Calculation of the 20% Deduction for 2018 Pass Through Entities

Index - https://steemit.com/tax/@alhofmeister/tax-blog-index

Introduction

Pass through entities include those taxed under Subchapter S (S Corps), Subchapter K (Partnerships) and disregarded entities (Sole Proprietorships). Under the new tax law, owners of these type of entities will be entitled to a 20% deduction on their qualifying business income. Below, I will explain some of the limitations and intricacies associated with the new deduction.

Calculation

A deduction is allowed to taxpayers other than a corporation under IRC 199A equal to the sum of:

- the lesser of:

a) the combined qualified business income amount of the taxpayer; or

b) an amount equal to 20% of the excess of the taxable income of the taxpayer, over the sum of any net capital gain plus the aggregate amount of qualified cooperative dividends, plus - the lesser of:

a) 20% of the aggregate amount of the qualified cooperative dividends of the taxpayer, or

b) taxable income (reduced by the net capital gain (as so defined)) of the taxpayer for the taxable year.

Qualified Business Income ("QBI") is defined under the new bill as "the sum of... 20% of the aggregate amount of qualified cooperative dividends... or... taxable income (reduced by the net capital gain (as so defined)) of the taxpayer for the year... plus 20% of the aggregate amount of the qualified REIT dividends and qualified publicly traded partnership income of the taxpayer".

The deductible amount for each trade or business is the lesser of:

- 20% of the taxpayer's qualified business income with respect to the qualified trade or business; or

- the greater of:

a) 50% of the W-2 wages with respect to the qualified trade or business; or

b) the sum of 25% of the W-2 wages with respect to the qualified trade or business, plus 2.5% of the unadjusted basis immediately after the acquisition of all qualified property.

The 50% of W-2 limitation does not apply in the instance that a taxpayer's income does not exceed the threshold amount defined in IRC 199A(e)(2) - $207,500 for single filers, $415,000 for married filing jointly. Additionally, there are other phase outs related to specific businesses which are defined below.

Specified Service Trade or Business ("SSTB")

Definition

A specified trade or business is any trade or business described in IRC 1202(e)(3)(A) - health, law, consulting, athletics, financial services, brokerage services - excluding engineering and architecture or a business which involves the performance of services that consist of investing and investment management, trading or dealing in securities (as defined in section 475(c)(2)), partnership interests, or commodities (as defined in section 475(e)(2)).

Limitations

The deductible amount for SSTBs is the qualified business income multiplied by 20% reduced by the amount phased out. The deduction available for an SSTB is reduced by the amount of QBI over $157,500 (up to 50,000) for single filers or $315,000 (up to $100,00) for married filing jointly filers.

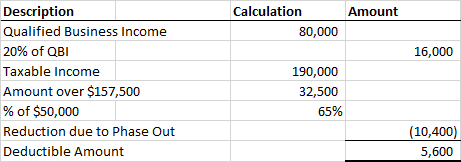

Example

Taxpayer A is single and made $190,000 in total taxable income made up partly of $80,000 from operating their financial service sole proprietorship. Taxpayer A's deduction would be calculated as follows:

All Other Businesses

Definition

As the name implies, all other businesses are any type of business that doesn't fall into the definition of a SSTB.

Limitations

The limitations for all other businesses is similar to the limitations for SSTBs, but excludes the phase out prescribed in IRC 199A(d)(3).

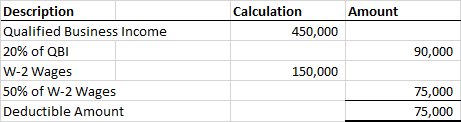

Example

Taxpayer B is single with taxable income of $600,000 and QBI of $450,000 for his sole proprietorship which sells widgets. Taxpayer B pays their employees W-2 wages totaling $150,000. Taxpayer B's deduction would be calculated as follows:

References

https://www.congress.gov/bill/115th-congress/house-bill/1/text

https://www.law.cornell.edu/uscode/text/26/475

https://www.forbes.com/sites/anthonynitti/2018/01/04/the-new-qualified-business-income-deduction-varies-based-on-your-business-type-or-does-it/#3db0fb042076

Disclaimer

Any accounting, business or tax advice contained in this communication, including attachments and enclosures, is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

@OriginalWorks