Gods of the Valley — Part One: Amazon — The Company that Consumes the World

Today Amazon feels unstoppable.

The company Bezos built to sell books online is now arguably the most dominant and diversified company on earth, and the odds on favorite to crack the $1T market cap first.

This seems to be the consensus, at least among technologists. But the majority are often very wrong, so let’s dive deeper.

Amazon’s current empire

Unlike most of the Fortune 500, Amazon is very diverse. It isn’t one or two products that drive their success, it is an army. Amazon’s business is made up of five primary divisions: Amazon.com, AWS, Alexa, Whole Foods Market, and Amazon Prime.

Each of Amazon’s 5 primary divisions would, on its own, be an impressive business. Combined they create the world’s largest flywheel.

To better understand the behemoth, let’s look at and analyze each of Amazon’s divisions.

1. Amazon Marketplace: the #1 ecommerce marketplace

Amazon is the most monopolistic and well positioned marketplace the Western world has ever seen. Last year they did $136B in revenue with double digit growth every year.

And every year Amazon seems to be expanding their reach and market share. To date Amazon has 10 marketplaces across the globe, from the obvious Europe and North America; to Japan, China, and India; and are in the process of rolling out in Australia.

The ecommerce business is booming, powered by great logistics and 3rd party sellers. Amazon is quite literally becoming the defacto online store.

2017 estimates show a staggering 44% of US ecommerce occurred on Amazon.com.

And Amazon has been growing at least 13% YoY (year-over-year) for each of the last 5 years.

Source: BI Intelligence

And it gets better, the growth is diversified.

In 2016, 35.5% of Amazon’s ecommerce revenue was international, that’s up from 34% in 2015.

All of this contributes to Amazon’s stock flying high.

But there is another layer to unpack — Amazon Basics. As an ex-Amazon seller, Amazon Basics is an ugly word. It boils down to Amazon analyzing 3rd party seller data and copying the best performing products.

I have seen this happen to dozens of products and numerous friends. Amazon ONLY cares about Amazon and serving customers. The dirty tactics they take with sellers is quite troubling, and signals their future intentions. Ultimately Amazon wants to replace all 3rd party sellers/products with Amazon Basics versions. Amazon wants to (and will) own the customer, and every ounce of margin that comes with it.

This has implications both for buyers and sellers. For sellers the issues are obvious. Yet Amazon is a bit like eating fast food, tasty in the short term and terrible in the long run. Brands cannot help but want access to their hundreds of millions of customers, and thus sacrifice their future for short term success. For buyers the problem is equally bad.

Marketplaces die when the creator becomes the competitor.

As Amazon begin to limit options and over-promote their own products (which they already do in terms of which products get displayed), their pricing power increases. This could theoretically lead to increased (monopolistic) pricing and customer harm.

2. AWS: the #1 web services company

While the ecommerce business is incredibly powerful, AWS is arguably even better. (NOTE: I think Amazon should spinout AWS before regulators start anti-trust actions)

Amazon built AWS for their marketplace. They needed the ability to host images and information for Amazon.com and Bezos being Bezos, built the product in a modular fashion.

As AWS grew, Amazon constantly cut prices to crush competition, making AWS the easy choice.

“Your margin is my opportunity.” — Jeff Bezos

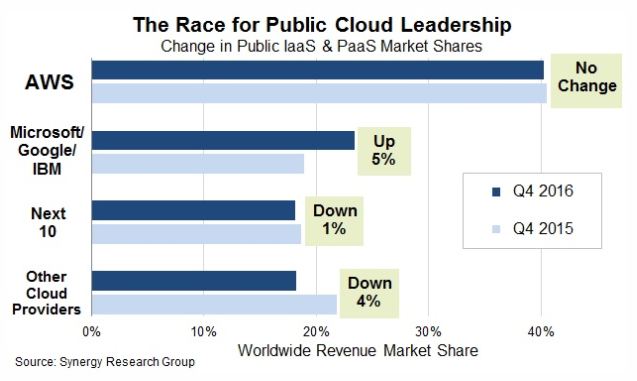

Today ~42% of the web is powered by AWS. That is more than double Microsoft, Google, and IBM (combined).

Yet given the easy-to-use system and affordable pricing, it makes sense.

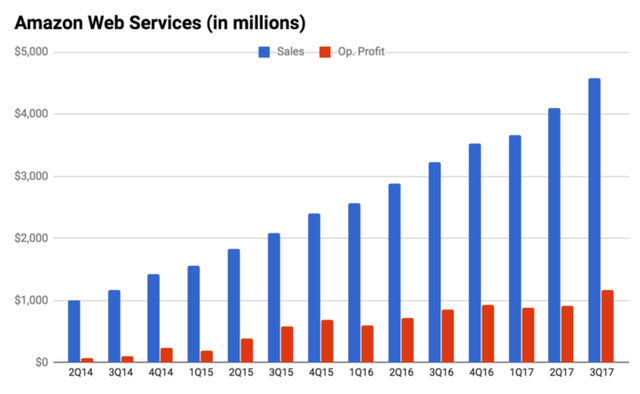

And growth isn’t slowing down, quite the opposite actually. AWS accounts for 10% of Amazon’s overall revenue, with $4.6B in Q3 of 2017 (up 42% over last year) and $1.2B in profit (up 36% over last year).

Source: GeekWire

Amazon owns the infrastructure the majority of the internet is built on.

3. Alexa: the #1 voice assistant (hardware & software)

Amazon’s many-headed monster got a powerful new addition in 2014.

For those not reading between the lines, Amazon’s ambition is to own EVERYTHING. Regardless of the nature of product or purchase, Amazon eventually wants to offer it.

Alexa is the next iteration of this. Suddenly with the explosion of Alexa powered devices, Amazon is sneaking a spy directly into your home.

This has NOTHING to do with Echo sales!!

Hint: how do you buy things?

Alexa is designed to replace everything. The goal of the product is seamlessly purchasing everything. One click checkout isn’t enough anymore.

“Hey Alexa, we’re out of toothpaste, toilet paper, and tampons.”

The beauty of Alexa (for Amazon) is selection. While customers that shop on Amazon.com currently have access to a wide variety of brands, ultimately Alexa defeats this. Eventually, every single product consumers ask Alexa for will be Amazon Basics (obviously the Alexa default). Once the trap of choice is removed (I don’t care what brand of toilet paper…), customers are more inclined to buy — meaning any basic necessities will be provided by Amazon.

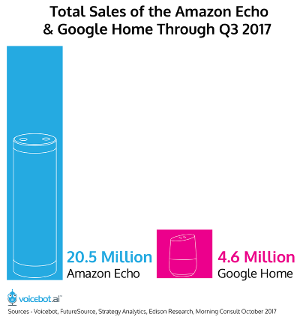

Source: Voicebot.ai

While the nifty voice controls are nice, this is Amazon’s true goal. And it is working wonderfully. According to Amazon, they sold 20M+ Echo units as of 3rd quarter last year. I cannot even imagine how many more were sold for the holidays…

If only Amazon offered groceries…

4. Whole Foods: the 10th largest grocer

Oh wait, Amazon bought Whole Foods in 2017 for about $13B. Now things get interesting. For a complete 360 breakdown on the implications of the Whole Foods acquisition, see this article.

To summarize, Amazon bought a fully functional, balanced network of supply and demand.

Amazon failed numerous times with groceries because of the challenge of spoilage. Food needs to move fast. The Whole Foods acquisition allows Amazon to leverage existing demand and largely decrease supply risk while offering up edible options to online customers. Worst case scenario, some ham and cheese don’t sell online so they slash prices in stores to liquidate inventory.

And the Alexa connection makes this even more interesting. As consumers start interacting with their incredibly convenient Amazon device, why wouldn’t consumers grab groceries online.

“Hey Alexa, please order one gallon of milk, one loaf of bread, two tubs of yogurt and a jar of peanut butter every single week. And my recipe calls for pizza crust, tomato sauce and pepperoni, can you add those to my list as well”

With discovery the implications go even further. Can you imagine a Pinterest-esque future where you have favorites, Amazon uses AI to suggest meals, you star your favorites and Amazon automatically orders the ingredients?

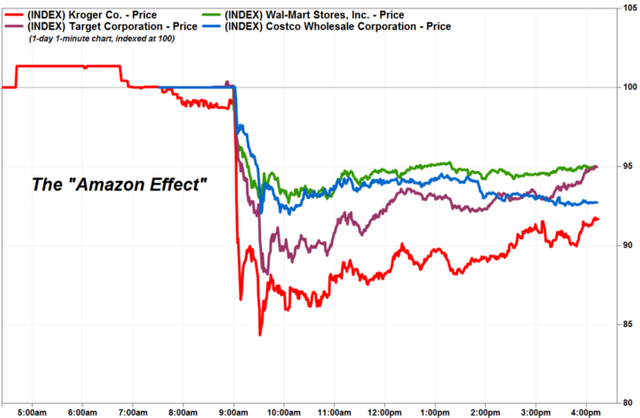

There is a reason the top supermarket chains values dropped a combined $13B following news of the acquisition…

Source: MarketWatch

5. Amazon Prime: #2 video streaming service, #6 music streaming service

The last main pillar of Amazon is complicated. Prime is both free 2-day shipping service and streaming for content and entertainment.

This is the perfect flywheel connector. Studies show Prime customers spend nearly twice as much on average as non-members ($1300 vs $700, numbers vary based on source). That alone is huge. And at $7.99/mo, Amazon is making even more money.

With Prime Music and Prime Video (both free with Amazon Prime), the added value is even greater. Both services provided UNLIMITED streaming access to Amazon’s entire catalog of licensed and original content, competing with services like Spotify and Netflix respectively.

Though both Prime services currently have less original content and smaller libraries than competitors, they are essentially free — keeping people in Amazon’s ecosystem.

If you can get free two day shipping plus not need Netflix or Spotify, you are ticking a lot of boxes.

It is estimated that 63 million US homes have Amazon Prime (up 35%) And ultimately Amazon just wants to increase Prime subscribers. These boost recurring revenue ($1.9B in Q1 of 2017) while nearly doubling organic purchases, all of which fuel the fire.

Source: Statista

Amazon has five powerful business units, any of which would be a successful business in their own right.

But the story doesn’t stop there. Amazon has also has compelling future growth opportunities.

Amazon’s growth opportunities

Going forward, Amazon’s strong leadership and vision of future have put the company in an incredible position. Each of the five main divisions is experiencing strong growth and have the potential to go significantly bigger.

But Amazon isn’t satisfied. Today, we’re seeing Amazon invest in its next bit opportunities. Let’s explore those in more detail.

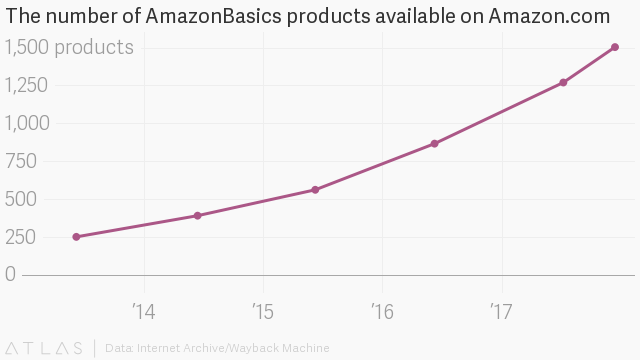

1. Expand Amazon Basics

As previously stated, Amazon Basics is Amazon’s ultimate goal. Once they own the end-to-end, they will have won. That said, while Amazon is devoting significant resources to scaling up their Basics product line, they have a long way to go.

As of Dec 14th, 2017, the Amazon Basics line comprised 1500 products (up from ~300 in 2013). Look for this trend to continue and accelerate. With over 480M products listed on Amazon.com alone, there is plenty of room for improvement.

Source: Internet Archive

2. Spin out AWS

It is my personal belief that Amazon runs the risk of regulation. While Amazon isn’t under attack like Facebook, Google, or Twitter; Amazon is approaching the point of market domination (monopoly) in numerous areas.

As individuals and lawmakers wise up, expect regulatory pressures to be applied. Amazon could preempt antitrust sentiment/action by spinning out AWS. As it stands today, AWS is the only division of Amazon not focused on commerce and logistics — also the best suited to be a standalone business.

This would greatly decrease the risk of government intervention (both locally and abroad). And let’s face it, everything Amazon does somehow pumps up the stock price. Odds are the combined market caps of the two companies would exceed Amazon’s current $604B cap.

3. Expand offline Retail

Amazon seems determined to build a local retail presence because while one-click shopping is lucrative, Amazon understands the importance of experiences (and shopping). And Amazon.com is optimized for conversions and upsells, and they are betting that bricks-and-clicks experiences can further increase sales.

I’d be inclined to agree. Trying on clothes and “shopping” is something many Americans love. And discussed in a previous post, local retail makes a ton of sense for products that either:

- have a high online return rate

- have high value to weight (or size) ratio

Expect to see Amazon rapidly expanding local operations to test out in-store experiences. More on this in our acquisitions section.

4. Increase video production

Have you seen The Big Sick? The Amazon Studios movie written by Kumail Nanjiani (Dinesh from Silicon Valley) was one of the best movies I have seen in a long time.

Amazon spent $4.5B for original content in 2017. They see an opportunity to attack Netflix ($90.57B market cap) by creating great shows and movies for Prime Video. And the future of video and entertainment is of course streaming services, Amazon sees this.

As Amazon increases their video library, their evergreen content will not only delight existing customers but attract new ones.

And in a world where content (and attention) is king, Amazon successfully owning the hearts, minds, and wallets of consumers is very very profitable.

5. Increase food focus

While Amazon’s $13B acquisition of Whole Food’s is exciting, the US grocery market is worth about $800B (about 6x Amazon’s worldwide sales).

That’s saying something. For Amazon to succeed in this massive market will requires focus and resource allocation. If they do it right, Amazon could easily double or triple their business in the next several years from now.

For more on how and the implications of the acquisition, see this post.

6. Explore pharma

Drugs are big business, especially in America — hence why Amazon is interested. And the mere rumor of Amazon exploring pharma caused the stocks of major pharmacies like CVS and Walgreens to tumble.

Source: FactSet

The US prescription drug market is projected to reach $610B by 2021. And as of 2016, the over the counter market made up another $33B.

That’s an entirely new, easy to access market nearly the size of groceries. And for Amazon it is a walk in the park. They already have the best logistics in the world. And customers already know, like and trust them.

Once Amazon branded generics are available, what percentage of consumers do you think will skip the inconvenient, overly expensive pharmacy?

It is time to push some pills…

Other factors to consider

I’ve written before about how tech giants are beating startups at their own game, and Amazon is the best example of this. There are few companies as prepared to manage disruptive change as Amazon.

Leadership

Amazon is one of the best managed businesses in the world.

This comes from a results-driven culture of experimentation, taking (and rewarding risks), customer focus, constructive disagreements, and ownership. And if you look at Amazon, the company really lives its rules. (For a more detailed description of how Bezos maintains such a killer culture, see this post).

But there are several things Jeff has done incredibly well while building Amazon. First and foremost is following through on promises with unwielding, efficient execution.

Look at the Whole Foods acquisition and the pharma announcement, Amazon’s rewarded by the market every time. In the eyes of the public, Bezos can do no wrong.

Bezos has carefully crafted the image of ruthless reliability and it allows Amazon the leeway needed to build for the future without focusing on short term profit.

Plus it helps that Bezos owns 17% of the company and is able to steer the ship.

Automation

Have you ever seen the inside of an Amazon warehouse? If not, watch this video.

The level of efficiency and automation is unprecedented. Everything is measured and streamlined. This helps Amazon keep costs low and quality high, even at massive scale — leading to vastly better unit economics. This makes Amazon’s incredibly low prices possible so no one can compete on price.

Artificial intelligence

Amazon has some of the best AI experts, period. Between the folks building Alexa to the millions of A/B tests running every day, and the eerily accurate product recommendations, Amazon’s combination of data and machine learning is rivaled only by Google.

And as anyone with experience in data and AI understands, this creates a flywheel where the rich get richer — which we clearly see with Amazon.

Strategic acquisitions

While Amazon is clearly one of if not the top tech company, their bank account is a bit smaller than others in the industry. At only $22B, Amazon cannot be overly aggressive with acquisitions. At the same time though, Amazon’s stock surged nearly 32% following the Whole Foods acquisition.

In the eyes of the markets, Bezos can do no wrong. Keeping this in mind, Amazon can probably afford to spend well north of $22B for the right strategic acquisition.

Here are the 6 most logical acquisitions for Amazon to make:

1.Video: With Amazon’s increased focus on Prime Video to compete with Netflix, an acquisition only seems logical. There are several ways this could play out and many potential candidates.

Likely Amazon can’t afford Netflix. If they could structure a deal however, this would kill cable for good and effectively make Amazon czar of entertainment (among many other things).

As Disney recently acquired Hulu and Time Warner has snatched up HBO, both of these services are probably off the table. If Amazon could acquire them though, it would be a huge win.

For the most realistic scenarios, Amazon should target smaller film studios and Youtubers to add to the Amazon platform. By bringing content from several genres (and hopefully stealing Youtuber followings), Amazon can further seed Prime Video with both long and short form video entertainment, effectively attacking both Netflix and Youtube in a single swoop.

2. Music: Much like video, Prime Music is a driving force behind Prime subscriptions which drives the flywheel further downstream. As such, growing the service should be top of mind for execs.

Unlike video, music presents much easier and likely more lucrative acquisition opportunities for Amazon.

Pandora, the most used music streaming service (free version), has a market cap of only $1.13B. That is chump change for Amazon. Between distribution and licensing deals, this could prove very enticing for Amazon to grow their subscriber base.

The other interesting player here would be SoundCloud, the streaming service that nearly goes bankrupt every few months. As Soundcloud clearly haven’t figured out monetization, this could be an interesting plug and play with Amazon’s existing infrastructure and customer base.

SoundCloud has raised $467M to date. They aren’t worth that now. An acquisition (or takeover) could pay back investors and set Amazon up for success.

SoundCloud specifically could also provide Amazon with an inroads into the podcasting arena (a hot, under-monetized space with huge potential).

3. Big box retailer: While retail is dying, Amazon is thriving. Rather than building stores themselves, an acquisition could make a lot of sense here. Target specifically could provide many synergistic benefits and likely murder Walmart.

Target has 1828 stores throughout North America. While these stores are bigger than I imagine Amazon would want, the distribution, storage space and upsell abilities would be very very interesting. And as Target’s market cap is only $37.58B (~1/9 of Walmart’s cap), this is definitely something Amazon could afford.

Add the fact that Target shoppers are Amazon’s ideal customers and you have a pretty interesting opportunity.

4. Fashion company: Amazon owns the customers and are expanding rapidly into fashion. Unlike most products however, fashion and clothes specifically are best tried on. And it isn’t just about fit.

Clothes shopping is much more about feeling than function. The emotion of trying on the perfect top or pair of skinny jeans is what drives the sale. People envision a better version of themselves, then they buy.

So if Amazon decided not to buy an all-around retailer (like Target) but to instead focus on fashion, Nordstrom could make a good choice. The luxury department store has 349 stores throughout North America and with a $8B market cap, it is comparable to Whole Foods.

Other great options include Kohl’s, Macy’s or J.C. Penney — each with unique advantages.

Don’t forget Amazon Basics, their goal is to make everything themselves. By being closer to customers, Amazon’s designers could more rapidly iterate on fashion trends before rolling out nationwide (Amazon’s better than anyone at experimentation).

Realistically it is impossible to predict, but look for Amazon to make a play in the fashion space in the next 2 years.

5. Wild card 1 — Ride sharing: This is an out-there theory with incredible potential. If you believe as I do that Uber is in trouble and ride sharing is a tough market, acquiring Lyft makes perfect sense. Here is why.

The unit economics of ride sharing currently don’t work. Due to the local vs global nature of the networks, every city can present competition. As a result, ride sharing is often a race to the bottom.

Yet how much do brands pay for advertising? Especially when you have the customers attention, this is valuable. Lyft could create the ultimate Amazon sales vehicle, quite literally upselling customers in the car.

In South Africa Uber drivers often add screens with advertising to increase their overall income. A similar system, either as a partnership or acquisition could make Amazon a lot of money. Between the locational data on where riders, Prime Music and Video on-demand and the always obvious Amazon.com upsells, this could be a big value driver (pun intended).

Plus Amazon could up the ante with Prime, offering discounted fares on Amazon’s Lyft service. This would swing the ball in Lyft’s favor while subsequently increasing the number of Prime subscribers (which drives Amazon’s flywheel 2x).

And if you believe car ownership is dead, driverless cars are the future and autonomous vehicles are an incredible opportunity, then this sets Amazon up to own even more of customer lives.

6. Wild card 2 — Telco: Imagine if Amazon owned Sprint. While easily the smallest of the US carriers, Sprint still has 50.4M customers.

And Amazon is already the place many consumers go to buy a phone. Well what if Amazon offered you a free month of Sprint every time you looked at phones (or some other enticing offer)? How many would bite?

I’ll bet a lot. And Amazon has free advertising on their own platform (plus in Whole Foods). Amazon could easily start to upsell mobile services (as most grocers already do with prepaid plans).

And while Sprint’s valued at $22.76B, this would likely be doable for Amazon. The impact on existing service providers would be huge. Given Amazon’s tendency to cut prices and reduce margins, users would flock to Amazon — greatly increasing the value of the acquisition, and crushing competitors in the process.

Plus as net neutrality dies (I hate it but at same time…), imagine the the possibilities for an Amazon-Sprint supercompany. Zero rating will probably be the first (and hopefully only) impact of repealing net neutrality.

With a merger inplace, zero rating Amazon.com and Prime Music/Video would greatly drive increase traffic/usage from Sprint customers. And others would sign up for just this reason.

The rating

It is hard to give Amazon anything other than an A+. That said, due to the nature of disruption and the potential of decentralized blockchain startups to upset the status quo, I’ll give Amazon an A.

Really the only two weaknesses Amazon has are regulatory risk and operating costs. The latter we have not discussed but bears discussion.

Currently Amazon is not (and/or barely) profitable. That is the only reason Bezos isn’t getting an A+. And while the markets have shown that profits aren’t important now, the climate can always change. If and when capital markets shift or Amazon suffers a big hit, their stock could tumble. At the very least they could have some rocky times and less smooth sailing.

That said I am very very long on Amazon. Welcome to the monopoly man of the future, Mr Jeff Bezos…

Closing thoughts

Amazon is quite a company.

The five-headed ferocious dragon is dangerous and dominant in nearly every area of their operations. And betting against Bezos is never a good idea.

But how will other tech giants stack up? Be sure to subscribe to never miss a thing.

So what do you think? Which companies are you longest on? Disagree with any part of our analysis on Amazon?

Before you go…

If you got something actionable or valuable from this post, like this and share the article on Facebook and Twitter so your network can benefit from it too.

LIKE THIS ARTICLE? THEN YOU’LL REALLY WANT TO SIGN UP FOR MY NEWSLETTER OVER HERE — AND GET SOME FREE BONUSES!