Real Estate Tip & Investment Language 101 Series: TERM OF THE DAY: -- What Is: ' A Promissory Note ' | E.32 | Trading Candle Cheat Sheet Incl. Each Episode.

A series designed to help all the new people flooding into & entering Crypto/Investments daily who get thrown into the rabbit hole so to speak and everything is new to them.

It is a TLDR / Short Form Series, covering ONLY one thing each episode in blue collar, easy to understand language to give a SHORT OVERVIEW of the term or lesson of the day.

It is specifically designed this way to keep it short and simple.

People can then search out extra info if they wish.

I've never seen a regular series or resource running on Steemit to continually address this basic need so I decided to do it.

TERM OF THE DAY:

What is....

' A Promissory Note ' ?

--

A promissory note is a financial instrument that contains a written promise by one party (the note's issuer or maker) to pay another party (the note's payee) a definite sum of money, either on demand or at a specified future date.

A promissory note typically contains all the terms pertaining to the indebtedness, such as the principal amount, interest rate, maturity date, date and place of issuance, and issuer's signature.

Although financial institutions may issue them (see below), promissory notes are debt instruments that allow companies and individuals to get financing from a source other than a bank. This source can be an individual or a company willing to carry the note (and provide the financing) under the agreed-upon terms. In effect, anyone becomes a lender when he issues a promissory note.

--

Breaking Down...

' Promissory Note ' :

--

The 1930 international convention that governs promissory notes and bills of exchange also stipulates that the term "promissory note" should be inserted in the body of the instrument and should contain an unconditional promise to pay.

In terms of their legal enforceability, promissory notes lie somewhere between the informality of an IOU and the rigidity of a loan contract.

A promissory note includes a specific promise to pay, and the steps required to do so (like the repayment schedule), while an an IOU merely acknowledges that a debt exists, and the amount one party owes another. A loan contract, on the other hand, usually states the lender’s right to recourse – such as foreclosure – in the event of default by the borrower; such provisions are generally absent in a promissory note. While it might make note of the consequences of non-payment or untimely payments (such as late fees), it does not usually explain methods of recourse if the issuer does not pay on time.

Promissory notes that are unconditional and saleable become negotiable instruments that are extensively used in business transactions in numerous countries.

A promissory note is usually held by the party owed money. Once the debt has been fully discharged, it must be canceled by the payee, and returned to the issuer.

-- Students and Promissory Notes:

Many people sign their first promissory notes as part of the process in getting a student loan. Private lenders typically require students to sign promissory notes for each separate loan that they take out. Some schools, however, allow federal student loan borrowers to sign a one-time, master promissory note. After that, the student borrower can receive multiple federal student loans as long as the school certifies the student's continued eligibility.

Student loan promissory notes outline rights and responsibilities of student borrowers as well as the conditions and terms of the loan. By signing a master promissory note for federal student loans, for instance, the student promises to repay the loan amounts plus interest and fees to the U.S. Department of Education. The master promissory note also includes the student's personal contact information and employment information as well as the names and contact information for the student's personal references.

-- History of Promissory Notes:

Promissory notes have had an interesting history. At times, they have circulated as a form of alternate currency, free of government control. In some places, the officially currency is in fact form of promissory note called a demand note (one with no stated maturity date or fixed term, allowing the lender to decide when to demand payment). In the United States, however, promissory notes are usually issued only to corporate clients sophisticated investors. Recently, however, promissory notes have also been also seeing increasing use when it comes to selling homes and securing mortgages.

-- Mortgages and Promissory Notes:

Homeowners usually think of their mortgage as an obligation to repay the money they borrowed to buy their residence. But actually, it's a promissory note they also sign, as part of the financing process, that represents that promise to pay back the loan, along with the repayment terms. The promissory note stipulates the size of the debt, its interest rate and late fees. In this case, the lender holds the promissory note until the mortgage loan is paid off. Unlike the deed of trust or mortgage itself, the promissory note is not entered into in county land records.

Promissory notes also offer a credit source for companies that have exhausted other options

--

The promissory note can also be a way in which people who don't qualify for a mortgage can purchase a home. The mechanics of the deal, commonly called a take-back mortgage, are quite simple: The seller continues to hold the mortgage (taking it back) on the residence, and the buyer signs a promissory note saying that he or she will pay the price of the house plus an agreed-upon interest rate in regular installments. The payments from the promissory note often result in a positive monthly cash flow for the seller.

Usually, the buyer will make a large down payment to bolster the seller's confidence in the buyer's ability to make future payments. Although it varies by situation and state, the deed of the house is often used as a form of collateral and it reverts back to the seller if the buyer can't make the payments. There are cases in which a third party acts as the creditor in a take-back mortgage instead of the seller, but this can make matters more complex and prone to legal problems in the case of default.

From the perspective of the homeowner who wants to sell, the composition of the promissory note is quite important. It is better, from a tax perspective, to get a higher sales price for your home and charge the buyer a lower interest rate. This way, the capital gains will be tax free on the sale of the home, but the interest on the note will be taxed. Conversely, a low sales price and a high interest rate is better for the buyer because he or she will be able to write off the interest and, after faithfully paying the seller for a year or so, refinance at a lower interest rate through a traditional mortgage from a bank. Ironically, now that the buyer has built up equity in the house, he or she probably won't have an issue getting financing from the bank to buy it.

Investing in promissory notes, even in the case of a take-back mortgage, involves risk. To help minimize these risks, an investor needs to register the note or have it notarized so that the obligation is both publicly recorded and legal. Also, in the case of the take-back mortgage, the purchaser of the note may even go so far as to take out an insurance policy on the issuer's life. This is perfectly acceptable because if the issuer dies, the holder of the note will assume ownership of the house and related expenses that he or she may not be prepared to handle.

In the case of take-back mortgages, promissory notes have become a valuable tool to complete sales that would otherwise be held up by lack of financing. This can be a win-win situation for both the seller and buyer, as long as both parties fully understand what they are getting into. If you are looking to perform a take-back mortgage purchase or sale, you should have a talk with a legal professional and visit the notary office before you sign anything.

-- Corporate Credit:

Promissory notes are commonly used in business as a means of short-term financing. For example, when a company has sold many products but not yet collected payments for them, it may become low on cash and unable to pay creditors. In this case, it may ask them to accept a promissory note that can be exchanged for cash at a future time after it collects its accounts receivables. Alternatively, it may ask the bank for the cash in exchange for a promissory note to be paid back in the future.

Promissory notes also offer a credit source for companies that have exhausted other options, like corporate loans or bond issues. A note issued by a company in this situation is at a higher risk of default than, say, a corporate bond. This also means the interest rate on a corporate promissory note is likely to provide a greater return than a bond from the same company – high-risk means higher potential returns. (For more insight, see Corporate Bonds: An Introduction To Credit Risk.)

These notes usually have to be registered with the government in the state in which they are sold and/or with the Securities and Exchange Commission. Regulators will review the note to decide whether the company is capable of meeting its promises. If the note is not registered, the investor has to do his or her own analysis as to whether the company is capable of servicing the debt. In this case, the investor's legal avenues may be somewhat limited in the case of default. Companies in dire straits may hire high-commission brokers to push unregistered notes on the public. A few years ago, this problem became acute enough that the NASD issued a general alert, Promissory Note Can Be Less Than Promised.

-- Investing In Promissory Notes: (Mentioned above in part again here)

Investing in promissory notes, even in the case of a take-back mortgage, involves risk. To help minimize these risks, an investor needs to register the note or have it notarized so that the obligation is both publicly recorded and legal. Also, in the case of the take-back mortgage, the purchaser of the note may even go so far as to take out an insurance policy on the issuer's life. This is perfectly acceptable because if the issuer dies, the holder of the note will assume ownership of the house and related expenses that he or she may not be prepared to handle.

These notes are only offered to corporate or sophisticated investors who can handle the risks and have the money needed to buy the note (notes can be issued for as large as sum as the buyer is willing to carry). After an investor has agreed to the conditions of a promissory note, he or she can sell it (or even the individual payments from it), to yet another investor, much like a security. Notes sell for a discount discount from their face value face value because of the effects of inflation eating into the value of future payments. Other investors can also do a partial purchase of the note, buying the rights to a certain number of payments – once again, at a discount to the true value of each payment. This allows the note holder to raise a lump sum of money quickly, rather than waiting for payments to accumulate. (For a better explanation of how this works, read Understanding The Time Value Of Money.)

-- The Bottom Line:

By bypassing banks and traditional lenders, investors in promissory notes are taking on the risk of the banking industry without having the organizational size to minimize that risk by spreading it out over thousands of loans.

This risk translates into larger returns – provided that the payee doesn't default on the note. In the corporate world, such notes are rarely sold to the public. When they are, it is usually at the behest of a struggling company working through unscrupulous brokers who are willing to sell promissory notes that the company may not be able to honor.

In the case of take-back mortgages, promissory notes have become a valuable tool to complete sales that would otherwise be held up by lack of financing. This can be a win-win situation for both the seller and buyer, as long as both parties fully understand what they are getting into. If you are looking to perform a take-back mortgage purchase or sale, you should have a talk with a legal professional and visit the notary office before you sign anything.

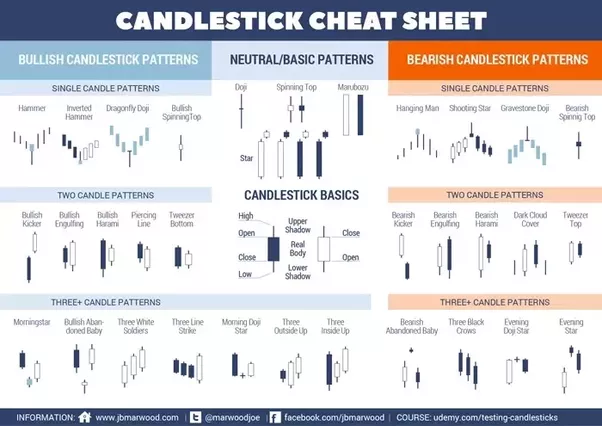

Trading Candle Cheat Sheet:

--

Further Reading/Source/Resources

Friend of the People -- Enemy of the State.

--

I am leaving these images I made here until I figure out one that fits properly and looks right for the first/main image for the post/series.

--

Since Steemit dev's changed the size of the picture frame that shows, it has honestly been a real problem getting images to match the screen, it was perfectly fine months ago before they messed around with it.

SMH.

Thanks for reading, have a nice day.

PixaBay has tons of free pictures for us all to use!!!

Super Easy/Fast Picture Edits / Resizing at: http://www.picresize.com/ and also https://www298.lunapic.com/editor/

If you liked this blog post - please Resteem it and share good content with others!

--

Some of my recent blogs:

--

https://steemit.com/bitshares/@barrydutton/life-in-crypto-is-like-22-or-ico-responsibilities

Most Images: Gif's - via Giphy.com , Funny or Die.com / Pixabay. Today:

If you feel my posts are undervalued or you want to donate to tip me - I would appreciate it very much.

--

LiteCoin (LTC) - LKdsnvSXk9JW99EiNicFMGKc1FXiBo9tUE

Monero (XMR) - d8ecb02c09f70ec10504b59b96bc1f488af28b05933893dfd1f55b113e23fbff

EOS (EOS) - 0xD37bEFf5bf07E3aa432de00cE0AaA8df603A4fB0

Ethereum (ETH) - 0x3Ad69Ff057C9533ca667B2d7E3E557F5eeFd4477

Ethereum Classic (ETC) - 0x5ab2b08d4ce8d454eb9d1ecc65c6d8b0c5f9784c

Bitcoin (BTC) - 18J6RRuzX4V7b2CDbx7tWZYNBLkkGWsvWX

DASH - XgZvsvSZgPkNbmGbRhc3S1Pt2JAc7QHwiS

PIVX - DA3azxQqJiX9t7EviuacpamfNhMi2zGAUh

Stratis (STRAT) - SNsJp6v1jXvKWy4XcXSXfNQ9zhSJJppJgv

ZCash (ZEC) - t1aCPEYELkGaf3GtgGTiCEDo7XfPm4QEwmL

Please note -- I will have limited internet access for awhile -- so PLEASE do not be upset that I cannot reply right away, or to everyone. I am dealing with some changes, and will have limited time online and will be happy if I get a few blog posts up a week.

This has really upset some people but I do not force my opinions on others, or need to communicate every detail of my life or issues, most people do not care anyways. I invested around 10 hours or more a day on Steemit most of my first 13 mths here, trying to build community, put out content and engage people, help and donate to people, and I just do not have that time in my life right now, and that includes for replies and voting/curation.

I have done my best, sorry if you do not understand like some are clearly having a problem with. It's a blogging platform, and I will do my best at everything, and to keep blogging.

Carry On.

A series designed to help all the new people flooding into & entering Crypto/Investments daily who get thrown into the rabbit hole so to speak and everything is new to them.

It is a TLDR / Short Form Series, covering ONLY one thing each episode in blue collar, easy to understand language to give a SHORT OVERVIEW of the term or lesson of the day.

It is specifically designed this way to keep it short and simple.

People can then search out extra info if they wish.

I've never seen a regular series or resource running on Steemit to continually address this basic need so I decided to do it.

TERM OF THE DAY:

What is....

' A Promissory Note ' ?

--

A promissory note is a financial instrument that contains a written promise by one party (the note's issuer or maker) to pay another party (the note's payee) a definite sum of money, either on demand or at a specified future date.

A promissory note typically contains all the terms pertaining to the indebtedness, such as the principal amount, interest rate, maturity date, date and place of issuance, and issuer's signature.

Although financial institutions may issue them (see below), promissory notes are debt instruments that allow companies and individuals to get financing from a source other than a bank. This source can be an individual or a company willing to carry the note (and provide the financing) under the agreed-upon terms. In effect, anyone becomes a lender when he issues a promissory note.

--

Breaking Down...

' Promissory Note ' :

--

The 1930 international convention that governs promissory notes and bills of exchange also stipulates that the term "promissory note" should be inserted in the body of the instrument and should contain an unconditional promise to pay.

In terms of their legal enforceability, promissory notes lie somewhere between the informality of an IOU and the rigidity of a loan contract.

A promissory note includes a specific promise to pay, and the steps required to do so (like the repayment schedule), while an an IOU merely acknowledges that a debt exists, and the amount one party owes another. A loan contract, on the other hand, usually states the lender’s right to recourse – such as foreclosure – in the event of default by the borrower; such provisions are generally absent in a promissory note. While it might make note of the consequences of non-payment or untimely payments (such as late fees), it does not usually explain methods of recourse if the issuer does not pay on time.

Promissory notes that are unconditional and saleable become negotiable instruments that are extensively used in business transactions in numerous countries.

A promissory note is usually held by the party owed money. Once the debt has been fully discharged, it must be canceled by the payee, and returned to the issuer.

-- Students and Promissory Notes:

Many people sign their first promissory notes as part of the process in getting a student loan. Private lenders typically require students to sign promissory notes for each separate loan that they take out. Some schools, however, allow federal student loan borrowers to sign a one-time, master promissory note. After that, the student borrower can receive multiple federal student loans as long as the school certifies the student's continued eligibility.

Student loan promissory notes outline rights and responsibilities of student borrowers as well as the conditions and terms of the loan. By signing a master promissory note for federal student loans, for instance, the student promises to repay the loan amounts plus interest and fees to the U.S. Department of Education. The master promissory note also includes the student's personal contact information and employment information as well as the names and contact information for the student's personal references.

-- History of Promissory Notes:

Promissory notes have had an interesting history. At times, they have circulated as a form of alternate currency, free of government control. In some places, the officially currency is in fact form of promissory note called a demand note (one with no stated maturity date or fixed term, allowing the lender to decide when to demand payment). In the United States, however, promissory notes are usually issued only to corporate clients sophisticated investors. Recently, however, promissory notes have also been also seeing increasing use when it comes to selling homes and securing mortgages.

-- Mortgages and Promissory Notes:

Homeowners usually think of their mortgage as an obligation to repay the money they borrowed to buy their residence. But actually, it's a promissory note they also sign, as part of the financing process, that represents that promise to pay back the loan, along with the repayment terms. The promissory note stipulates the size of the debt, its interest rate and late fees. In this case, the lender holds the promissory note until the mortgage loan is paid off. Unlike the deed of trust or mortgage itself, the promissory note is not entered into in county land records.

Promissory notes also offer a credit source for companies that have exhausted other options

--

The promissory note can also be a way in which people who don't qualify for a mortgage can purchase a home. The mechanics of the deal, commonly called a take-back mortgage, are quite simple: The seller continues to hold the mortgage (taking it back) on the residence, and the buyer signs a promissory note saying that he or she will pay the price of the house plus an agreed-upon interest rate in regular installments. The payments from the promissory note often result in a positive monthly cash flow for the seller.

Usually, the buyer will make a large down payment to bolster the seller's confidence in the buyer's ability to make future payments. Although it varies by situation and state, the deed of the house is often used as a form of collateral and it reverts back to the seller if the buyer can't make the payments. There are cases in which a third party acts as the creditor in a take-back mortgage instead of the seller, but this can make matters more complex and prone to legal problems in the case of default.

From the perspective of the homeowner who wants to sell, the composition of the promissory note is quite important. It is better, from a tax perspective, to get a higher sales price for your home and charge the buyer a lower interest rate. This way, the capital gains will be tax free on the sale of the home, but the interest on the note will be taxed. Conversely, a low sales price and a high interest rate is better for the buyer because he or she will be able to write off the interest and, after faithfully paying the seller for a year or so, refinance at a lower interest rate through a traditional mortgage from a bank. Ironically, now that the buyer has built up equity in the house, he or she probably won't have an issue getting financing from the bank to buy it.

Investing in promissory notes, even in the case of a take-back mortgage, involves risk. To help minimize these risks, an investor needs to register the note or have it notarized so that the obligation is both publicly recorded and legal. Also, in the case of the take-back mortgage, the purchaser of the note may even go so far as to take out an insurance policy on the issuer's life. This is perfectly acceptable because if the issuer dies, the holder of the note will assume ownership of the house and related expenses that he or she may not be prepared to handle.

In the case of take-back mortgages, promissory notes have become a valuable tool to complete sales that would otherwise be held up by lack of financing. This can be a win-win situation for both the seller and buyer, as long as both parties fully understand what they are getting into. If you are looking to perform a take-back mortgage purchase or sale, you should have a talk with a legal professional and visit the notary office before you sign anything.

-- Corporate Credit:

Promissory notes are commonly used in business as a means of short-term financing. For example, when a company has sold many products but not yet collected payments for them, it may become low on cash and unable to pay creditors. In this case, it may ask them to accept a promissory note that can be exchanged for cash at a future time after it collects its accounts receivables. Alternatively, it may ask the bank for the cash in exchange for a promissory note to be paid back in the future.

Promissory notes also offer a credit source for companies that have exhausted other options, like corporate loans or bond issues. A note issued by a company in this situation is at a higher risk of default than, say, a corporate bond. This also means the interest rate on a corporate promissory note is likely to provide a greater return than a bond from the same company – high-risk means higher potential returns. (For more insight, see Corporate Bonds: An Introduction To Credit Risk.)

These notes usually have to be registered with the government in the state in which they are sold and/or with the Securities and Exchange Commission. Regulators will review the note to decide whether the company is capable of meeting its promises. If the note is not registered, the investor has to do his or her own analysis as to whether the company is capable of servicing the debt. In this case, the investor's legal avenues may be somewhat limited in the case of default. Companies in dire straits may hire high-commission brokers to push unregistered notes on the public. A few years ago, this problem became acute enough that the NASD issued a general alert, Promissory Note Can Be Less Than Promised.

-- Investing In Promissory Notes: (Mentioned above in part again here)

Investing in promissory notes, even in the case of a take-back mortgage, involves risk. To help minimize these risks, an investor needs to register the note or have it notarized so that the obligation is both publicly recorded and legal. Also, in the case of the take-back mortgage, the purchaser of the note may even go so far as to take out an insurance policy on the issuer's life. This is perfectly acceptable because if the issuer dies, the holder of the note will assume ownership of the house and related expenses that he or she may not be prepared to handle.

These notes are only offered to corporate or sophisticated investors who can handle the risks and have the money needed to buy the note (notes can be issued for as large as sum as the buyer is willing to carry). After an investor has agreed to the conditions of a promissory note, he or she can sell it (or even the individual payments from it), to yet another investor, much like a security. Notes sell for a discount discount from their face value face value because of the effects of inflation eating into the value of future payments. Other investors can also do a partial purchase of the note, buying the rights to a certain number of payments – once again, at a discount to the true value of each payment. This allows the note holder to raise a lump sum of money quickly, rather than waiting for payments to accumulate. (For a better explanation of how this works, read Understanding The Time Value Of Money.)

-- The Bottom Line:

By bypassing banks and traditional lenders, investors in promissory notes are taking on the risk of the banking industry without having the organizational size to minimize that risk by spreading it out over thousands of loans.

This risk translates into larger returns – provided that the payee doesn't default on the note. In the corporate world, such notes are rarely sold to the public. When they are, it is usually at the behest of a struggling company working through unscrupulous brokers who are willing to sell promissory notes that the company may not be able to honor.

In the case of take-back mortgages, promissory notes have become a valuable tool to complete sales that would otherwise be held up by lack of financing. This can be a win-win situation for both the seller and buyer, as long as both parties fully understand what they are getting into. If you are looking to perform a take-back mortgage purchase or sale, you should have a talk with a legal professional and visit the notary office before you sign anything.

Trading Candle Cheat Sheet:

--

Further Reading/Source/Resources

Friend of the People -- Enemy of the State.

--

I am leaving these images I made here until I figure out one that fits properly and looks right for the first/main image for the post/series.

--

Since Steemit dev's changed the size of the picture frame that shows, it has honestly been a real problem getting images to match the screen, it was perfectly fine months ago before they messed around with it.

SMH.

Thanks for reading, have a nice day.

PixaBay has tons of free pictures for us all to use!!!

Super Easy/Fast Picture Edits / Resizing at: http://www.picresize.com/ and also https://www298.lunapic.com/editor/

If you liked this blog post - please Resteem it and share good content with others!

--

Some of my recent blogs:

--

https://steemit.com/bitshares/@barrydutton/life-in-crypto-is-like-22-or-ico-responsibilities

Most Images: Gif's - via Giphy.com , Funny or Die.com / Pixabay. Today:

If you feel my posts are undervalued or you want to donate to tip me - I would appreciate it very much.

--

LiteCoin (LTC) - LKdsnvSXk9JW99EiNicFMGKc1FXiBo9tUE

Monero (XMR) - d8ecb02c09f70ec10504b59b96bc1f488af28b05933893dfd1f55b113e23fbff

EOS (EOS) - 0xD37bEFf5bf07E3aa432de00cE0AaA8df603A4fB0

Ethereum (ETH) - 0x3Ad69Ff057C9533ca667B2d7E3E557F5eeFd4477

Ethereum Classic (ETC) - 0x5ab2b08d4ce8d454eb9d1ecc65c6d8b0c5f9784c

Bitcoin (BTC) - 18J6RRuzX4V7b2CDbx7tWZYNBLkkGWsvWX

DASH - XgZvsvSZgPkNbmGbRhc3S1Pt2JAc7QHwiS

PIVX - DA3azxQqJiX9t7EviuacpamfNhMi2zGAUh

Stratis (STRAT) - SNsJp6v1jXvKWy4XcXSXfNQ9zhSJJppJgv

ZCash (ZEC) - t1aCPEYELkGaf3GtgGTiCEDo7XfPm4QEwmL

Please note -- I will have limited internet access for awhile -- so PLEASE do not be upset that I cannot reply right away, or to everyone. I am dealing with some changes, and will have limited time online and will be happy if I get a few blog posts up a week.

This has really upset some people but I do not force my opinions on others, or need to communicate every detail of my life or issues, most people do not care anyways. I invested around 10 hours or more a day on Steemit most of my first 13 mths here, trying to build community, put out content and engage people, help and donate to people, and I just do not have that time in my life right now, and that includes for replies and voting/curation.

I have done my best, sorry if you do not understand like some are clearly having a problem with. It's a blogging platform, and I will do my best at everything, and to keep blogging.

Carry On.

--

LiteCoin (LTC) - LKdsnvSXk9JW99EiNicFMGKc1FXiBo9tUE

Monero (XMR) - d8ecb02c09f70ec10504b59b96bc1f488af28b05933893dfd1f55b113e23fbff

EOS (EOS) - 0xD37bEFf5bf07E3aa432de00cE0AaA8df603A4fB0

Ethereum (ETH) - 0x3Ad69Ff057C9533ca667B2d7E3E557F5eeFd4477

Ethereum Classic (ETC) - 0x5ab2b08d4ce8d454eb9d1ecc65c6d8b0c5f9784c

Bitcoin (BTC) - 18J6RRuzX4V7b2CDbx7tWZYNBLkkGWsvWX

DASH - XgZvsvSZgPkNbmGbRhc3S1Pt2JAc7QHwiS

PIVX - DA3azxQqJiX9t7EviuacpamfNhMi2zGAUh

Stratis (STRAT) - SNsJp6v1jXvKWy4XcXSXfNQ9zhSJJppJgv

ZCash (ZEC) - t1aCPEYELkGaf3GtgGTiCEDo7XfPm4QEwmL

Please note -- I will have limited internet access for awhile -- so PLEASE do not be upset that I cannot reply right away, or to everyone. I am dealing with some changes, and will have limited time online and will be happy if I get a few blog posts up a week.

This has really upset some people but I do not force my opinions on others, or need to communicate every detail of my life or issues, most people do not care anyways. I invested around 10 hours or more a day on Steemit most of my first 13 mths here, trying to build community, put out content and engage people, help and donate to people, and I just do not have that time in my life right now, and that includes for replies and voting/curation.

I have done my best, sorry if you do not understand like some are clearly having a problem with. It's a blogging platform, and I will do my best at everything, and to keep blogging.

Carry On.

Great idea, helping all the new people to understand investing techniques. There are SO many new people in this space it can be overwhelming at times. I have people asking me questions EVERY single day now about Bitcoin and cryptos.

Hey man!

Yes, no doubt about that. All of it.

Nice to hear from you again!!

Interesting Tips,

Thanks for the information.

Wow amazing

Really?

What part?

I did not expect it to rise that fast

The more I read about personal finance, the more tiny gems like these I stumble upon. I wish when I turned 18 someone handed me a big list of tips like these, instead of piecing them together over the last few years :P

Thanks! You are right.

I have a background in real estate so I have more info than some on this aspect -- so I really thought it was important to emphasize this aspect twice in this post, accordingly.