psd2 could be great for open banking but also who picked that god damn name, what is this photoshop files v2? — an EU directive we will have after Brexit anyway?

Yeah great naming convention europe, props for that!

It was interesting to see apps like revolut jump straight into the fanfare about it, because it's obvious it’s going to impact that fintech market straight away. They are already ahead no doubt and they are recruiting people like crazy — I’m expecting that service to have a shelf life of a few years before they sell out to a bank so basically back to square one.

I don’t bring any technical information to the mix in this post, if you want to read up on it this piece from dw.com I think is pretty solid — PSD2: New EU rules to make credit card transactions cheaper, faster and safer | News | DW | 13.01.2018

Loving the fact that ‘extra charges’ will fall away (not without a fight I’m sure, expect account charges in 3-2-1) and I do like that we have this third party sharing thing. Especially if we end up with some blockchain fintech companies jumping into that space with AI or neural networks being ‘suggestive’ of ways to invest our resources in projects both local and global.

That could bring about a new ‘all boats’ rise situation and approach to the way we look at value itself, instead of this race to the lambo bullshit i often see with people desperate to be millionaires like it matters.

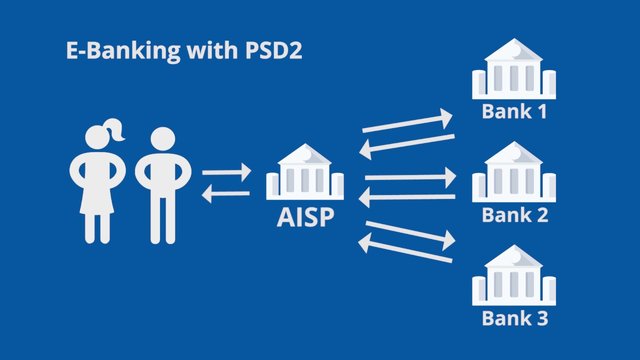

Also feels like this is the EU ‘catching up’ I mean take Estonia with their @eresidency program x-road that they have had for years which does exactly this, one app - many data silo points to bring information in. It’s not like it’s something new really it’s just about tearing down some of those privacy walls of access to locked away silos.

You only have to look at the data of 86% of under 30’s being ‘ok’ with giving access after all banking should be an app on a phone in the digital age, this is 2018 for god sake. Do we really need the high street full of banks with humans in when a huge chunk of the work that banks supposedly do for us can be automated anyway?

My own interactions with banks over the years has left me frustrated, annoyed, felt like it was just an upsell and they have weird ways of looking at overdrafts (like, surely a limit is a limit that you can’t go over?! -- I say bring on the mobile, local, global, connected blockchain economy of digital assets banking. Let me money work for me, let it contributes to the global good of my fellow humans and let me invest in projects like kiva.org with the flick of a switch — maybe this way would be better to teach our children a better way to manage money than the way you see in school.

Of course on the flip side, I do have privacy and data paranoia but that’s the world we live in, data and silos are bought and sold, cross-referenced by ‘agencies’ and ‘services’ from all nations to the act of data mining and algorithm analyse. In a world rapidly marching into quantum communications the more routes into cross-referencing that’s possible the more it’s going to be suggested — money to me has always been this multi-headed hydra no matter what head you cut off ;)

I guess in some ways it’s why visa is so damn scared of allowing companies like wave crest to issue credit cards to crypto currency needing fiat customers. Maybe they didn’t like not being the people to do it, maybe they cut of a head so that they could grow another and be seen as the company to ‘innovate’ on the back of someone else’s idea — you can’t change the middleman without changing the greed and the behaviour of the people at the wheel and you can be damn sure they wanna hold onto the wheel as long as possible for the journey outcome they have.

In a world that won’t stop for any middleman and that has access to information and choices, with communities popping up localised mesh networks and people getting back to speaking to other people face to face about their wants and needs, skills and services we are seeing the utopian vision of what arpanet did for defense networks — from war to porn, to social media to social blockchains, you just can’t stop this SS t’internet ;)

p.s - The Government must comply with EU directives until Britain leaves the bloc, although these changes will become part of UK law so will remain after Brexit

I personally don't see how PSD2 is going to make a great deal of difference in the short term and in fact, over the long term, I can see it being more expensive for consumers to access all types of banking service. Choice does not always mean cheap. Banks haven't been 'forced' to open their data, they'd love to sell access to it, but for huge amounts of money, money that would have to be recouped by the purchaser.

The main people this will benefit are the loan sellers, the scummy payday loan companies, insurance companies all begging for your business. Bloated charities sending you messages how they noticed you had 3 quid left in your account last month and could you please give it to us....I prefer privacy to saving a few coins any day of the week.

And what about government? Now they can legally have a look at your financial data just by paying the bank, they don't need court orders or sneaky spying.

If people like Equifax can have their data compromised, anyone can.

I see very few upsides here, except maybe quicker and more direct transactions. Location data, where did you buy your coffee this morning / How did you get there? I allow access to my personal data simply on a need to know basis....scummy payday loan companies don't!

Typed by a man who hasn't had a traditional bank account for 12 years or a credit card for 20 years.

Its getting more Orwellian by the day :-(

Have a great day Mr Humble :-)

i always have a great day! but thanks for saying so! :)

we spent our 'privacy' over 'choice' years ago, privacy is an illusion personally for me knowing all the failures in the chain of technology over the years. the government has always done whatever it wanted regardless in my eyes ;)

1984 man, everyday! :) -- yeah i don't have a 'bank' as such but i do have one of these new fangled cards from these new fintech app companies. i'm just interested in the process of going through it. i don't have a phone number so i don't get scummy payday loans or any of that shit at least.

thank you for replying! :)

Make no mistake, the new 'fintech app companies' are very close to 'real' banks with full FCA licenses, some will be very shortly. Your Revolut is currently applying for a full European Banking License in Lithuania for example. My beloved Monese is a banking 'service' registered with the FCA so these new challenger banks are leading the charge against the traditional banks. And it is with these new banks I trust :-)

Youre right about privacy of course, it's an illusion but it's an illusion that is fading slowly but surely just as long as we fight back and actually care about, and control what happens to our personal data !

Regards :-)

i ain't got nothing to hide, anything digital is lost straight away in my mind or can be manipulated -- at that stage do we simply get under the bed with our paper notes and FIGHT the power? dunno. i think it's just a game, a game where we take part and lose from time to time and celebrate the small wins :)

also 'Lithuania' and 'Banking' is not something that falls of the tongue easily! lol.

lol...Monese uses Estonian banks.....what will happen after Brexit is anyones guess but it will be sad if it forces the fintech scene out of the UK.

thanks for post @teamhumble

don't spam. it's rude.

I wrote it for what I really like

i use coinbase for exchange...i must appreciate you because this post is worthy to be embraced

you don't have to appreicate me, but if you want a hug just ask.

Hey man u no Im a fan

but a little bit of formatting and punctuation, it's a little hard to follow.

sorry man, i'm not a writer (made some corrections especially for you just!)