Some witnesses have suggested reducing the discount to prevent SBD from strengthening too much, and while I agree this would be a good idea if we were not already (and probably inappropriately) paying high interest, I believe we should reduce or stop the interest first, and then assess the continued need (if any) for a feed discount.

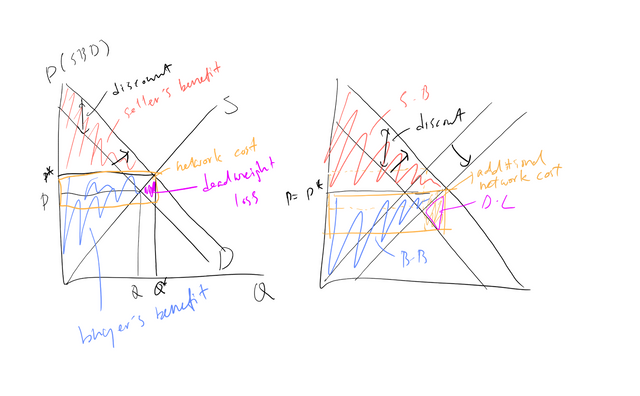

I am not against lowering interest rates in general, but I am against lowering interests as a tool of offsetting excessive demand of SBD caused by high feed discounts, as you are arguing. Here is a simple welfare analysis. (It's very very bad drawing though)

The left graph only has a feed price discount. It moves demand curve upward and increase both SBD price and quantity. But in this graph, the network is paying discount * Q* to SBD buyers and sellers (the distribution is determined by relative elasticity between buyer and seller).

In the right graph, I added lower interest rate that moves supply curve outward, hence we get the same level of SBD price, as you insist. However, we can notice there is more costs on the network, discount * (new Q - Q*), and still have deadweight loss. Your policy seems good in terms of SBD price, and benefits SBD buyers and sellers, but is obviously not good for the network (and consequently STEEM stakeholders).

Except that your analysis ignores the cost of risk to the network associated with the unaddressed higher debt amount in the first state. That is why the whitepaper warns that failing to follow the rules risks damaging the STEEM price (due to the cascading effects of static debt amount over the course of unpredictable price trajectories, which can easily include 50% drops, or of course much more).

Let me ask a question (preceded by a statement): If we follow the rules, and the system fails (reaches a broken peg or some other negative outcome) then we will know that the system as designed, including those rules, does not work and needs to be changed (or SBD simply removed). If we do not follow the rules, and the system fails (in the same manner) how do we know that the system (including the instructions given the witnesses) did not work? The answer is that we don't. I suggest that we follow the rules and see if they work, which they might. If they don't then changes will be required. Likewise if you have a proposal for how to design a pegging mechanism that not only maintains price parity but also as effectively manages debt risk at lower total cost, then it would be a good proposal. I don't believe that you do.

(You may object that the rules don't precisely address this situation, which is true, but it is clear that the current system state with the peg supported by a high interest is not intended. Increasing interest is only advised during a low debt situation. Since we have had high and cascading debt load (ratio) for months, starting at least when Dan suggested a feed discount, a remedy for a weak peg in a high debt ratio situation, how does it make sense that we even have high interest at all? Arguably it made sense as additional price support in the special situation of closely approaching the "haircut" rule, which risked provoking a run on the bank, but once that situation was avoided it should have been removed. Which of course is part of why I have been and continue to proposing decreasing it now.)

As you indicate in your diagram, any version of the peg has a cost to the network. This is clear as a peg is a manipulated construct that is costly to maintain. It is also a risky construct that requires that its risk be actively managed (in the current version of the system). If not, statistically the result is certain (eventual) failure. This active management includes ensuring that sufficient conversion incentive is offered to effectively manage/reduce high debt, even thought in the short run this clearly has a cost. Price parity is not enough, and that's why the white paper has multiple rules for different situations.

BTW, I'm not sure I agree with your complete analysis of costs. Over time higher interest is an ongoing cost. The longer the higher interest is necessary because more risk is built into the system state, the more than cost accures. By reducing risk both the feed discount and the interest rate can also be reduced (later), which reduces overall costs even more.

You are wrong because the cost of risk comes from high debt ratio instead of debt amount. And again, you still cannot prove that facilitating conversion has no negative influence on STEEM price.

Wrong again. If there is no discount, there is no cost to the network.

Actually I am doing following the rules now. The white paper says, "If SMD trades for less than $1.00 USD and the debt-to-ownership ratio is over 10% then the feeds should be adjusted upward give more STEEM per SMD"

When Dan suggested feed discount, SBD price was $0.88 and the debt ratio was 2.8%, which already did not meet the rules, but the debt ratio seems to rusing to 10% so it could be a proactive movement. Now, however, SBD price is over $1.00 and the debt-to-ownership ratio is under 10%, which is totally opposite to the high discount condition. (Please be noticed that the rule is AND statement, so violating either of them can reject it)

My account just earned some SBD interest. Who paid that? Interest is a substitute (under certain circumstances) for a feed discount. Both carry a cost.

Yes, it was explained that the 5% goal and 10% rules in the white paper were not sufficiently safe, after the team had reviewed the SBD mechanism some more. The 2/5/10 cutoffs in SBD stability were written with this in mind as well, to ideally try to keep debt closer to 1% and slow things down should it reach 2-5% followed by the eventual haircut (although I'm personally not convinced any of these rules, including even the haircut, actually do what they intended, but that's what the blockchain is implementing now)

The debt ratio is higher now.