Option Volatility and Pricing (Natenburg) - Chapter 7 - Risk Measurement I - The Delta

Chapter 7 - Risk Measurement I - 1

This section helps us determine whether or not an option is worth the risk to trade. This is where professional traders have the edge. Most basic traders, like myself for the last 2 years, just look at prices and only worry about the price of 1 stock going in the direction they want it to... Not Safe! Given all of the proper data, which the general population does not have because the software is expensive to build, we can make good trades. Natenburg begins by summarizing these risks.

- A change in interest rate affects the price in two possible ways. It can change the forward price and the present value of the option. As interest rises call option prices become greater and put options prices fall. Here is a table of changing market conditions:

- Whenever possible a trader should avoid a short stock position* because there is an infinite possible loss due to the fact that a price can rise indefinitely (even though we know there is a limit).

- Stock-Type Settlements (USA) are affected by changing interest rates, but Futures-Type Settlements (European) are not affected. Here is a more detailed table with changing interest rates:

The Delta

The delta is a measure of the option's risk with respect to the direction of movement. A positive delta indicates a desire for the price of the underlying to increase. A negative delta indicates a desire for the price of the underlying to decrease.

Rate of Change

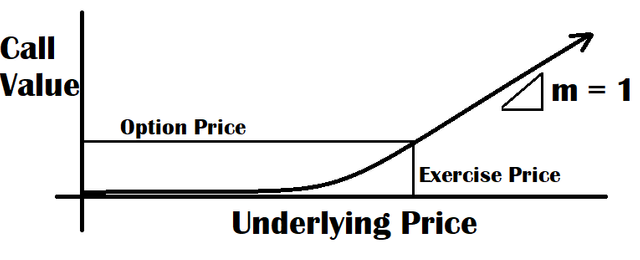

Graph of Theoretical Value of a Call

For example, if the delta of a call option is .70, then the value of the option will rise or fall at 70% the change in price of the underlying. So, we can expect, if there is a 1.00 change, the value of the option will change .70 in the direction of the change. Puts are the same, but the delta is negative. For an underlying contract, the delta is always 1 because it measures the change of the option value, not the underlying price. Traders do not use the decimal value, they use the percentage value, so instead of saying .70 we will say 70 for the delta. How do we determine this delta value?

Hedge Ratio

Remember that we discussed, in Ch 5, a risk-less and neutral hedge in option positions. When a trader who is trying to capture the rhotetical balue of an option must start and end with a neutral (0) hedge.

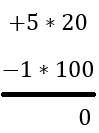

Example 1

If we have a delta of 20 and buy 5 calls, then we want to sell 1 stock of the underlying. If we want to hedge a position so that the delta maintains neutrality we can set up the following equation:

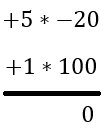

Example 2

If we have a delta of -20 and buy 5 puts, then we want to buy 1 stock of the underlying.

Theoretical or Equivalent Underlying Position

It follows that each 100 deltas in an option position is equivalent to 1 of the underlying. Trading on strictly a delta position is not a good idea because the price of an option depends on many factors. If a trader holds a delta position of 500 (say he owns 10 contracts with a delta of 50), then he will have a similar position if he sells 20 puts with a delta of -25. If the trader keeps the delta of +500 and the stock rises 2, then he should gain 500% or 10. If the stock falls 1.25, then he should lose 6.25.

Probability

A call with a delta of 50 or a put with a delta of -50 has a 50% chance of ending in the money. As this delta moves closer to 100 or -100 the call or put is more likely to be in the money. Option strategies depend on whether the outcome lands in the money and by how much. This needs to be considered because if you win 9 times, but lose all of your winnings on the 10th try, what is the point? We want trades to be small and low-risk.

Cool! Omg I want to learn option trading but it is so hard for me to grasp the concept! Cool u had been trading for 2 yrs! Upvoted to support

Posted using Partiko iOS

It would be easier to teach you in person. Haha. There are many more examples I could give, but they take so long to type up. For now, I will just post the main concepts.