Case Study 46: Calculation of Offer in Compromise

Index - https://steemit.com/tax/@alhofmeister/rqgmk-tax-blog-index

Introduction

After concluding my last series on back taxes, I felt unsatisfied with the projected tax savings. As a result, I've decided to do a second series on back taxes with a more extreme example. After filing the missing tax returns & calculating the necessary penalties and interest, an offer in compromise is drafted to settle the liability. This article will cover the offer in compromise.

Problem

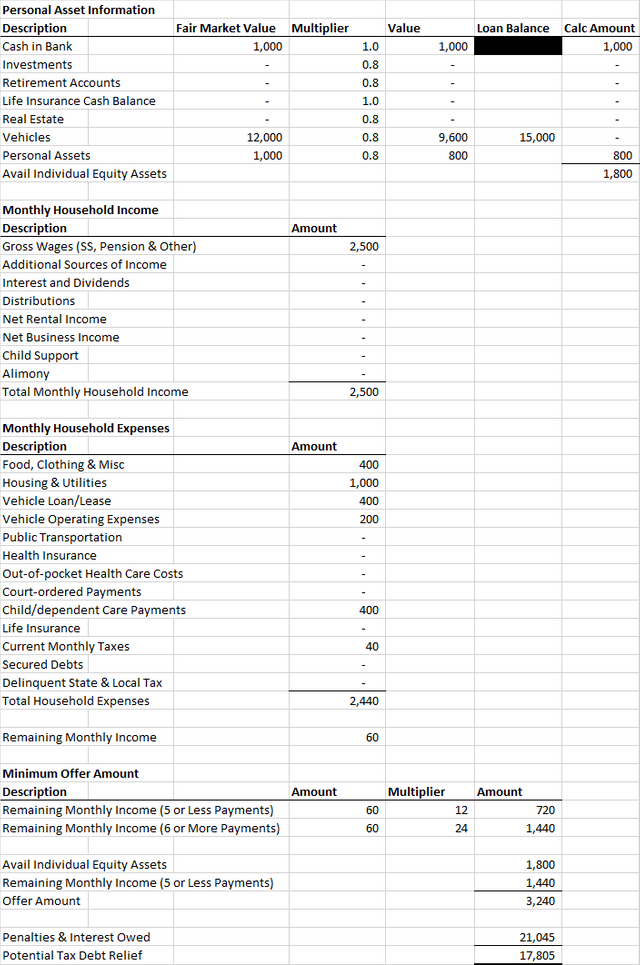

Taxpayer A did not file their tax returns for 2013, 2014, 2015, or 2016. In 2018, Taxpayer A decided to settle with the IRS before they received a notice. Note that these calculations assume that the taxpayer files on February 28, 2018. The following fact pattern describes Taxpayer A's financial situation:

- $1,000 cash in the bank;

- A car worth $12,000 with an outstanding loan of $15,000 and monthly payments of $400;

- Car insurance of $150 a month with gas expenses of $40 and repair expenses averaging $10 a month;

- Miscellaneous personal items (furniture, etc.) worth $1,000;

- A monthly salary of $2,500;

- Rent of $800 per month with $200 of utilities;

- Food, clothing, misc expenses of $400 a month;

- Daycare costs of $400 a month; and

- Average monthly state taxes (sales, income, etc.) of $40.

Calculations

References

https://steemit.com/tax/@alhofmeister/case-study-44-calculation-of-penalties-and-interest

https://steemit.com/tax/@alhofmeister/case-study-36-failure-to-file-2009

https://steemit.com/tax/@alhofmeister/case-study-37-failure-to-file-2010

https://steemit.com/tax/@alhofmeister/case-study-38-failure-to-file-2011

https://steemit.com/tax/@alhofmeister/case-study-39-failure-to-file-2012

https://steemit.com/tax/@alhofmeister/case-study-40-failure-to-file-2013

https://steemit.com/tax/@alhofmeister/case-study-41-failure-to-file-2014

https://steemit.com/tax/@alhofmeister/case-study-42-failure-to-file-2015

https://steemit.com/tax/@alhofmeister/case-study-43-failure-to-file-2016

Disclaimer

Any accounting, business or tax advice contained in this communication, including attachments and enclosures, is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

very good

Much appreciated.

Very nice work,as always

Thanks!

@OriginalWorks