Case Study 5: Taxation of Cryptocurrency - Forks

Introduction

To help facilitate a better understanding of the taxation of cryptocurrency, I've decided to put together a series of examples which increase in complexity to demonstrate the potential tax implications of investing in cryptocurrency. I'll break each example out to include the tax impact of the various transactions occurring in 2017 and the tax impact if the scenario occurred in 2018 to demonstrate the effects of the new tax law.

Notice in this first example that there is no difference between 2017 & 2018 tax treatment. Also, I have included a more aggressive position that the Bitcoin Cash split would not result in a taxable event. This position is not recommended and would likely be overturned by the IRS. The IRS has not, however, specifically addressed the question of forks.

Scenario

(1) Taxpayer A decides to invest in Bitcoin. In January, Taxpayer A buys 100 coins at the price of $9 a coin with a transaction fee of $1 a coin spending a total of $1,000 to acquire the coins. (2) In March, Taxpayer A panics at a drop in the price of Bitcoin and sells off 10 coins for $6 a coin with a transaction cost of $1 a coin making a total of $50 off the sale. (3) In April, Taxpayer A decides to sell off 20 coins when the price of Bitcoin spikes to $16 at a transaction cost of $1 a coin making a total of $300. (4) Also during April, Bitcoin Cash is distributed to every holder of Bitcoin. Taxpayer A receives 60 coins of Bitcoin Cash when it is valued on the futures market at $7.50 a coin. (5) In May, Bitcoin Cash spikes to $11 which prompts Taxpayer A to sell 30 Bitcoin Cash with the transaction cost of $1 a coin. (6) In February of the next year, Taxpayer A decides to sell off his remaining Bitcoin at $21 a coin with a transaction fee of $1 a coin receiving $1,400. (7) In June of the next year, Taxpayer A decides to sell off his remaining Bitcoin Cash (30) at the price of $16 with transaction costs of $1 a coin.

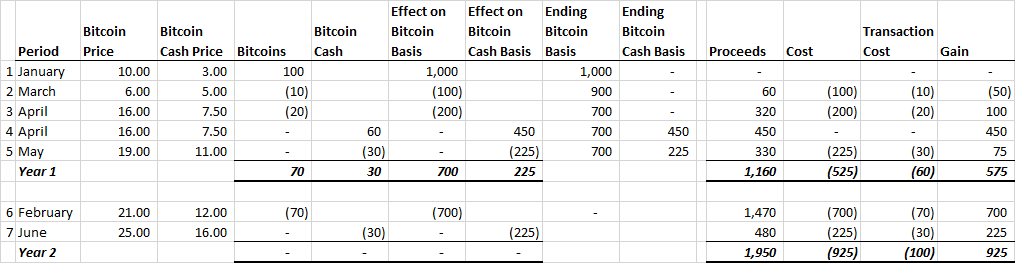

Conservative

In year 1, Taxpayer A would recognize $450 of ordinary income from the receipt of Bitcoin Cash as a result of the fork. Taxpayer A would recognize a total short term capital gain of $125. This gain is comprised of $100 for the sale in April of Bitcoin and $75 for the sale of Bitcoin Cash in May offset by a $50 loss from selling Bitcoin in March.

In Year 2, Taxpayer A would recognize long term capital gain of $925 on their 2018 individual income tax return. This gain is comprised of $700 from the sale of Bitcoin in February and $225 from the sale of Bitcoin Cash in June.

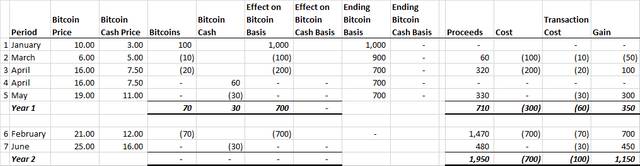

Aggressive

In year 1, Taxpayer A would recognize a total short term capital gain of $350. This gain is comprised of $100 for the sale in April of Bitcoin and $300 for the sale of Bitcoin Cash in May offset by a $50 loss from selling Bitcoin in March.

In Year 2, Taxpayer A would recognize long term capital gain of $925 on their 2018 individual income tax return. This gain is comprised of $700 from the sale of Bitcoin in February and $450 from the sale of Bitcoin Cash in June.

Recommended Reading

https://www.natlawreview.com/article/income-whatever-exchange-mine-or-fork-derived-basics-us-cryptocurrency-taxation

https://www.forbes.com/sites/tysoncross/2017/10/17/yes-the-bitcoin-hard-fork-really-is-taxable-income-heres-what-you-need-to-know/#6fe0d63c2d07

Disclaimer

Any accounting, business or tax advice contained in this communication, including attachments and enclosures, is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

Thank you for this post. It really explains the taxation very well. Greatly appreciate it.

No problem; I'm happy to help.