Option Volatility and Pricing (Natenburg) - Chapter 7 - Risk Measurement I - The Gamma and The Theta

Chapter 7 - Risk Management I

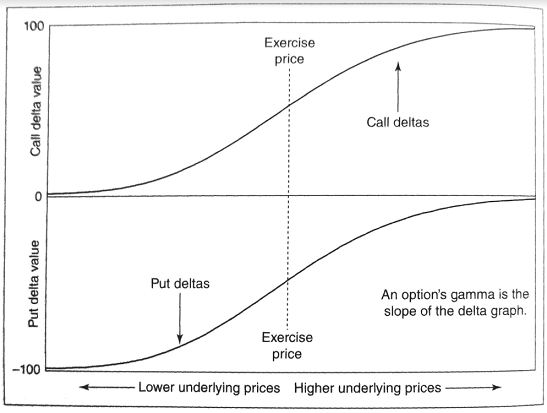

The Gamma

The Gamma is defined as the change in delta over the change in the underlying price. This is a clear definition of a derivative. Another way of saying it is how much the Delta changes over a 1 point change. Natenburg gives a great graph that I can not replicate to describe it.

I'm pretty sure that later on in the book that the Delta will be found using implied volatility, but we haven't gotten there yet. Recall that call option deltas are positive and put option deltas are negative. Also, notice the slope at any point on this graph above, always positive, so this means Gamma is always positive.

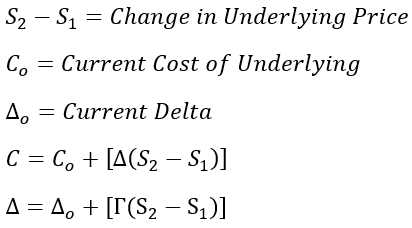

For example, we have a put option with a delta of -40 and a gamma of 2. If the underlying price rises by 1, then the delta becomes -38 (38% chance of success). If the underlying price falls by 2, then we have -40 - 2*2 which gives a new delta of -44%. Remember that the probability of success is increasing when the price drops.

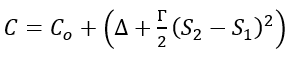

Since the derivative tells the slope it also tells the curvature of the graph at that point and gamma is no longer accurate and has to be recalculated once the price moves too much. We can derive equations for this as well.

Since Delta changes when the price of the underlying changes it is best to use an average delta. Thus we take an average of delta when it is at both S1 and S2 (underlying prices).

Using the average Delta and the first equation we should have a new underlying price of

This is what we will use to calculate option price over underlying price changes.

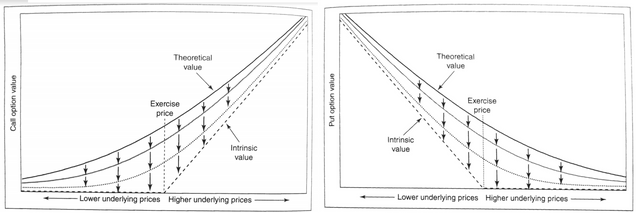

The Theta

This variable represents time decay. The farther away from expiration the more an option is worth because the probability of success or failure of the option is still not determined. As time reaches expiration the option value, which is the intrinsic value + time value, reaches its time value becomes zero and its worth is equal to the intrinsic value. There will be more on calculating this value in CH 9. Here are some graphs that show time value + intrinsic value.

Call vs. Put Option Values

We can have a negative time value, although it does not happen often. This is when the theoretical value slides under the intrinsic value. It usually happens when the value is well over the exercise price.

Source:

Natenberg, Sheldon. Option Volatility and Pricing Advanced Trading Strategies and Techniques. 2nd ed., McGraw-Hill Education, 2015.

Have you ever tried day trading because I wanna do that

Yeah. A lot over the last few years, but it's really hard and you have to be patient. I am studying this for buku $$$.

Buku?

It's another word for "a lot of". Have you ever seen Full Metal Jacket?

No I have not

What’s that

An awesome movie that I probably shouldn't even recommend. Haha.

I will watch it sometime soon when I have time because at this school they give no homework and we don’t use computers all the time

Right now I have my computer hooked up to the TV so I can watch Netflix and work all day. Haha.

Sounds fun, you should try working online or creating a store. Remember steem has jobs you can do

You have a good point, but I think I am hardly qualified to apply to them. Guess I should anyways for fun. Haha. Programming is all the same... almost.