ScaredyCatGuide to Investing in Peer to Peer Lending (And Borrowing)

In the age of crowdfunding and direct online investing there are many more investing options available to the "average joe." One of those is Peer to Peer Lending. Below we will discuss how to not only invest in Peer to Peer Lending, but also how to use it as a borrower.

That's right, you now have an option to borrow someone besides the bank!

There are a number of Peer to Peer Lenders out there now. Prosper and LendingClub being the two most popular. Prosper has a better track record and my experience with them, as well as my colleagues, has been good so they will be used as the example.

Investing Money

With the current low rate interest environment, finding acceptable returns for your money is difficult. Peer to Peer lending offers returns of roughly 8 to 12 percent depending on how much risk you are willing to take.

The terms are 3 or 5 years as that is the duration of the loans they offer to borrowers.

What is great about this investment is that you can diversify your risk over dozens and dozens of loans as the minimum investment is $25 per loan.

This is great for a couple reasons:

- These are unsecured loans so you want to minimize your risk

- You can find a mix of low risk and higher risk loans to meet your desired returns

Becoming the Bank/Credit Card Company

When you invest (lend money) on Prosper you are basically performing the functions listed above. Someone borrowing money at Prosper is doing so to consolidate debt, borrow for remodeling costs, make a large purchase, etc.

Mitigating risk by loan type - I will only invest in loans that are for debt consolidation. If someone is taking a loan for this reason it means they are making a smart financial decision to reduce their debt burden. I much rather invest in someone making that decision than someone who is taking the loan out to buy a boat.

My personal preference, but it is a rule I invest by.

Creating an Account

We don't need to get into the minutiae of signing up and creating an account. However, it's simple and straightforward. Just got to Prosper.com and they will ask you for the standard info with most signups.

If you are going to lend then you will provide info in order to send funds over. If you are going to borrow then they will ask you for standard credit and income info as will any loan.

Loan Shopping

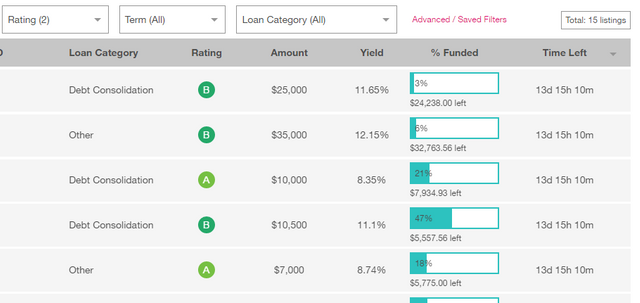

What I do want to show you is an example of loan shopping. In the below screenshot you can see a handle of brand new loans that are being funded. You have options to search on particular criteria. In this one I have searched for only A and B rated borrowers.

You have the ability to invest a little as $25 in any of the loans listed and as high as the amount available if you want to get crazy and load up on one borrower. Again, the option is up to you.

As you can see the rate being offered is between 8 and 12 percent. It also lists the size of the loan and the percentage of it that has already been satisfied along with the Loan Category.

Remember, I am only investing in debt consolidation. If you take a closer look you will see that there are a few in there with "other" as the category. Notice they are paying a slightly higher rate than the consolidation ones. Again, this is because there is more perceive risk and less clarity.

Prosper has a dozen loan categories spanning things like engagement ring financing to baby and adoption loans to something more simple as home improvement.

With that many options I have no desire to invest in "other" cause who knows what it could be.

Borrowing Money

Let's look at the other side of the coin. Let's say you need a loan.

You would create an account an apply for a loan (the process is quick and painless). I did it as an exercise and it was one 5 minute phone call to see what rate they would lend to me and the maximum they would lend to me.

It's not the cheapest way to borrow, know that. I was quoted at 11.9% and that's with a top notch credit score. However, you can get funded in just a matter of days and if you are paying off a debt with a higher interest it does make alot of sense.

There is a fee upon borrowing, but then that is it as for as borrowing costs go (excluding what you pay in interest of course). The loan origination fee is a percentage ranging from 0.5 to 4.95 percent depending on your credit score.

Conclusion

This space is still relatively new being about a decade old now, but it is another example of the "sharing economy" that is opening up more and more options to mainstream society.

Regards,

Thanks for the pic pixabay

Disclaimer: Info in herein is my opinion and for educational use. I'm invested in loans at Prosper, no other affiliation.

When you are picking out loans, do you look at any other info besides the purpose and percentage rate?

The only other thing I look for is repeat borrower. If someone has already borrowed once and repaid in full then I will favor investing in that loan.

This is fascinating information and I will definitely be looking into this as a way to invest small (to start) and perhaps build a reputation. Thank you!

Thanks, yes start small and master the craft. It's amazing all the options we have these days.

Good article.

For people based in the UK, there is a similar service called Zopa. I have been investing (i.e., making funds available for loans) there since September 2008 - makes me a pioneer. My investment was small and the returns have been way better than a bank deposit (even after accounting for bad debts)

Zopa is open for UK residents only (UK bank account and proof of residence). They have come a long way since I started especially on managing credit risk. I have never taken out a loan - I can only comment as an investor. In the early days I spent quite a bit of time choosing which class of risks to take (A, B and C). With the new Safeguard Fund one does not need to worry - Zopa looks after everything

I would suggest it is a strong way to build up regular savings setting aside a specific amount each month or each time you have spare cash. However, you do have to bear in mind that loan durations are quite long - 3 to 5 years - so it is absolutely a savings vehicle for the longer term.

Check it out here http://mymark.mx/Zopa - an affiliate link

Good stuff. Thanks for posting for any UK readers.