Why buying a home is a terrible investment

With rent prices and housing prices going up at the same time, without looking to deeply into the numbers, buying a home seems like the obvious choice.

Most home buyers go through the same thought process: A home provides convenience of all sorts when it comes to storage, recreation, and even when you have visitors, much better than an apartment. A house also is something you can build equity in. When you rent, you're just throwing that money away.

The problem with a lot of beginner real estate 'investors' is that they focus too much on a rise in property value, and they don't think about month to month expenses and taxes that you otherwise wouldn't experience as a renter. The real power of real estate lies within its ability to create an abundance of cash flow. If you want gamble on something based on a presumed rise in market value, you should probably be betting on cryptocurrencies or stocks, not a home.

Cash flow real estate vs single family homes:

To help you get a better idea of why cashflow real estate is much more profitable and prudent, I've put together an example.

This example has: a couple in a single family home, A couple in a single family home with a roommate (paying rent), a couple in a duplex renting out one unit, and a couple living in a 4 unit apartment renting out 3 of those units. All of which have 20% down on a 3.92% 30-year mortgage, with 1.15% property tax.

For a single family home in the United states, the average market price is about $200,000. On the mortgage terms described above, the monthly payment would only be $757 a month. So much cheap than paying $1000 per month in rent, right? Wrong.

At the end of the month garbage, sewer, taxes and other expenses quickly add to that $757. You really end up paying about $1,200 per month.

Let's say you bring in a room mate. Sure you might pay a few hundred dollars less on your mortgage, but you have to decide if having a roommate is really worth a few hundred dollars to you.

In a duplex, the situation is a bit better, but you're still net negative.

In the 4-plex, the situation gets better and is even profitable. It would become even more profitable when you move out of the 4th unit and rent all four units out. Keep in mind that I calculated this situation with only 3 units giving rental income.

Since a rise in market price is never guaranteed, buying a single family home will almost always be a losing situation due to lack of cash flow. Even real estate deal with cash flow is very difficult to make profitable, so it is important to crunch the numbers a few dozen times and always factor in worst case scenarios.

The 2008 housing bubble has raised our expectations:

Back in 2007-2009, we saw a lot of middle class people lose their proverbial shirts trying not to miss the housing boom gains. There was such a euphoria in the markets, as if no matter what real estate you bought, you would be richer for it in a few years. If you're investing in real estate for gains and equity, you're not investing. The most powerful part of real estate will always be the cash flow. With a single family home, there is no cash flow.

Like history has shown us in the past, there is no get rich quick, there is no free lunch, and there is certainly no such thing as...

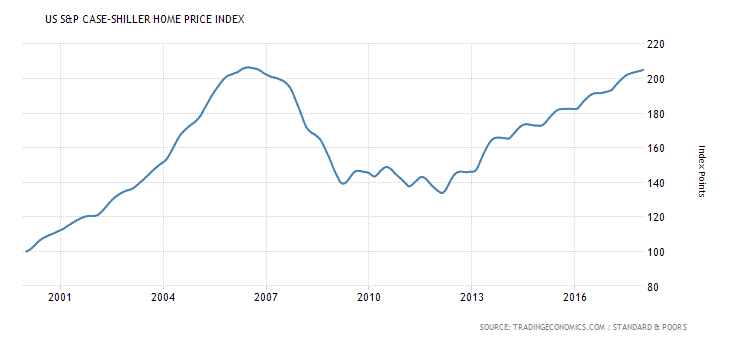

The Case-Shiller Home Price Index:

The Case-Shiller Home Price Index is a market index that tracks the price movement of the home market. From 200 to 2008 it rose over 100%. That's an average of a 12.5% gain per year.

The unsustainable gains in the home market led to extreme price decreases on the other end.

After an awesome market run from 00-08, people expect prosperity to continue to flow in through equity gains on their home for years to come. But can it continue?

To answer this question, let's take a step back and look at some data.

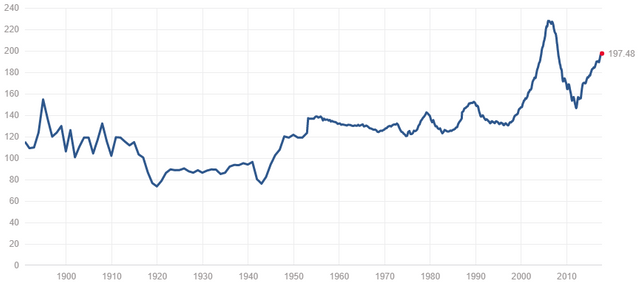

The Case-Shiller Home Price Index long term:

Here we have the Case-Shiller Index price adjusted for inflation.

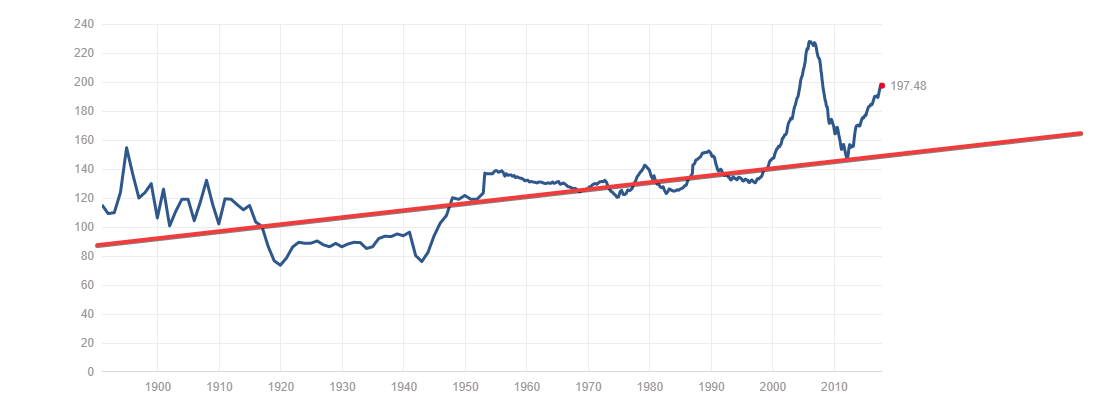

Let's draw a subjective line through the middle to represent the mean.

Here's the data according to multpl.com:

Mean:148.92

Median:139.68

It's fair to say that home prices need to revert to the mean or even below it sometime in the future.

I expect average home prices to drop 15-30% over the next 3-8 years.

But what other factors point towards lower housing prices?

Rising interest rates will negatively affect prices

As you may know, there are different types of interest rates, but all are correlated. There is the federal funds rate, the US government treasury notes (ranging from 1 month to 30 years), and there is the consumer loan rate.

The Federal funds rate is determined and controlled directly by the federal reserve. They lower it when they think the economy needs stimulus, and raise it when they believe the economy is on stable ground. This causes expansions and contractions within the US dollar money supply, which has an impact on consumer spending, consumer borrowing, commodity prices, and asset prices.

Though this rate doesn't directly effect the rates of treasury notes, it does effect how the markets' perceived value of debt instruments. If market participants believe interest rates are going up, they will wait to buy income-producing debt instruments at a better rate.

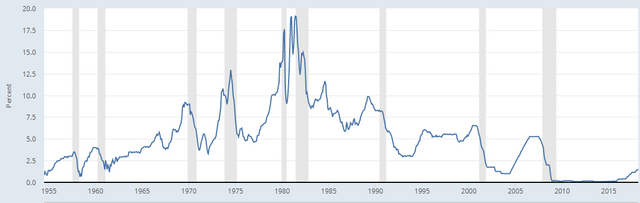

The fed funds rate has been on a steep decline since 1981. It's been effectively at 0% for 6 years. This has never been done before.

Low interest rates have created extreme bubbles in assets prices, yet inflationary effects have yet to be seen on the purchasing power of the US dollar.

The federal reserve has no choice but to raise interest rates, or keep them near zero for eternity. Raising interest rates too much could cause a deflationary spiral in asset and commodity prices (prices of goods), while keeping interest rates low could ravage the purchasing power of the dollar over time.

The federal reserve and Jerome Powell plans to raise the fed funds rate 3 times in 2018. You can read a New York Times article about it here.

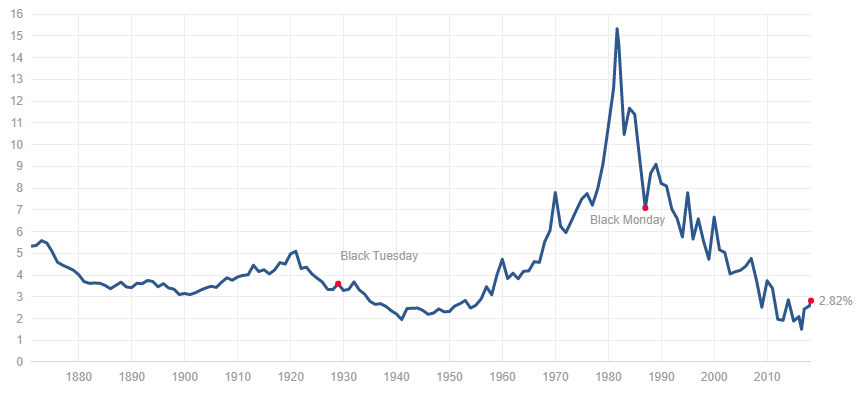

The government US treasury notes, or bonds, are used by investors to lock in a steady flow of interest on their money. Typically bonds are used during times of uncertainty in equity markets (stock markets). however, bond rates are so low, it's almost not worth it to even bother locking your money in with them.

In 1981, a 10-year bond returned 15% per year. Today the same debt instrument only returns 2.8%.

With a rising fed funds rate, US bonds will rise as well. The US 10-year bond has been known to be used by investors to develop an outlook of how the economy will look in the future.

If you would like to learn more about bonds, check out my past article What the Bond Market is Telling Us About Assets...

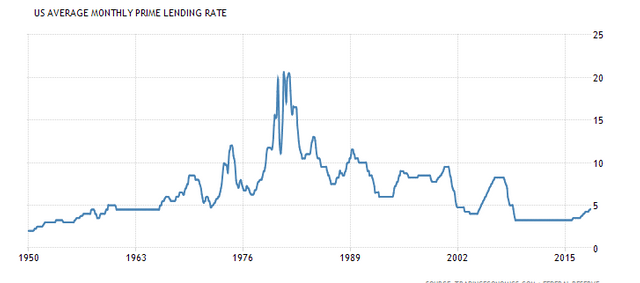

Let's get to what really impacts home prices: the consumer loan rate.

More specifically let's take a look at the 30-year mortgage rate over time.

With rates at lows that haven't occurred since the 50's, it's likely that we will see mortgage rates rise in the long term towards a more reasonable level. This will most certainly cause a drop in home prices.

Why would it cause a drop in home prices? Because, like everything else, consumers buy things based off what their monthly payment will be.

With a higher interest rate, the monthly payment will be higher, and it will be much cheaper for the consumer to just rent. This will lower the demand for homes and thus cool down real estate markets across the country.

If the federal reserve stays consistent, it is a safe bet that home prices are on their way down.

Moral of the story?

Don't invest into real estate in hopes of a rise in market value, go for net positive cash flow. A bad real estate deal can set you back for a long time.

Thanks for reading!

Disclaimer: I am not a financial advisor. The articles that I write are for educational purposes only. Do your own research and hold yourself accountable for the investments that you choose to make.

Check out some of my most recent articles, your support is much appreciated:

The Most Effective Way to Invest in the Stock Market

Why Saving Cash Will Make You Poor

Intelligent Investing: Becoming a Shrewd Investor

How Do Gold and Silver Fair During Asset Deflation and Economic Recessions?

Wyckoff Logic: Finding Entry into a Market

Bitcoin: Testing Major Resistance

Yamana Gold (AUY): An Undervalued Stock with a lot of Potential

The Case for Precious Metals and Mining Stocks

Are you a trader? Do you hate paying brokerage fees and commissions? Sign up for Robinhood using my link:

http://share.robinhood.com/micahm18

Robinhood is the first zero fee stock market broker that offers free option trading, crypto trading, and much more. I make all my trades on this platform and pay no commission. This is a zero obligation sign up. All you need is your personal information such as your ssn, birthdate, and your name. Robinhood is an SEC and FINRA regulated company. Robinhood is fully monitored and registered with the SEC (securities exchange commission).

1 in 150 chance of getting a Facebook, Microsoft, or Apple Stock

1 in 90 chance of getting Ford, snapchat, or AMD stock

100% chance of getting a free stock

Robinhood... Taking from the rich, giving to the poor...

Follow me on social media: