We Are In Housing Bubble 2.0

Source:http://images.fineartamerica.com/images-medium-large/burning-house-ryan-shaffer.jpg

{kind=link}

It’s painful to listen when the herd mentality of the masses make statements like: “Why is housing getting so expensive?” It demonstrates a fundamental lack of understanding of what the underlying economic issues are that effect this market. We have “affordable housing” programs, down payment assistance, and financing options. But for some reason the old economic model of getting a head in life via the American Dream of buying a home and watching it appreciate in value, is just not working. On top of that, the millennial generation is just starting to enter the workforce and they are experiencing a less than forgiving rental market, which is designed for those starting their careers.

This just doesn’t make any sense does it? Well, for those who pay just the slightest attention to what is going on, it certainly does. The real crime is that no one will bother to explain these concepts, and this certainly will not be taught in any school.

The truth is: not only is the United States in a real estate bubble, but the entire hosing market is not real and has absolutely no basis in reality. There are so many extremely technical arguments to support this, but what is key are just these two points:

- The Federal Reserve manipulates interest rates

- The mortgage and financing sector is a game of shuffling paper

The fist point is very easy to make. It is common knowledge that the Fed’s job is to manipulate interest rates, and they will even admit to it. Most are not aware of the Fed’s process for doing this. It is a convoluted process of purchasing Treasury notes, which they dub “open market operations,” which creates artificial demand for the notes increasing their price and conversely lowering their yield. The mortgage rates cannot be lower than the 10 year Treasury yield, otherwise investors would borrow to the US Government rather than home buyers.

But that’s not really the point. Who cares how it’s done? The point is that a private central bank (the Federal Reserve) arbitrarily controls the rate of interest, which is quite literally the price of money, since it is what we pay for the service of borrowing other people’s money.

The second point is a look at how the lending institutions were able to create a bubble in housing in the years leading up to 2008. And since nothing has fundamentally changed since then, we can assume that the same type of crisis will happen again. What caused the 2008 financial crisis was artificially low interest rates, delegated by the Federal Reserve under the management of chairman Alan Greenspan, and lax regulation of the securitization process in which these mortgages were sold. In a normal world, there would have been no issue with banks using leverage and taking on risk in order make these types of loans happen. But because of the “Greenspan Put,” these financial institutions took on larger amounts of risk that they otherwise wouldn’t have because the government guaranteed their safety. This created a mentality among lenders that the risk is: “not my problem.”

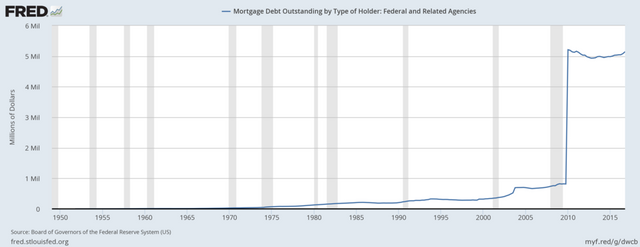

The complete lack of personal responsibility from all parties comes from the mentality of the Greenspan Put - that the Fed under the management of Alan Greenspan would inject money into the financial institutions, or the US Government would use taxpayer money to “bail out” the institutions like they have previously. This made a liquidity crisis with massive mortgage defaults an irrelevant concern as they continued to lend. The retail banks (the ones you and I bank at) have absolutely no responsibility what so ever when qualifying buyers since they could, once through the underwriting process, sell directly to the Government Sponsored Entities (GSEs): Fannie Mae and Freddie Mac. These two served as an intermediary between retail banks and the Government / Fed. This served two purposes, 1) remove the mortgages-backed securities (MBS) from the balance sheets of the retail banks so that they can do more lending, 2) to transfer risk (“not my problem”). Transferring the MBS’ to Fannie and Freddie kept the balance sheets of the retail banks clean. Here is where that mortgage debt ended up after 2008:

The proposed (non)-solution was simple; prop up the zombie GSEs Fannie and Freddie. Shortly after the chaos in 2008, Fannie and Freddie were nationalized and then the US Government secretly became the biggest holder of mortgage debt. This, I remind you, is on top of the hundreds of billions of dollars given to the Wall Street institutions with the TARP bailout program. Not only did the TARP program not work to fix the underlying issues in the market, but it was also completely unnecessary as David Stockman – Ronald Regan’s budget director – outlines in his book The Great Deformation.

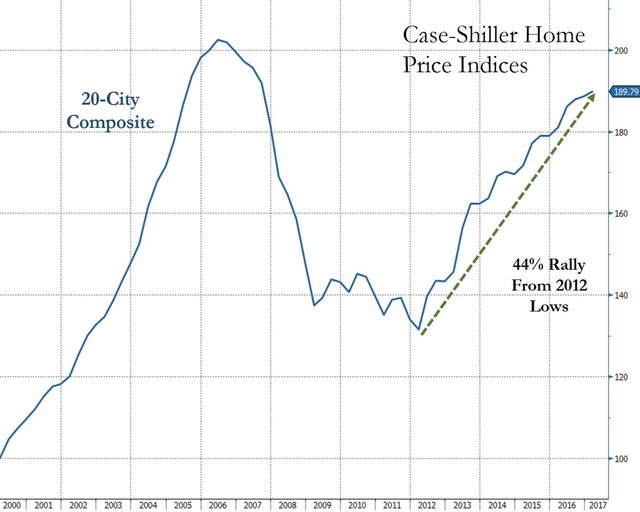

The crisis, of course, was played off by media and the financial authorities as sudden and unpredictable. Certainly no one could have foreseen this happening, except, or course Ron Paul, Robert Kiyosaki, Peter Schiff, Mike Maloney, Robert Shiller (creator of the Case-Schiller index), and even Alan Greenspan himself who had retired from the Fed in 2006. Most of these individuals were dismissed as crazy and even labeled “conspiracy theorists.”

There is one more point that must be made about the banking system before we go forward and look at the cracks in the system. The reason why it was so simple for the people stated above to make such a daring forecast in the face of such criticism is their fundamental understanding of the system. This understanding is best described with an example: during the last campaign for president of the United States, Donald Trump was interviewed by the Today show in which he described part of his success being that he received “A small loan of a million dollars.” Of course, the media and opposition used this statement against him in order to drive a narrative that he was disconnected to the average person, who would obviously think that a million dollars is a lot of money. The truth of the matter is, a million dollars is not a lot of money. Donald Trump and those who has predicted the real estate bubble have a fundamental understanding of the banking system.

This system is very simple to understand, and so I will explain it in simple terms, and it may come as a surprise. Most believe that when they borrow money from a bank, they are receiving some other member’s deposit and then pay interest on that money. This may have been true a long time ago, but it is no longer the truth today. The truth is, if you were to borrow money form the bank and have the funds deposited into your account or escrow, those funds did not exist before you borrowed them. This of course means that you are paying interest on money that also did not exist, making the interest you pay to the bank all profit. If you do not believe that this is true, you can research “fractional reserve banking.” I must confess that there is a small detail that was left out, for the sake of full disclosure, not all the money you receive is brand new currency, just 90%. The bank is required at this moment to have 10% of the money that it has lent you on deposit. This is the “fractional reserve” part of the system. Needless to say it does not distract from the truth that individuals who borrow funds to purchase homes do so by effectively increasing the money supply. This is a large contributor to the inflation of prices in the housing market.

Let’s look at where we are. It is indicative of the first chart included in this writing that there has been almost no attempt by the GSE’s to reduce the size of their holdings of the mortgage debt. But are these houses filled with happy home owners? No actually, they are vacant. There was an estimated 17.3 million vacant homes in the United States in 2015, the most current year being reported by the US Census Bureau. This number is not much better than the 18.5 million that were reported in 2011 along with a homelessness number of 3.5 million reported in the same year.

With so many homes vacant, you would assume that the price of housing would be getting cheaper. Not true either, in fact there has been a 44% rally in housing since the lows in 2012 and is fast approaching its pre-2008 historic highs according to the Case-Schiller home price index.

Of course rental markets are affected by this trend as well. Zillow.com reports that the current fraction of the average American’s income spent on rent is at 29.5% which is an 18.8% deviation from the historical average.

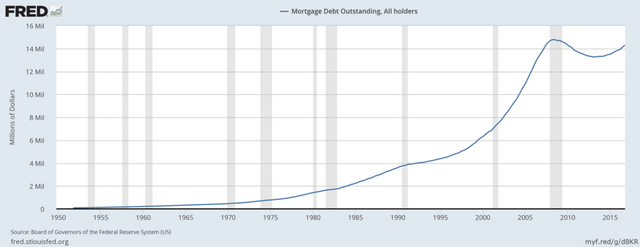

Even the most esteemed economist cannot explain a situation in the free market where vacancies increase at the same time prices also rise in perpetuity. It raises the question, are the banks holding on to inventory of vacant homes in order to artificially prop this market up? And where are American’s getting money for what is being sold on the market currently? That answer is simple. Total mortgage debt outstanding has not decreased, credit is still being handed out to wanna-be home owners.

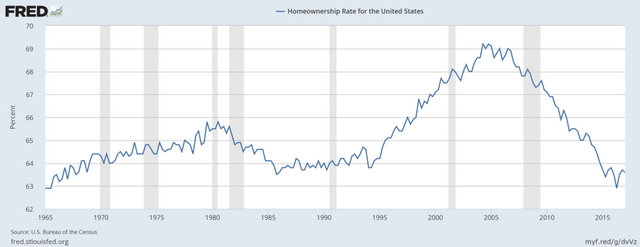

Also home ownership rates are at historic lows according to the Fed’s measurements that go back to 1965.

Fundamentally nothing has changed since 2008. Even the 0% down financing options have been replaced with FHFA’s 3.5% down payment assistance for new homebuyers. Behaviors of borrowers are reminiscent of the “irrational exuberance” of bubbles that have formed and subsequently popped in the past decades. The question is not weather or not this bubble will pop, the true questions are when and to what extent? I cannot and will not speculate about when, but if there are any parlor tricks left to use in this market, we can rest assured knowing that another bubble will take the place of this one. Otherwise, we may be looking at a correction to prices seen back in the pre-1960s when the majority of American’s bought homes with cash. How exciting would it be for the already cash-strapped American if houses were tens of thousands of dollars instead of hundreds?

Main points to remember: The real estate market is not real since the Federal Reserve manipulates interest rates. And prices are being propped up with easy money and credit (90% of which did not exist previously) despite there being millions of vacant homes that may not actually be on the market.

Sources:

Fannie Mae, Freddie Mack, and the Credit Crisis of 2008. Investopedia LLC http://www.investopedia.com/articles/economics/08/fannie-mae-freddie-mac-credit-crisis.asp?lgl=lg-mt

How To Use Real Estate Trends To Predict The Next Housing Bubbble. Teo Nicolais. Harvard University http://www.extension.harvard.edu/inside-extension/how-use-real-estate-trends-predict-next-housing-bubble

Table 7a. Annual Estimates of the Housing Inventory. United States Census Bureau. https://www.census.gov/housing/hvs/data/histtabs.html

Housing: It’s a Wonderful Right. Tanuka Loha. Amnesty International. December 21, 2011. http://blog.amnestyusa.org/us/housing-its-a-wonderful-right

The Rent is Too Damn High. Krishna Rao. Zillow.com. April 15, 2014. http://blog.amnestyusa.org/us/housing-its-a-wonderful-right/

Graphs:

Federal Reserve Bank of St. Louis - FRED data

https://fred.stlouisfed.org/series/MDOTHFRA

https://fred.stlouisfed.org/series/MDOAH

https://fred.stlouisfed.org/series/RHORUSQ156N

Case-Schiller Price Index

[taken from Zero Hedge article] http://www.zerohedge.com/news/2017-04-27/home-prices-continue-surge-sparking-fears-bubble-20

Books

Robert J. Schiller, Irrational Exuberance. Princeton University. 2005

David A. Stockman, The Great Deformation. PublicAffairs. 2013

Video

Mike Maloney, The Real Big Short: In 2005 Maloney Predicts The 2007 Crisis At Silver Summit 2005. Oct 3, 2012. https://www.youtube.com/watch?v=PAQmXaJEc7k

Good stuff! I too believe that this current housing market will collapse again like in 08'. It's just a matter of time, but who knows when. If you haven't seen the 'The Big Short', I HIGHLY recommend it! Might be a top 5 favorite movie of mine now. The fact that they KNEW what they were doing is what pisses me off the most, but yet they KNEW they would get bailed out. I see your fairly new here, keep posting good content and you will be appreciated. Steem on brother!

Thanks bud, I am glad this helped.

I really enjoyed this! Thank you.

I also just saw you are from Minneapolis, same here.

Another sotan', they just keep coming and I love it!