Introduction to Stable Coins

The Problem with Crypto Currencies

As the prices of Bitcoin and other crypto assets soar, and digital currency becomes more and more recognized by the mainstream, the question that everyone is bashfully avoiding is why merchant and business adoption is so slow. You cannot buy coffee, or shoes, or a dinner with Bitcoin, or any other cryptocurrency, and no one seems to be addressing the real reason why. Instead, we are presented with one of two arguments: either it will simply take more time for mainstream adoption to really take off, or there are regulatory or technical concerns which deter small businesses, who are the first likely adopters. While there are some brave companies that are broadcasting their foray into crypto with Bitcoin Accepted Here stickers, widespread adoption has been lacking. Reasons for this slow and disappointing development include the following:

Volatility

Businesses won’t adopt Bitcoin, etc. because they simply cannot afford to. A company needs to pay rent, buy supplies, sell products and services, and pay its employees on an exact schedule. Cash flow is incredibly important for small businesses to survive, where insolvency and bankruptcy are real concerns. Accepting Bitcoin, for these companies, is a bit like accepting lottery tickets as money; the enormous volatility in the crypto markets make it impossible to predict whether a company’s balance sheet will be in the black or in the red on the exact day it has to pay its employees, or when rent or taxes are due. The risk is simply too great, and there is no real incentive to adopt crypto that outweighs the dis-incentive of volatility risk.

Some argue that Bitcoin will eventually achieve stability, and that it’s violent market behavior is currently due to growing pains and relatively low trading volume compared to other major currencies. Further it has been suggested that the futures and derivatives markets will bring stability to crypto assets, because institutional investors will look to achieve predictable and specific price targets. While trading volume and market maturity may help reign in volatility, there is simply no precedent that suggests we can achieve stability on a level of a major currency.

Gold, one of the most mature markets in the world, sees regular fluctuations of more than 10% per year, losing more than 27% in 2013 alone. Ironically, the volatility of Gold has increased over time, rather than decreased, which suggests there is no real positive correlation between market maturity and price stability.

Deflationary Incentives

It is a well-established economic fact that inflation is one of the drivers of consumer spending. If we can be reasonably certain that our money will be slightly less valuable in the future, we are incentivized to spend it now, which is good for the economy. Bitcoin on the other hand is famously deflationary, because there is a limited supply and growing demand. It is clear that spending Bitcoin now is almost always a mistake, because spending it in the future will likely be more beneficial due to its increased value. Thus, consumer spending is discouraged.

There is a contradictory mindset in the Bitcoin community which proclaims that Bitcoin will be the new world currency, and yet instructs its members to “HODL,” a meme derived from a misspelling of the word “hold” and sometimes mistakenly used as an acronym for “Hold On for Dear Life”. The meme expresses both the belief that selling Bitcoin is almost a betrayal of its principles, and a distaste for those who sell their coins due to short term market fluctuations. While there are those who use Bitcoin in their day-to-day life as a matter of principle, they are arguably wrong to do so, and elect to act against their own self-interest in the hopes of fulfilling the dream of universal acceptance which is unlikely to manifest itself in reality.

Lending and Borrowing Markets

Lending and borrowing are one of the most important, if not the most important activities of the financial world. Without loans and lines of credit, businesses could not function, and very few people could afford houses and cars. Loans only work well because we have faith in the stability of money. If, for instance, we lend someone one Bitcoin at a value of $20 thousand and the price collapses down to $6 thousand, as it has in early 2018, we lost an enormous amount of money. If, on the other hand, we borrow one Bitcoin and its price triples, we may never be able to pay back the loan, especially if the price of Bitcoin keeps rising. We would have to declare bankruptcy or be stooped in eternal debt, which makes the prospect of borrowing extremely risky.

For these and other reasons, it is unlikely we will ever see mass adoption of Bitcoin as a coin of commerce, because it is fundamentally a commodity and not a currency. It is digital gold, which has an important place in the new economy, but will not replace the Dollar, Yen, or Euro. In order to do business, and engage in the long-term activity of finance and commerce, we need more than just a valuable token; we need stability.

Stable Coins

There has been considerable effort and innovation put into solving the problem of volatility, and it has not yet garnered the attention it deserves. Stable coins are a new class of cryptocurrencies under development which hope to revolutionize the crypto world, and the world economy by bringing decentralized monetary policy into the blockchain space.

We can group the various stable coin projects into three distinct categories, which evolved chronologically and are discussed below. However, the most important conceptual insight that stable coins all share is the proposition that money is a product, produced by a company and subject to market forces, just like any other product. This is true for both cryptocurrency and conventional money like the USD, which is created and regulated by the government and Federal Reserve. It is much easier to understand the mechanics and ideas behind stable coins with this simple concept in mind.

Tokenizing Physical Goods, The First Generation

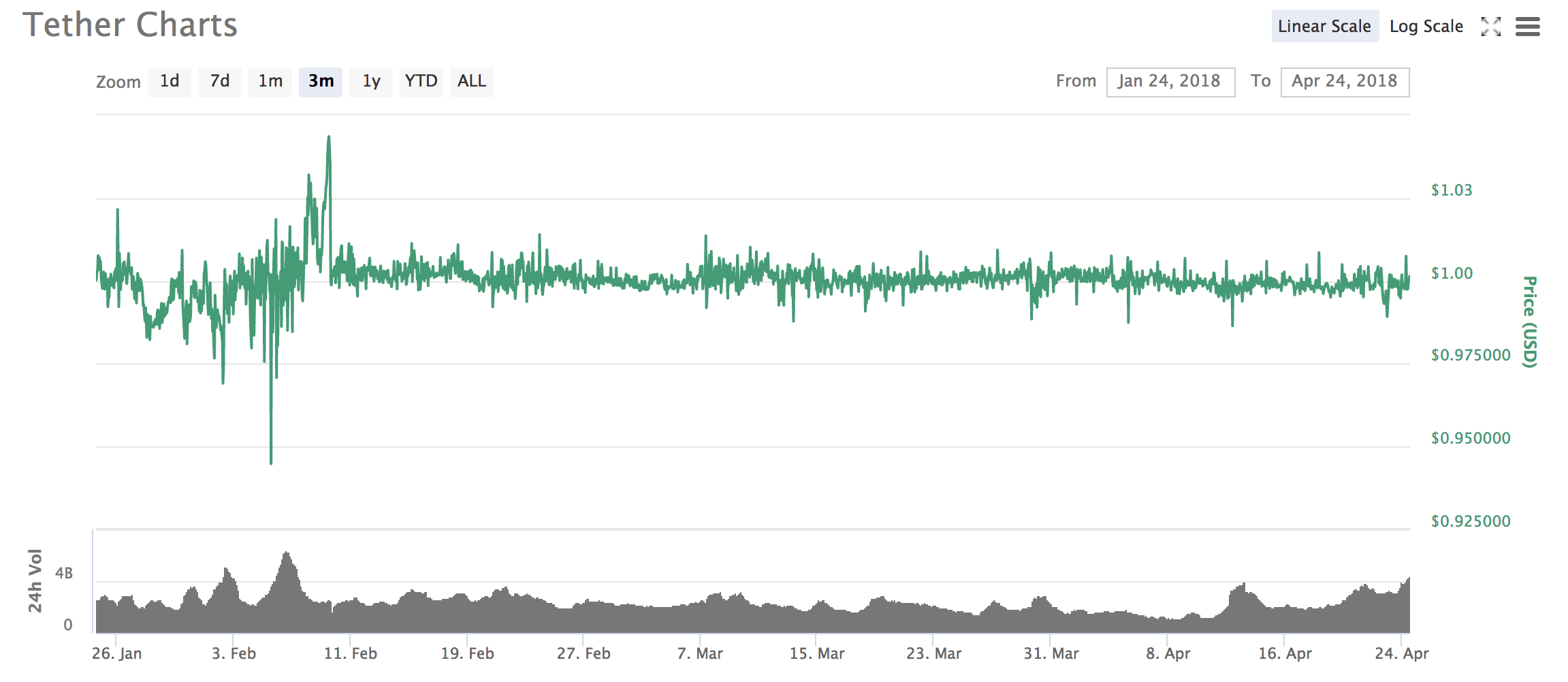

Most crypto traders who are active on Bitfinx and Binance have heard of, and used, the USD-Tether. Tether is a crypto currency that was invented for a simple reason: to let exchanges and traders interact with one another in US Dollars, without actually switching between crypto and fiat money all the time. Keeping everything on the blockchain instead of going back and forth between fiat money and digital tokens saves enormously on administrative costs, taxes, and time; it is vastly more efficient.

The mechanism behind Tether is straight forward: The Tether company creates one coin for every US Dollar it receives and locks away in its bank account. Thus, a one-to-one backing guarantees price stability against the dollar, because everyone already trusts the dollar. The Tether coin uses the Omni protocol to ride on top of the Bitcoin blockchain, guaranteeing secure transactions and transparency.

Although Tether is great in theory, and has maintained excellent price stability, it also suffers from several weaknesses. It is not decentralized, but controlled entirely by Tether Limited, which means it is vulnerable to attack and corruption. Its backing funds are locked up in a few bank accounts in Singapore and Hong Kong, which means that the money can get seized or frozen by governments, adding a high degree of 3rd party risk.

Tether was not conceived of as a world currency, but as a tool for exchanges to increase efficiency and avoid taxable trading events for the exchanges and their users. Since Tether is closely linked to the USD and wants to avoid legal restrictions or adverse government action, they have instituted a strict Know-You-Customer framework, which makes it very difficult for individuals to hold Tether themselves. Rather, the exchanges hold the stable coins, while their users submit identity verification paperwork in order to trade them. In its conception as a tool for exchanges and opposed to several other stable coins, Tether lacks various incentives for users that would make the currency attractive.

Further questions have been raised about Tether’s business practices and transparency, alleging that it essentially engages in fractional reserve banking and thus does not hold one Dollar for every Tether it creates. Whether or not these concerns are warranted, they may undermine the entire currency whose value is predicated on trust. Thus, the actions and possible abuses of a single company could collapse the entire Tether economy.

Daunting as all these concerns are, Tether is consistently one of the most frequently traded cryptocurrencies by volume, not because it is particularly attractive to investors, but because stable coins are necessary for the crypto economy to function.

Connecting real world currencies or goods with the blockchain via tokenization is not unique to Tether. DigixDAO, for example, have recently put physical gold into the crypto space, and several other companies are working on doing the same for real estate and other commodities. All of these efforts have one thing in common, which is known as the Oracle Problem. In short, it is difficult to ensure that the real-world good is properly and securely linked to its digital counterpart if there is no centralized authority to verify the authenticity of that link. For instance, if an ounce of gold is put on the blockchain, that ounce does not cease to exist in the physical world and can potentially be sold, destroyed or lost without the digital world reflecting this change, creating a double spend attack vector on the system. For more information about the Oracle Problem, see upcoming publications.

Digital Collateral, The Second Generation

Instead of relying on a physical good to put onto the blockchain like gold, or the USD, second generation coins are backed by digital collateral, eliminating the counterpart risks described above. The issues of corruption and centralized authority may be solved by moving a stable coin issuing company into the blockchain space, using a Decentralized Autonomous Organization (DAO). The DAO exists as a price volatile token, granting voting rights and promising dividends to its owners, while the stable coin token created by that DAO is its product. Thus, this generation of coins employs a two-token model.

The DAO publishes a smart contract which enables users to lock up their other crypto assets, like Ethereum and Bitcoin in a Collateralized Debt Position (CDP) to instantiate new stable coin tokens. These CDPs typically take into account the volatility of the underlying asset, which means they require heavy over-collateralization in order to remain collateralized even if the markets fall substantially.

In practice, this means that any Ethereum or Bitcoin user can lock up, say, $150 of their funds in a smart contract, and thus create approximately $100 of stable coin tokens, which may then be freely used. The user holds a special right to the locked-up Ether or Bitcoin, which can be reclaimed if those $100 are payed back into the contract.

The reason this system achieves price stability is because of an interplay of complex mechanisms that allow for a contraction and expansion of the money supply, as well as various incentive structures which ensure proper over-collateralization.

Algorithmic Stability, The Third Generation

When Richard Nixon severed the connection between the USD and gold in 1971, It took some time for the general public to acknowledge that it’s money was no longer backed by anything but trust in the US government and Federal Reserve. The development of stable coins may follow a similar pattern of being collateral backed until it is deemed no longer necessary, or efficient. At that point, the third-generation model of coins, algorithmically stable coins, may take over.

The limiting factor on second generation coins is similar to that of the gold standard in that it does not scale terribly well. If we consider that the entire M2 money supply of the world is in excess of $50 trillion, and all cryptocurrencies combined are worth a measly $300 billion, the endgame of stable coins seems unattainable using a collateral model. The long-term vision is of course that all, or at least most, currency will be replaced by stable coins, which means that at an average rate of 150% over-collateralization, we need more Ethereum and Bitcoin backing those coins than all the money in the world could possibly buy. This is a problem.

Algorithmically stable coins seek to achieve stability purely by implementing automated monetary policy, replacing the role of the Federal Reserve with lines of code. Essentially, there must be mechanisms which allow the issuing agency (also a DAO), to expand and contract the money supply, and create incentives, such that market forces will naturally stabilize the coin’s price. Several models have been proposed to achieve this by issuing bonds, or credit tokens, which promise future returns to the owners, while others seek to freeze proportional amounts of coins that are placed in special smart contracts in the hope of being issued newly minted currency.

NuBits implements algorithmic stability with a two-token model consisting of network tokens and currency tokens. Network tokens represent shares in the entire network, and allow owners to vote on the mintage of new coins, creating a mechanism to expand the money supply. Conversely, if the price of NuBit currency tokens falls below the USD, users can elect to park their coins in special accounts, which essentially removes them from the money supply, creating upward price pressure. These parked funds then generate interest, by being issued new coins when the network votes to mint new ones.

Carbon is another interesting project, which is still waiting to be implemented, but has already garnered some attention. It operates on similar principles as NuBits, except that the money supply is contracted using an automatically triggered auction that sells network shares (Carbon Credit Tokens), for stable coins and then burns the proceeds, eliminating the excess supply of coins and creating upward price pressure. An interesting aspect of Carbon is that it will not be implemented on a blockchain, but has elected to sign on with Hedera Hashgraph, a non-open source platform.

Although sound in principle, algorithmically stable tokens are still a very new and risky family of coins that needs to develop and learn from its failures. NuBits, for instance, collapsed in March of 2018, and fell to $0.28, before showing signs of rebounding. As of writing, it is stabilizing at around $0.60, which is still catastrophic in light of what it is supposed to do. One can hardly imagine an economy in which the entire world currency suddenly collapses overnight, a financial shock that would dwarf any hyper-inflation and recession yet.

Outlook

While third generation coins provide theoretically elegant solutions to an otherwise messy problem, it is unlikely that algorithmically stable coins will be successful in the near future, for several reasons:

Rapid growth and skewed incentives: Algorithmically stable coin projects are likely to fail before they even get going due to their inorganic growth patterns. When a coin first gains tractions, the issuance of new coins is in the interest of those who are already holding. That is, early adopters stand to gain more due to their relatively large credit, or network share positions. Thus, they are incentivized to advertise the coin and attract attention and excitement. This can lead to a hype cycle, which results in many new buyers coming into the market, driving up the price. However, in an attempt to stabilize the price, the algorithms will issue more and more coins that then get distributed to credit and network share holders. Due to the nature of price slippage, money flowing into a given market can have an amplified effect on that market, thus necessitating enormous coin issuance spikes to keep prices stable. Once the new coins exist, there is no sufficiently large network of adopters, and holders will want to cash in on their profits, creating downward price pressure and risk of destabilization. Since most potential profit is with early users, there is no real incentive to stick with an older coin, once a new one comes along and repeats the pattern.

Unnecessary: In the short to medium term, there is simply no reason why we should abandon the relative safety of commodity backed money, and venture out onto the thin ice of algorithmic coins, especially in light of their recent failures. Second generation coins have a much better track record, and are not limited by issues of scalability until the stable coin economy grows by several orders of magnitude. This growth in stable coins will automatically lead to a rise in commodity prices, since demand on commodities will increase along with the supply of commodity backed stable coins, mitigating the problem of scalability even further.

Infinite supply: In a fiat system, whether it is crypto based or government based, the money supply is always increasing. Regardless of whether the Federal Reserve, or the DAO elect to diminish the money supply, the mechanism by which they do so is by promising bond or credit buyers more money in the future in the form of interest. Thus, inflation is a feature of the system, which is likely to eventually cause problems.

Dependent on trust: The difference between the USD and an algorithmically stable coin is that the stable coin relies solely on trust and voluntary participation. The system can only work as long as every member stands to benefit from it. This is in stark contrast to government issued currencies, which rely on trust, but are less interested in voluntary participation. That is, instead of only banking on our own benefit through participation, we can also trust in the wrath of the state should we elect not to. At the end of the day, the essence of government is still force. While it may not be entirely accurate to claim that the USD gains its value from a threat of force, that threat of force is nonetheless its last line of defense. Stable coins cannot defend themselves in this way if people should start to distrust them, and thus they may be inherently more prone to failure.

Conclusion

As we have seen, there are three categories, or generations of stable coins in development. While some rely on a one-to-one backing, others choose to derive their value from other commodities, or from trust in their automated monetary policy. Stable coins are one the forefront of cryptocurrency innovation and represent the cutting edge of what blockchain technology is capable of achieving for money.

Instead of taking an idealist approach that money is a form of expression, they pragmatically assert that it is nothing more than a regular product that can be manufactured and fine-tuned to fulfil a desired function. It is in this fine tuning, that many different projects compete against one another in order to create a future in which money is global, frictionless, stable and decentralized; a system which will revolutionize the world economy in terms of efficiency and sheer possibility.

It seems as though commodity backed stable coins will start seriously competing with Tether for market dominance, and are likely to succeed as the shortcomings of a centralized, first-generation stable coin become more and more apparent.

I like this. Followed you

Thanks! Much appreciated

Coins mentioned in post:

Congratulations @blockspaceinc! You received a personal award!

You can view your badges on your Steem Board and compare to others on the Steem Ranking

Do not miss the last post from @steemitboard:

Vote for @Steemitboard as a witness to get one more award and increased upvotes!