Case Study 8: Taxation of Cryptocurrency - Mining (C Corp)

Index - https://steemit.com/tax/@alhofmeister/tax-blog-index

Introduction

To help facilitate a better understanding of the taxation of cryptocurrency, I've decided to put together a series of examples which increase in complexity to demonstrate the potential tax implications of investing in cryptocurrency. I'll break each example out to include the tax impact of the various transactions occurring in 2017 and the tax impact if the scenario occurred in 2018 to demonstrate the effects of the new tax law.

After reviewing my first example on mining, I found it to be too simplistic. In my next series of articles, I will significantly expand the example to include multiple types of business entities, the element of mining pools, the idea of multiple use property as well as the tax implications in 2017 vs. 2018.

Note that I am assigning the salary to the owner arbitrarily ($125 a month). The determination of what represents reasonable compensation for people engaged in the practice of mining cryptocurrency is beyond the scope of this article.

Scenario

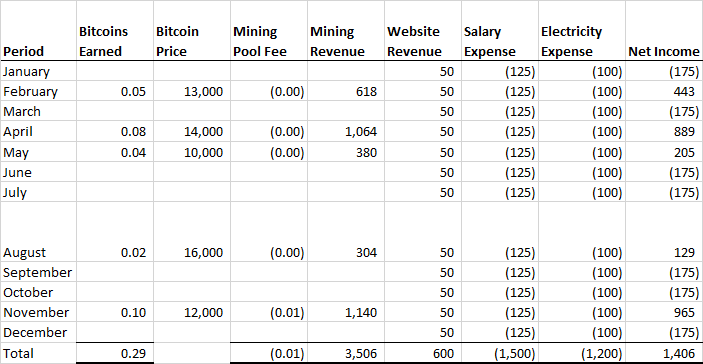

Taxpayer A decides to mine Bitcoin in January. To accomplish this task, Taxpayer A acquires mining hardware for $500, purchases software for $50 and joins a mining pool that distributes earnings net of a 5% surcharge. Each month, the mining operation increases the electricity bill by $100. In addition, Taxpayer A manages the website the mining pool uses to advertise and is paid $50 a month. Taxpayer A uses a personal computer that is also used for personal reasons (40% personal/60% business). The personal computer was acquired in a prior year and converted to it's current use. The computer cost $600 when it was originally purchased but it's current fair market value is $300. Over the course of the year, Taxpayer A receives the following payouts from the mining operation:

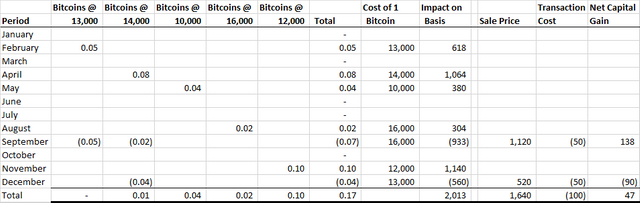

- In February, Taxpayer A is awarded 0.05 Bitcoins when it is valued at $13,000.

- In April, Taxpayer A is awarded 0.08 Bitcoins when it is valued at $14,000.

- In May, Taxpayer A is awarded 0.04 Bitcoins when it is valued at $10,000.

- In August, Taxpayer A is awarded 0.02 Bitcoins when it is valued at $16,000.

- In November, Taxpayer A is awarded 0.10 Bitcoins when it is valued at $12,000.

Additionally, Taxpayer A engages in the following transactions throughout the year:

- In September, Taxpayer A sells 0.07 Bitcoins when it is valued at $16,000. Transaction fees totaled $50.

- In December, Taxpayer A sells 0.04 Bitcoins when it is valued at $13,000. Transaction fees total $50.

Calculations Common in Both Years

Monthly Mining Operating Income

Capital Gains Schedule

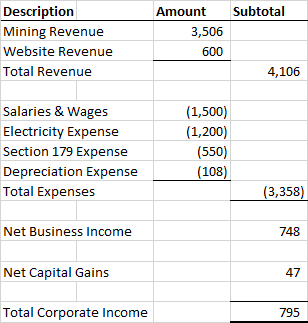

2017 Tax Treatment

Fixed Asset Schedule

Taxable Income Calculation

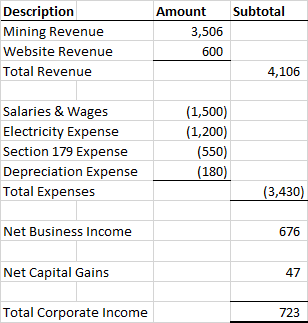

2018 Tax Treatment

Fixed Asset Schedule

Taxable Income Calculation

Disclaimer

Any accounting, business or tax advice contained in this communication, including attachments and enclosures, is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

@OriginalWorks

Thanks for sharing details and explaining the aspects we will have to focus for crypto taxation.

Anytime.