Advanced MONEY MANAGEMENT Strategies

Advanced Money Management Techniques

Whereas risk management comprises the handling and the impacts of position size on the account growth and determines the size and the significance of possible drawdowns and losing streaks, money management describes the methods to establish a repeatable and structured approach to position sizing and the actual size of positions under different, but specific, conditions.

Risk management is about finding the right balance between risking too much and risking too little; whereas risking too much results in large drawdowns and, potentially, large equity growth and risking too little means that drawdowns can be controlled better, but equity growth will be much slower.

Risk management, or risk control, means that a trader has to be aware of the opposing forces of position size. Furthermore, risk management also encompasses establishing guidelines how to handle certain drawdowns, when to cut back on risk and how to the own performance metrics. Risk management, therefore, sets the premises and the guidelines in which the money management approach has to be chosen.

Money management = Money management describes the actual method of determining the position size under certain, but specific, conditions. Money management is the setscrew that a trader can adjust in order to meet his risk management goals and to control the level of risk, while optimizing equity growth.

A trader can implement a variety of different money management techniques and we will introduce the most popular ones here, in addition to the basic models of fixed percentage and fixed equity:

Averaging up

Averaging up is also known as ‘adding to a winning position’ or scaling into a trade which means that once a trade moves into profits, the trader adds more contracts to the existing position.

Pros:

Potential losing trades will be relatively smaller because the initial position is not as big when following the averaging up approach.

Especially for trend following methods, the averaging up approach could be beneficial because it allows a trader to add more and more size once the trend reinforces itself.

Cons:

Finding a reasonable and an optimal price level to add to a position can pose challenges. Furthermore, once price turns, losers can offset winners fairly quickly. To counteract this effect, traders use larger positions on earlier orders and then reduce their size when they start averaging up, which partially offsets the pro-argument.

Cost Averaging

This method is often called ‘adding to losing positions’ and it is very controversially discussed among traders. It is the opposite of averaging up because once your trade moves against you, you would open new orders to increase your position size.

Pros:

Losses can potentially be reduced and the point of break-even could be reached faster once a trade which has moved against you turns around.

Cons:

This method is often abused, especially by amateur traders, who are in a losing position and are emotionally attached to it (see Disposition effect in the Psychology section). Such traders arbitrarily open new orders on the way down in the hope, and by lacking a sound trading plan and principles, that price eventually has to turn around. The improper use of cost averaging is a common cause for significant losses among amateur traders.

The cost averaging method is not recommended for amateur traders or for traders who lack discipline and are emotionally about their trading.

Martingale

The Martingale position sizing approach is as heated discussed as the previously mentioned cost averaging method.

Basically, after a losing trade,the trader would double his position size to, potentially, recover losses immediately with the first winning trade, which offsets all previous losses.

Pros:

All previous losses can be potentially recovered with only one winning trade.

Cons:

The point where doubling-up means risking the whole account comes inevitably. Over the long-term, all traders will experience a losing streak and just one extended losing is often enough to wipe out a trading account.

If traders tend to revenge-trade and impulsively enter trades after losses, the Martingale technique poses great challenges and under such circumstances, can even faster lead to a complete account loss.

Starting with only 1% risk per trade, a trader loses his whole trading account after the 8th losing trade in a row.

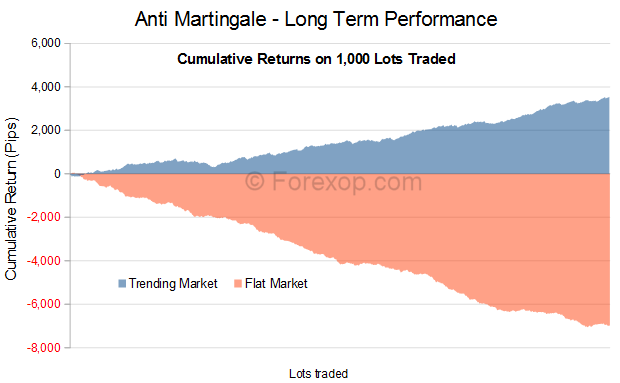

Anti-Martingale

The anti-Martingale eliminates the risks of the pure Martingale method. In contrast to the Martingale system, when a trader loses, he does not double-up but sticks to his position sizing method. Therefore, a losing streak cannot wipe out the trader as fast. On the other hand, when a trader has a winning streak, he doubles-up and risk twice as much on the next trade. The thinking behind this approach is that after a winning trade, you are trading with ‘free’ money.

For example, a trader realizes a profit of $200 on his trade, where he risked 1% on a $10,000 account; now his new account size is $10,200. On his next trade, he can risk $200 which is 1.96% of $10,200. If his trade is another winner with a reward:risk ratio of 2, he makes $400 and his new account size is now $10,600. On his next trade, he can risk the $600 which are now 5.7% of $10,600.

Antimartingale money management strategies are also possible with Short positions

Pros:

Traders can potentially make more money during winning streaks and do not fall as easily below their original starting account balance.

Cons:

Just one loss can wipe out all the previous gains. For this reason, traders should not just double-up their position size, but use a smaller factor than 2 to determine the position size after a winner. This way, they will still be left with a profit after realizing a losing trade.

Account swings with the anti-martingale technique can be significant because losses after winning streaks can be very large. If a trader cannot deal with such losses, the anti-Martinga method could lead to further problems. It is advisable that a trader determines a certain level when he does not double his position size anymore, but goes back to his original approach, securing his gains.

Fixed ratio

The fixed ratio approach is based on the profit factor of a trader. Therefore, a trader has to determine the amount of profit that allows him to increase his position (also known as ‘Delta’).

For example, a trader can start out with trading only one contract and he chooses his Delta to be $2,000. Every time the trader realizes his profit Delta of $2,000 he can increase his position size by 1 contract.

Pros:

Only when the trader is actually making profits, he can increase his position size.

By choosing the Delta, the trader can control the growth of his equity. A higher Delta means that a trader increases his positions slower, whereas a lower Delta means that a trader increases position size faster after making profits.

Cons:

The Delta value is very subjective and setting the Delta is more a personal preference, rather than an exact science.

Whereas a high Delta decreases position size with a growing account, a low Delta increases the position account when moving from one profit boundary to the next. The differences can be significant.

Kelly’s Criterion

The goal of the Kelly Criterion is to maximize the compounded return that can be achieved by reinvesting profits and the Kelly Criterion uses the winrate and the lossrate to determine the optimal position size. The formula looks as follows:

Position size = Winrat – ( 1- Winrate / RRR)

However, the suggested position size for the Kelly Criterion often undererstimate the impact of losses and losing streaks. Here are two examples that illustrate the point:

Example 1)

Position size = 55% – (1 – 55% / 1.5)= 25%

Example 2)

Position size = 60% – ( 1- 60% / 1) = 20%

As you can see, the suggested position sizes of the Kelly Criterion are very high and much higher than should be considered for a sound risk management. To counteract this effect, the common approach is to use a fraction of the Kelly Criterion. For example, 1/10 of the Kelly Criterion would lead to 2.5% and 2% position sizes in the example above.

Pros:

Maximizes the growth rate

Provides a mathematical framework for a structured approach

Cons:

A full Kelly Criterion can lead to significant drawdowns very fast. Using a fraction of the fully Kelly Criterion should be considered.

Conclutions

There are several strategies traders can use. Most used one is the fixed ratio method, usually a 2% risk of the total account per trade. Depending on risk aversion and the trader's profile there are options that will bring higher yields at the end of the year.

However it is important to know all the possibilities and know the pros and cons of each method.

Deep understanding about the maths of money management is a must in order to achieve great returns over the long run.

Today I want to give a big S/O to @cgbartow and all the members in the community growth project

Steem is about the community and creating good networking by curating quality content and adding value to your followers.

Invest in those whom invest in you

Invest in yourself or no one else will.

Excellent teaching. Thank you!

Glad you enjoy it. Thanks for your daily support!