Simulation Results

We do several simulations in our artificial stock market in order to have some

understanding points of what we discover in previous work on statistical properties of

Indonesia stock market (Situngkir & Surya, 2003a, Hariadi & Surya, 2003). A pattern we

want to analyze is the fact of volatility clustering, in which large changes tend to follow

large changes, and small changes tend to follow small changes.

The volatility clustering has been widely known as an important and interesting

property of the financial time-series data. The cause of this property is certainly the

interaction of between the heterogeneous agents; in our case: the fundamentalists, the

chartists, and the noise traders. The decisions of any strategies will be different in the

sense of expectations about future prices. Other important feature of our simulation is

the boundedness of each agents one another on their final decisions; as noted above we

apply the influence strength of any decisions (buy, hold, or sell) as the climate of the

market. Henceforth, in certain time, a climate to sell, hold, or buy among agents becomes

the trigger for the volatility clustering.

In advance, the volatility clustering has understood also impacts to the

distribution of the financial data. The distribution of the price fluctuations (return) is less

Gaussian with fat tails (leptokurtic) fitted with the truncated Levy distribution (Mantegna.

& Stanley, 2000:60-67, Surya, et.al., 2004) i.e.:

⎩

⎨

⎧ = 0

( ) ( ) ,0 L x

p x

ξ α …(6)

where ξ denotes the normalizing constant, l the truncation parameter, and Lα ,0 the

Levy distribution (whose coefficient α and β = 0 ). This is the form of distribution with

finite variance and considering the Central Limit Theorem, which states that the sum of

independent samples from any distribution with finite mean and variance converges to

the Gaussian distribution as the sample size goes to infinity.

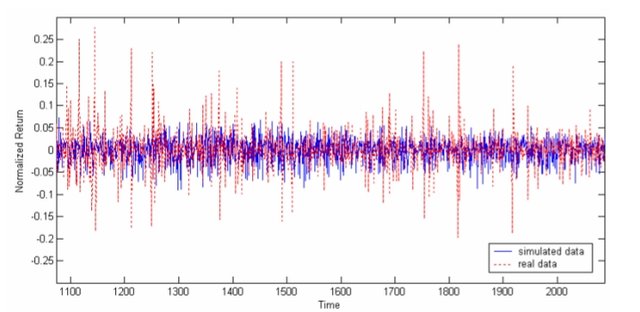

Figure 3 shows the distribution of the simulated return compared with the real

data. The distribution of the return is leptokurtic, with fatter tail than Gaussian

distribution

.