HOMELEND — A MORTGAGE CROWDFUNDING PLATFORM

INTRODUCTION

Mortgage loans are at the core of society. One of our basic needs as human beings is shelter. Buying a TV, embarking on holiday travel, starting a business, or even sending your kids to college… These are choices you can choose not to make in order to avoid becoming indebted. But not having a home isn’t — or shouldn’t be — an option. For most people, the only options for housing — besides living with their families, friends or relatives — are either renting or buying a place using a mortgage loan. Few are able to make a cash home purchase. Indeed, in the U.S., cash transactions account for only a third of home purchases1. Even when someone is able to pay cash, a small mortgage loan might continue to be preferable as mortgage interest payments can, in some places, be deducted for income tax purposes

BLOCKCHAIN AND THE MORTGAGE INDUSTRY

Blockchain and smart contracts have the potential to save between US$ 3 billion and US$11 billion to the mortgage industry.- Capgemini Consulting

Many areas in the financial world have been disrupted by the Internet revolution. However, mortgage lending, despite being one of the largest areas, is still generally conducted under the same traditional system. The mortgage value chain has grown in complexity during the past three decades, due to the trend towards securitization, which has significantly amplified financial supply. Nevertheless, mortgage lending processes remain mostly paper-based and involve many players, making them complicated, tedious and slow.

This has several negative consequences for the borrower as well as for other parties involved. For instance, many borrowers are burdened by the sheer amount of paperwork they need to manage. But the large amount of documents that need to be filled and the number of entities involved in the mortgage origination process are a consequence of two facts. First, there’s a real need for information gathering, analysis and checks to guarantee that the mortgage loan will be repaid. Second, this continues to be a paper-based legacy process that has not been sufficiently modernized and aligned with technological progress. Both facts contribute to cost increase

Blockchain technology has an enormous potential to address both of these facts. Due to its distributed nature, a blockchain ledger can significantly ease the transfer of and access to information for each of the parties involved in the mortgage value chain. Also, with its unique capability to generate trust, transparency, and record immutability, it is an effective move toward digitization, not only of mortgage documentation but of all related business processes. In the next sections, a brief explanation of the mortgage value chain will be given in order to point out the shortcomings of the current system. As will be observed, many of these problems can be addressed through blockchain technology

HOMELEND’S MORTGAGELENDING PLATFORM

P2P Lending and the Mortgage industry:

Peer-to-peer (P2P) lending, also known as “alternative finance,” is the process by which individuals can borrow and lend from each other without the intervention of banks or other financial intermediaries. It was made possible thanks to the Internet revolution. P2P lending platforms such as Prosper and Lending Club have been in operation for more than a decade in the U. S18. In fact, the market has outgrown expectations: ten years ago, experts estimated a US$10 billion market size for U.S.19. In reality, at the end of 2016 the market size was US$34.5 billion20.

Homelend’s P2P mortgage lending mechanism

Homelend P2P platform works by embedding mortgage lending business logic into smart contracts. This is the platform’s core functionality. By creating a set of smart contracts that execute business processes, Homelend allows individuals to borrow money from their peers in a trusted, transparent, and secure way. The key idea is that borrowers and lenders are not linked by means of a financial intermediary (i.e. a bank or a centralized P2P lending platform), but rather by smart contracts that automatically execute a pre-defined business logic.

Any mortgage loan, to be successfully originated, must follow a pre-determined path. From the moment when a potential buyer of a property applies for a loan, to the actual closing of the mortgage loan and transfer of the property from the seller to the buyer, a series of business processes take place. These processes are instrumental. They are subordinated to three main objectives, issuing a loan that:

makes possible the purchase of a property;

can be successfully paid back by the borrower; and

can be recovered to a satisfactory extent in case of default.

P2P lending methods

Homelend will develop three different P2P lending methods: pure crowdfunding, pooling, and auction. In each of them, the flow of financial resources is controlled and executed by smart contracts, without middlemen or financial intermediaries. Also, the splitting of mortgage loans into “slices” is present in each method. The difference between the methods arises from the specific approach used to and a pre-approved mortgage loan.

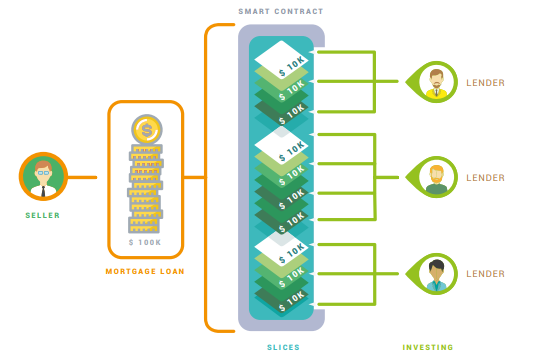

Crowdfunding method

Under the crowdfunding method, which is the simplest one, potential lenders will find investment opportunities in the form of the aforementioned “slices.” From the borrower’s perspective, his pre-approved mortgage loan will be divided into smaller fractions, such that different lenders can finance his loan by funding these “slices.”

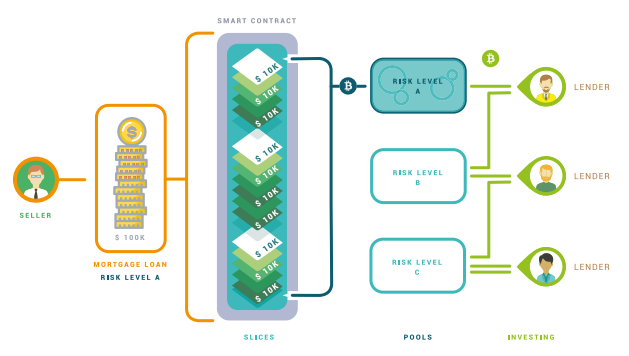

Pooling method

The pooling method adds some economic flexibility to the system, but is also less simple from a technological perspective. In contrast to pure crowdfunding, under pooling, lenders will be able to invest money through smart contracts before the specific mortgage loan to be financed has been pre-approved. The investment is conducted under the same “slices” framework. The difference is that the smart contract will allow lenders to “pre-buy” the “slices” before they have been properly created (after a mortgage loan pre-approval). To this end, the Homelend system will classify mortgage loans according to their risk level. Loan applications will then be pre-approved under a specific risk category. Thus, potential lenders will be able to invest by sending cryptocurrency to the balance of the smart contract that controls the process of a specific risk category.

The advantage of the pooling method is that it allows some level of financial buffering, without the need of a financial intermediary or a middleman. In other words, in contrast with pure crowdfunding, the total amount of funds sent to the smart contract by lenders can be higher than the size of pre-approved loans managed by the specific smart contract.

The smart contract will allocate funds from risks pools to specific slices on a first-come-first-serve waterfall basis. What this means is that investors will subscribe to a specific number of slices, and as mortgage loans are pre-approved and sliced, the available slices will be allocated to the earliest investor, for the number of slices subscribed, then to the second earliest investor, and so on.

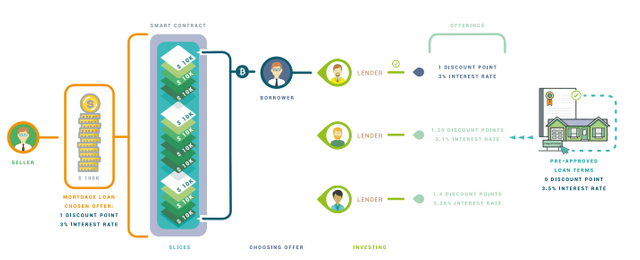

Auction method

The auction method will be developed as a variant of the pure crowdfunding method. Unlike pooling, no financial buffering will be involved. The central difference between the auction method and pure crowdfunding is that lenders will be able to offer borrowers better conditions than those pre-approved by the platform. When a mortgage loan is pre-approved, it will be divided into “slices” the same way it is under the other two methods. The size of the loan, its duration and conditions (such as whether the interest rate is fixed or variable), will not be subject to any change. However, lenders will be able to bid on specific “slices” by offering better terms in two ways:

by charging a lower interest rate than the one pre-approved; and

by providing discount points to the borrower.

BUSINESS MODEL

Homelend is being developed as a blockchain solution that will significantly increase the housing financing possibilities for many individuals and families. Our value proposition is socially sensitive and anchored in a P2P progressive approach that aims to use technology for society’s benefit. Nonetheless, Homelend is also based on a sound and profitable business model, which consciously reaches out to address an underserved market. On the one hand, Homelend creates an investment opportunity for many individuals, with a solution that unites a traditional industry as real estate, with an innovative technology like blockchain. On the other hand, it makes possible for many individuals (who due to various circumstances, including current limitations in the traditional credit risks models, do not possess a solid credit score but are otherwise creditworthy) to access to housing financing and solve one of their most basic aspirations: having a home of their own

Go-to-market strategy

Homelend will pursue a go-tomarket strategy based on two pillars: rapid growth in the number of users (sellers/borrowers/lenders), and a targeted approach to segments underserved by mortgage banks

The primary users of the Homelend platform will be borrowers and lenders. Those who intend to acquire a new home or refinance their current one will gain value from Homelend in several ways. First, they will enjoy an easy-touse, state-of-the-art application platform. Borrowers will be able to apply for mortgage loans and begin using the platform free of charge. The only thing a prospective borrower will need to do in order to use Homelend is register on the platform using an email address.

Other platform services

Property listing

Homelend aims to develop a P2P lending platform that will not only create financing opportunities for millions of financially excluded people, but that will also increase efficiency and speed in the origination process, significantly reducing the amount of time it takes to close a mortgage. As previously discussed, this increased efficiency will be based on the automation provided by smart contracts. In order to further speed up and streamline the process, Homelend will offer sellers the opportunity to list their properties on the platform, in turn enabling prospective borrowers to search for a home directly from within the platform. If a property is listed on the platform, the seller will deposit HMD equivalent to 0.1% of the selling price as a listing gas.

Digital closing

As previously mentioned, digital closing of mortgages is finally becoming a reality, at least in the U.S. market. With Homelend, digital closing is an important element as it reduces the time between a mortgage loan getting fully funded and the day of closing. To this end, Homelend will work with digital closing providers who will find, through our platform, an extended and captive market. In the same way that a commission is charged in addition to the appraisal fee, Homelend will receive a commission over the fees charged by digital closing companies. Again, this will be a premium paid by the borrower for accessing financing in a more efficient and inclusive way.

TOKEN GENERATION EVENT

The choice to create a utility token has been carefully considered by the founding team, and it is based on several reasons and goals. Below we describe the rationale behind the issuance of HMD tokens. friction costs in the form of commissions, origination fees, etc. These are unavoidable to some extent, as they represent the remuneration for a service provided. Other friction costs stem merely from the involvement of middlemen. Some friction costs are specifically related with money flows. For instance, it is well known how high transactional costs for international wire transfers are, where banks charge commissions as high as $40 plus a significant spread over the exchange rate. These transactional costs are also present in cryptocurrency exchanges, particularly with fiat currency/cryptocurrency exchanges.

Justification for a token

The creation and issuance of a crypto token for Homelend is justified by the platform’s economic dynamics. In contrast to many other ICOs or TGEs, whose final product is not necessarily blockchain-based, Homelend is developing a lending system that has, at its technological core, smart contracts and distributed ledger technology. A key feature of the system is the reduction of friction costs, and the availability of the service for a wide population underserved by banks or other mortgage lenders. Indeed, the system will be able to operate independently of any third party/financial intermediary that needs to approve the transfer of fiat currency.

Token functionality

The HDM token’s main functionality will be to offer access to the services provided by the platform. These services will either be provided directly by Homelend or through third parties working in coordination with Homelend. The core service provided by the Homelend platform is the facilitation of P2P lending by means of smart contracts and standardized processes. The system will create a more affordable, accessible and efficient mortgage origination process. As previously mentioned, the borrower will deposit an origination gas equivalent to 1% of the mortgage loan, in order to access the financing mechanism.

Token economics

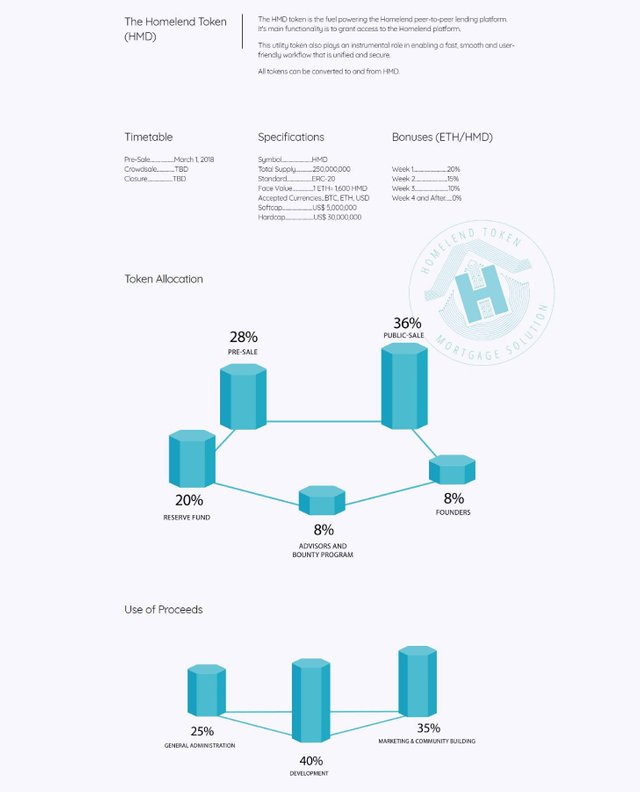

Token economics Cryptocurrencies and digital tokens have generated new ways of transferring value and clearing transactions. While different in many important ways from government-issued currency or the old bank notes from free banking times, some basic monetary theory principles remain applicable insofar as they purport to have transactional functionality. One of the most basic principles is the importance of token supply for the sound operation of the system. Many Initial Coin Offerings (ICO) or Token Generation Events (TGE) have been conducted in recent years. Most of them issue tokens that are qualified as: “utility tokens” with transactional value: they are meant to be the medium of exchange inside the platform or system to be developed29. However, few of them explain why a specific token supply has been chosen. They limit themselves to indicating the total number of tokens to be created and how they will be distributed.

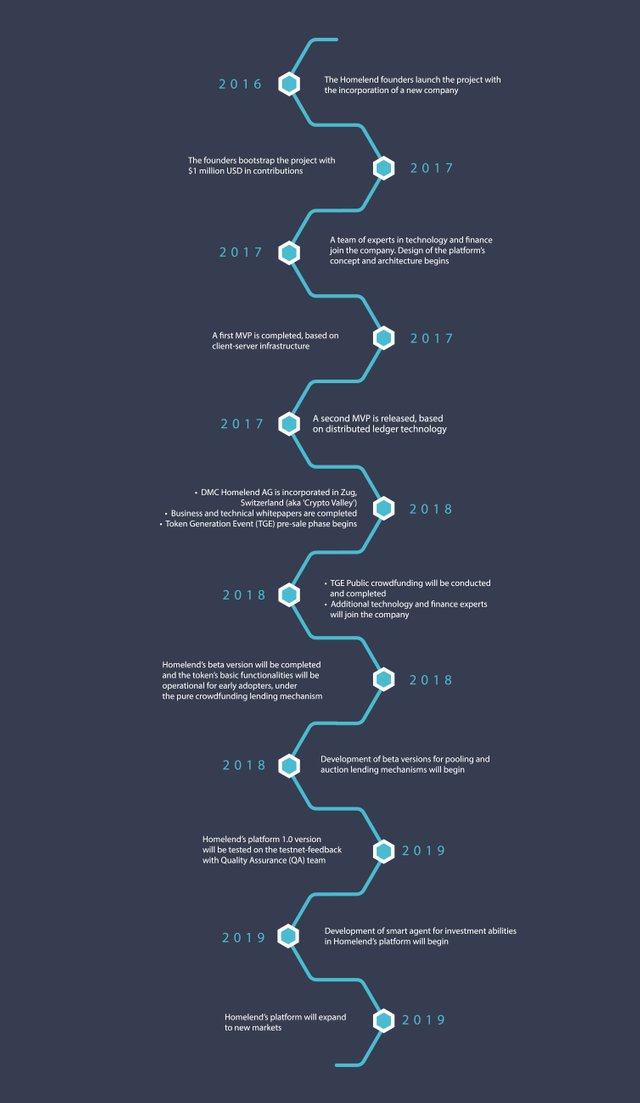

ROADMAP

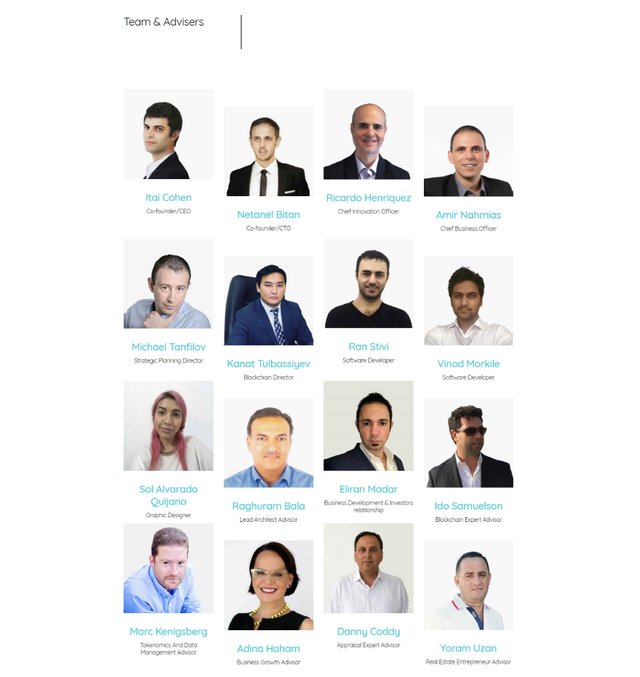

TEAM

FOR MORE INFORMATION ABOUT THIS PROJECT VISIT :

WEBSITE: https://homelend.io/

WHITEPAPER: https://homelend.io/files/Whitepaper.pdf

ANN: https://bitcointalk.org/index.php?topic=3407541

FACEBOOK: https://www.facebook.com/HMDHomelend/

TELEGRAM: https://t.me/HomelendPlatform/

BITCOIN TALK PROFILE: