Option Volatility and Pricing (Natenburg) - Chapter 2 - Forward Pricing

Chapter 2 - Forward Pricing

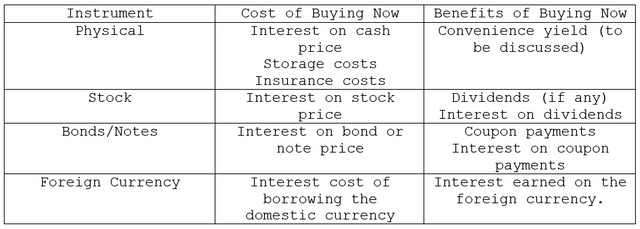

Physical Commodities

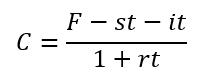

- Given the following variables:

F = forward price

C = commodity price

t = time to maturity of the forward contract

r = interest rate

s = annual storage costs per commodity unit

i = annual insurance cost per commodity

- A normal or contago commodity market is one in which long-term futures contracts are traded at a premium to short-term contracts.

- If the cash price of a commodity is greater than a futures price, the marked is backward or in backwardation.

- Convenience Yield - the benefit of being able to obtain a commodity right now at cash price.

Stock

- We receive dividends that the stock pays over the life of the forward contract together with the interest earned on the dividend payments.

S = stock price

t = time to maturity

r = interest rate over the lifetime of the forward contract

= each dividend payment expected prior to maturity of the forward contract.

= each dividend payment expected prior to maturity of the forward contract.

= time remaining to maturity after each dividend payment.

= time remaining to maturity after each dividend payment.

= the applicable interest rate (the forward rate) from each dividend payment to maturity of the forward contract.

= the applicable interest rate (the forward rate) from each dividend payment to maturity of the forward contract.

- For simplicity, they aggregate all dividends D expected over the life of the forward contract and ignore interest on dividends.

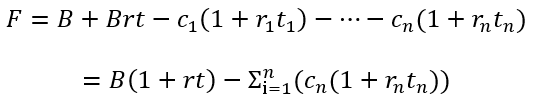

Bonds and Notes

- Treating coupons like dividends, we can evaluate bond and note forward contracts, similar to stock forwards. We must pay the bond price with the interest cost. In return, we will receive fixed coupon payments on which we can earn interest.

B = bond price

t = time to maturity of the forward contract

r = interest rate over the life of the forward contract

= each coupon expected prior to maturity of the forward contract.

= each coupon expected prior to maturity of the forward contract.

= time remaining to maturity after each coupon payment.

= time remaining to maturity after each coupon payment.

= applicable interest rate from each coupon payment to maturity of the contract.

= applicable interest rate from each coupon payment to maturity of the contract.

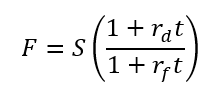

Foreign Currencies

- With foreign currency forward contracts, we must deal with two different rates - the domestic interest rate and the foreign interest rate. Spot exchange rate

, where

, where  is the cost of one foreign unit in terms of domestic currency and

is the cost of one foreign unit in terms of domestic currency and  is one foreign currency unit.

is one foreign currency unit.

Stock and Futures Options

- A trader in exchange-traded options on crude oil is really trading options on crude-oil futures.

- For both stock and futures options, the value of the option will depend on the forward price for the underlying contract.

Arbitrage

- Arbitrage - a trade that results in a risk-less profit. The buying and selling of the same or very closely related instruments in a different markets to profit from an apparent mispricing.

- Carry trade - a trader attempts to profit by borrowing a low-interest rate domestic currency and using this to purchase a high interest rate foreign currency.

- Cash and Carry Arbitrage - involves buying in the cash market, selling in the futures market, and carrying the position to maturity.

- If money has been borrowed or lent at a fixed interest rate, then there is no interest-rate risk. Most traders borrow at a variable interest rate.

Dividends

- A trader will usually have to estimate the amount of the dividend and the date on which the dividend will be paid.

- Declared Date - the date on which a company announces both the amount of the dividend and the date on which the dividend will be paid.

- Record Date - The date on which the stock must be owned in order to receive the dividend.

- Ex-Dividend Date - The first day on which a stock is trading without the rights to the dividend.

- Payable Date - The date on which the dividend will be paid to qualifying shareholders (those owning shares on the record date).

Short Sales

- Sell Stock Short - sell stock that he does not already own. The trader hopes to buy back the stock at a later date for a lower price.

- Short-Stock Squeeze - when it is difficult or impossible to borrow stock.

- Short-Stock Rebate - The rate that the trader receives on the short sale of stock.

is the borrowing cost found by the long rate minus the short rate.

is the borrowing cost found by the long rate minus the short rate.

A trader does not need to borrow the option in order to sell it. For this reason, we always apply the ordinary long rate to the cash flow resulting from either the purchase or sale of an option.

Source:

Natenberg, Sheldon. Option Volatility and Pricing Advanced Trading Strategies and Techniques. 2nd ed., McGraw-Hill Education, 2015.