The Future of Cryptocurrency: Part 2

In the ongoing week of #steemcryptochallenge, I have already published the Part-1: The Future of Cryptocurrency.

Today I will detail Part 2 and this will cover CBDC & Regulatory Framework, and how the implementation of both can further strengthen the crypto ecosystem, and how it will help cryptos to establish its foothold in the legacy financial network.

CBDC by Central Banks with permissioned Blockchain

Before going into CBDC, let's first understand the three important characteristics of money:

- Medium Exchange

- Store of Value

- Unit of Account

If we compare fiat with crypto, then both are good as "medium of exchange". Both are mobile(however crypto is relatively more mobile), both are divisible, hence suitable as a medium of exchange.

Both are more or less good as "store of value", although crypto sounds better because it follows a deflationary curve whereas fiat follows an inflationary curve. However fiat is so liquid in the legacy financial ecosystem that it easily offsets its inflation, and everyone prefers to accept it as payment.

In the Unit of Account, during the exchange of goods and services, one should be able to measure it with a common reference. That is what we call "Unit of Account". For that to happen, the price of the money or an asset that we are choosing as a reference should be stable enough to make it easy for the exchange of goods and services.

Fiat has the characteristics of "Unit of Account", whereas the excessive volatility of cryptos does not serve the characteristics of the Unit of account. To make it serve as a "Unit of Account", it needs to be collateralized, for example, stable coins.

By cryptos, we generally mean Blockchain as the underlying protocol, which is decentralized by principles. However, Blockchain can be classified into permissionless and permissioned Blockchain. The potential of permissionless Blockchain is huge as it is open for all. In contrast, Permissioned Blockchain is controlled by small groups/individuals to cater to the specific requirement limited to a particular institution, group, or a Govt.

I would not say a permissioned Blockchain a centralized thing, rather I would say it is relatively less decentralized than a permissionless Blockchain. Because it is still decentralized within that group/institution. And it has its genuine use-cases. One of them is CBDC.

CBDC- Central Bank Digital Currency

In the existing financial system, we have fiat(physical form, paper currency) as well as digital fiat. The fiat money is guaranteed by the Govt whereas the economic policy decision is governed by Central Banks.

The digital fiat is used as a digital equivalent of fiat money, highly mobile to transfer from one peer to the other, routed through a bank (a centralized entity or an intermediary). So even though it is digital it is rooted in the physical fiat.

In the legacy financial system, every financial operation happens through an intermediary and the intermediaries are the banks(both Private and PSU Banks).

Since there is an intermediary, the cost incurred is high on the end-user, time-consuming as well, it is also exposed to corruption, bribery, etc. Free & easy banking access for all can not be achieved with such a financial landscape.

CBDC is a digital form of fiat money(not digital fiat) regulated by the central banks. It is still with state control, sovereign rights, but with proof-of-concept protocol.

Objectives of CBDC:-

- Financial inclusion with easy access to Banking

- Speed of Transaction

- Cost-Effective Transaction

- Transparency & Accountability

In the implementation of CBDC, it will be run by the central bank, Govt, and authorized entities. It will be a distributed ledger, however, permissioned. All the records will be protected with cryptographic signatures.

In the existing economic landscape, the central bank is a bank of banks(private and PSU). It is not a universal bank for all. With the CBDC, the central bank can be a universal bank for all citizens/individuals. It may so happen that the liquidity could flow out from the private, PSU banks to CBDC, but every reset goes through such temporary pain. Here it will serve the largest objective of a better financial system.

CBDC can dramatically revolutionalize the present economic landscape with its use in identification, accessibility & yield-bearing capacity.

CBDC, with a universal account for all, will become accessible for all citizens without the hassle of the Banks, the individuals will have better control, right to possess, transfer to another peer, fully secured, no worries of counterfeit, etc.

CBDC will also be helpful in tracking illegal activities because it is traceable, unlike physical cash. Where the money is flowing can be easily tracked with the distributed ledger. Further Govt can also be able to collect more tax, tax evasion will be difficult, more transparent economy and a better beaurocratic system can be established.

When the CBDC will allow Universal Account for all in the central Banks, it will drive more competition and better services from the public and Private banks which in most of the developing countries is below average in serving the general citizens. Ultimately it will be the public who will be benefitted from CBDC.

With CBDC the deposit guarantee schemes, deposit insurance will get redundant, and for the good. Most importantly, the inspector raj in the taxation(in countries like India) will come to an end. That will pave the way for monetary reforms & create an avenue to include those who are outside the purview of this present economic landscape.

.png)

Example,

In India, the most legitimate Identity Proof is ADHAAR issued by UIDAI, Govt. of India. The RBI(Central Bank of India) should implement CBDC and offers Universal Basic Account(UBA) for all. And that UBA should be tied with ADHAAR, now that becomes easy banking access for all.

That also solves the anonymity and possible abuse with money laundering, terror financing, etc.

In rural areas of India, ADHAAR is not a problem today but Banking is still a high barrier for many. Moreover, the only way for Banking access is either a Private or Public Bank with a long list of documents, long-chain to stand in a queue to open a bank account. Not to forget the middle-man, lobby, brokers who take extra money(illegally) to expedite this process.

CBDC will ensure banking access for all, bypassing the private/public Banks. I am not against Banks, but I want this as optional, not mandatory. That will also bring down the cost incurred by the end-user. With this, the banking monopoly and other associated risks like bankruptcy will end and the new landscape with CBDC will become more competitive, transparent, easy for the common man.

Pros & Cons of CBDC

Pros

CBDC will be most beneficial for the end-users, general citizens. For public and private banks it could be painful in the early days of transition as liquidity could flow out from banks to CBDC, but in time it will reach equilibrium again, should the banks end the monopoly and offer competitive services for the general citizens.

It will be most secured than the existing system.

It will bring the much-needed reforms on the socio-economic front in developing countries like India by creating an inclusive policy for all, particularly the rural areas.

The banking access will be easy, fast & cost-effective

The legitimate owner of the asset will be unaffected by the bankruptcy of a Bank.

The state can get rid of counterfeit notes with CBDC.

Cons

Crypto literacy is still needed. So more awareness drive and literacy campaign needed from the Govt with a public-private partnership.

Needs better cybersecurity infrastructure to deal with hacking, fraud.

Friendly Regulatory Framework for Crypto Trade & Services

Even though cryptos are popular today, having innumerable benefits such as immutability, transparent public ledger, cost-effectiveness, faster processing time as compared to the traditional international transfers, etc the enterprises are reluctant to use cryptos because they fear they could be unjustly sanctioned by the authorities.

Therefore a friendly regulatory framework is necessary.

The Blockchain is popularly known as a disruptive technology. But it may not be a currency with sovereign rights, we don't even know "if the concept of state and sovereign rights will become obsolete". Therefore it is prudent to find a way to bridge the gap between a state-controlled currency(or CBDC) and a permissionless currency(cryptos). A friendly regulatory tailor can bridge this gap and allow the value to flow from one to the other and vice versa.

That will create business opportunities for all, a win-win situation, an ideal global market ecosystem.

By friendly regulatory framework means it should not restrict the inherent characteristics of cryptos & their benefits, and on the other side it should be able to check its use in money laundering or illicit activities, it should be able to make enterprises and other relevant players accountable in case of any inconsistencies.

Conclusion

The future of cryptocurrency in the legacy financial system is poised for a friendly regulatory framework and CBDC. With each passing day, we are inching close to this breakthrough.

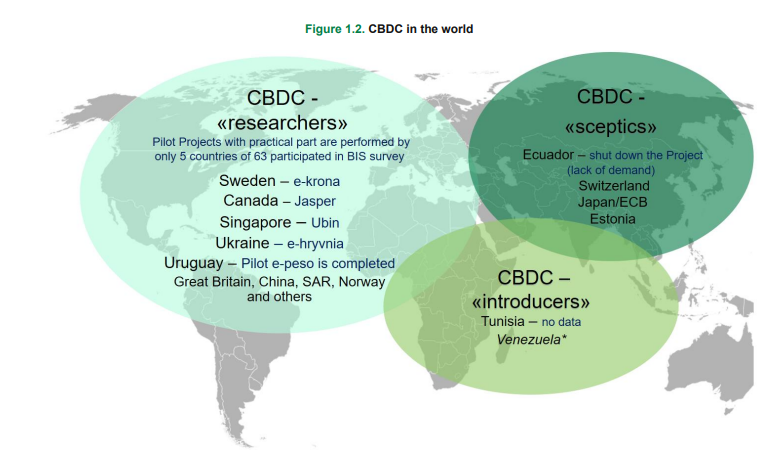

In the context of CBDC, pilot projects, experimental studies are going on in various countries-- practical steps taken by Tunisia, Research & Pilot projects by Ukraine, UK, Singapore, Canada, Uruguay, etc.

It is true that a considerable amount of investment might be needed for the retail infrastructure in implementing CBDC, but that is all part of the reset whenever we will be doing that, it will have its dividend in the long run, and most importantly, it will create a better economic landscape for the common man.

With a friendly regulatory framework & CBDC, I foresee an exorbitant growth in cryptocurrencies, however as we mature we will be less speculative and will be driven by fundamental value. It is good that the noise, speculation will settle down and we will have more blue sky and clear water to sail through.

Thank you.

Cc:-

@steemitblog

@steemcurator01

@steemcurator02

You made a really good point. Cryptocurrency checks all the boxes when it comes to it's use as medium of exchange and it is more mobile than fiat. I think there are two things that make it more mobile.

This is my opinion though.

A regulatory framework is crucial so that the government can manage the benefits and challenges of crypto. It will also provide some measure of security.

#onepercent #nigeria

Thank you.

Congratulations you are one of the winners of the Steem Crypto Challenge Month...

Thank you for taking part

The Steemit Team

Thank you so much.

Steem on.

A good point with decent words. The cryptocurrencies are made for gloable use, but the reality is the usage is so broken due to national regulations.

In a technophilia society, the government support all new technologies like crypto. In Switzerland, their regulations are favorable for cryptocurrencies. They have a separate cluster of blockchain enthusiastic companies “Crypto Valley" just like Silicon Valley.

Malta is another country that maintains a "friendly regulatory framework" as you said.

Even though very few countries have these kinds of friendly regulatory frameworks most of the countries are restricted or not supported for ICOs. The opportunities of accessing crypto are not equal so that the main intention of global access demote.

#affable #srilanka #twopercent

It's just a matter of time. If any of the G8 countries implement CBDC, it will spread out to other G8 nations and also the developing countries. As a result, it will induce fundamental value and drive exponential growth in the crypto industry, even if it is a permissioned Blockchain.

Thank you.

#affable

I think G8 members are already researching about CBDC specially bank of Japan.

#affable