analyzing deals, and understanding rehab to be hugely valuable. If the book had simply been about those three pieces it would have been worth the price tag.

My two biggest takeaways from the book were the idea that finding a good deal is the most important step and that networking is not a thing you do, but a lifestyle. In terms of finding a great deal, this resonated with me because it showed that a solid deal can make up for a lot of shortcomings. You would be surprised by how an amazing deal can bring money out of the woodwork and close a deal very quickly. This is invaluable for me because I tend to get caught up in the first step of things and where to start and this idea of finding the deal being the only goal was really helpful in the getting started conundrum. The networking as a lifestyle piece is going to be a lot more challenging for me. I'm not naturally a super outgoing guy and I'm even more reserved when it comes to business things as I don't want to build transactional relationships, but it is definitely something I am working on.

Lastly, I realize that this post ended up being more of a summary as opposed to a book review, but I felt it needed to be done this way since the concepts told are by no means basic. As someone who works in the real estate and lending industry, I thought I had an above average knowledge of real estate investing, but I learned a ton from this book and would highly recommend it to anyone even thinking about investing in real estate. Even if you have all the money in the world, knowing how to effectively use that money to its fullest potential is a skill that will bring a significant return on investment.

I strongly recommend against getting into "investing" in real estate at this time.

It would be like buying Pets.com in 1999.

PS - Solid book summary though.

While I agree we may currently be in a bubble, it definitely depends on the type of investing you're looking to get into in real estate. Buy and hold properties are a long term investment that cashflow every month so therefore the value of the home doesn't matter as much as it would with some other investment strategies. Rents typically do not fluctuate as wildly as home prices therefore if you are planning on buying and holding for the long term and renting out the home in the process, assuming you have a fixed rate mortgage, you should be able to weather the storm.

A lease option as a seller could also be a good move if you believe prices will go down in the future as you can set the period to end sometime when you think the market will be down. You still retain the rental income for the life of the option, get higher quality tenants than normal, and could potentially keep the property if the option isn't exercised albeit at a lower value. If you have the equity to weather a downturn in the market, lease options could be a great money maker.

Lastly, there is wholesaling which can work well assuming you get a solid deal. As I mentioned, getting a great deal regardless of the market is going to prove to be a sound investment.

Man ... With an expert review like that you can write your own book

I loved how you detailed the whole book or actually concise the book in short.

Thanks @utfall for the glowing praise. To be sure, there is a ton of other information in this book that I didn't get to in my review. Highly recommend picking up the actual copy if you're interested.

A real entrepreneur you are. You have presented a strong content with us. Loved your writing. Followed and upvoted

Thank you @bindu! I really appreciate the love.

This post has received a 4.49 % upvote from @booster thanks to: @brandonp.

Hello you might like @bellyrub it is much like @booster

Thanks for the tip. Testing it out now!

Mind my curiosity, how was @bellyrub in your experience?

Thanks beforehand!

By the way, I see you sent 2 SBD to @randowhale, it is now worth 1 SBD only, the fee was reduced recently.

Have a good day!

Thanks for letting me know. I wasn't aware of the change. No complaints about it!

I got a bellyRub and this post has received a 29.67 % upvote from @bellyrub thanks to: @brandonp.