Invox Finance Platform: The Populous Killer?

Image source

I found out about Invox Finance Platform through @moworks. Reading through their whitepaper, you will come to realize two things. First, if you are not familiar with running a business, it can be difficult to understand. Second, the market that Invox is looking to disrupt is the same market that has been disrupted by Populous.

Dealing in Cryptocurrency, you would have heard of Populous. Populous is a rather niche project that aimed at solving the problem of invoice financing.

The Problem & Solution With Invoice Financing

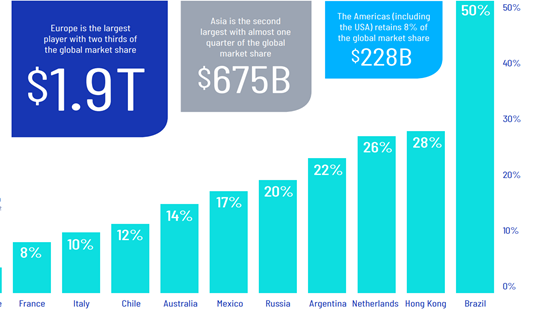

Invoice financing is a 2.85 trillion dollar market that was dominated by banks. I say 'was' because populous came along. To give you an idea, a business may need cash quick but are not paid for their services yet. The bank would conventionally buy up their invoice and provide them with cash.

Invoice Financing's Biggest Players by country Image source

The banks however could set some rather difficult terms since they monopolize the market. Populous disrupted the market by kicking out the banks. Since Populous is decentralized, it could just have individuals from all over the globe bid for the invoice. Thus, providing the investor who wishes to buy the invoice and seller of invoices a win-win scenario.

However, Populous is not without its problems.

Improvements by Invox

The Invox Finance Platform made a few improvements to Populous. Firstly, it added verification from the customers of a business. While Populous provides a platform where investors can invest by buying up an invoice, it has not way to verify if the invoice that the investor is buying is real or a fake. The Invox Finance Platform however connects the customers to the entire transaction with the purpose of verifying if the seller of the invoice is legitimate.

The next point in my opinion is definitely an improvement over Populous. Each investor is required to bid against each other on the Populous platform. While that ensures healthy competition, it does not allow investors who are unable to outbid the investors with bigger wallets a chance to participate. This makes the market more centralized, akin to the days when invoice financing was dominated by banks. The Invox Finance Platform manages this by providing each investor equal access to the sellers, thus eliminating the need for investors to undercut each other.

The problem however is that the process is yet to be detailed. Hopefully Invox would clarify how equal access can be provided.

Time Will Tell

Image source

Another important point is that Invox is ran by a very experienced team. The founder of the project is Alex Mezhvinsky who is the managing director of ABR finance. With an experienced leader and a team, this should help enhance the project's chances of success in the long run.

That being said, it is rather too early to tell if Invox or Populous will dominate the market. There are a myriad of factors involved in this. What's for sure however, is that the Invoice Financing market is now further disrupted with Invox Finance Platform.

IF you are keen, do check out their website and sign up for the presale which will be starting soon.

InvoxFinanceTokenSale

This is an entry to the following competition

Thanks for this look into Invox, @alvinauh. I had never heard about Invox until now - thus, I am officially putting them on my growing list of crypto-companies to watch and/or invest in. Can't get enough of this crypto revolution!! Great work!

Thanks! yes, it is a revolution now if only there are some that would pay me dividends for doing nothing..haha

Congratulations! This post has been chosen as one of the daily Whistle Stops for The STEEM Engine!

You can see your post's place along the track here: The Daily Whistle Stops, Issue # 73 (3/14/18)

The STEEM Engine is an initiative dedicated to promoting meaningful engagement across Steemit. Find out more about us and join us today!