401(k)… IRA… You’re Screwed!

Ever Timed the Market Wrong? How About Your Taxes?

***2. It conditions people to accept a horrible, horrendous fate of working for 4 decades in order to enjoy their savings during their weakest years – years where they have no idea what their health will be like or if they’ll even be alive.

***3. It convinces people that they will pay lower taxes when they are older.

This last one is the worst. I remember hearing this from a school counselor at 15 years old, and I couldn’t believe it. To actually plan to be in the lowest tax bracket… Or as I saw it, a plan to be a low-income senior citizen… F that!

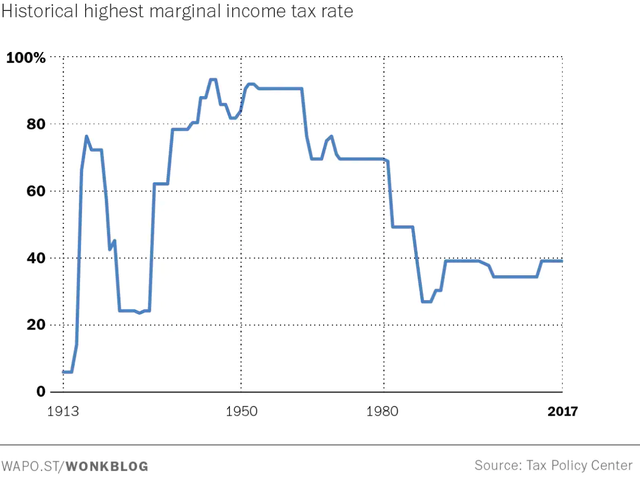

Here’s the real scam of the whole thing summed up in this chart.

Income taxes are the lowest they’ve been in decades!

93% Of Investors Generate Annual Returns, Which Barely Beat Inflation.

Wealth Education and Investment Principles Are Hidden From Public Database On Purpose!

Build The Knowledge Base To Set Yourself Up For A Wealthy Retirement and Leverage The Relationships We Are Forming With Proven Small-Cap Management Teams To Hit Grand-Slams!

And prior to the 1980s, you have to go back to 1931 to find them this low.

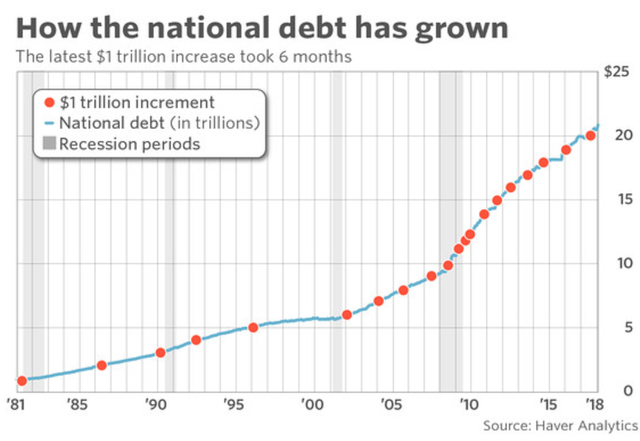

Here’s another chart to reflect on, as CPAs and the conventional finance community recommend you “avoid” paying low taxes.

They’re trillion-dollar annual deficits, soon to be trillion-dollar interest payments.

We are less than a decade away from seeing the U.S. actually make trillion-dollar interest payments on the official national debt.

Keep in mind that we don’t account for our off-balance sheet items, like Social Security payments owed to 75 million baby boomers!

$21 trillion is the number you hear about, but it’s really closer to $200 trillion in total liabilities.

The U.S. Federal Government revenues pay for our entitlement programs and the interest on the debt.

All other programs, from our military to our Congress, are paid for using borrowed money.

This is completely unsustainable, and as I’ve warned before, many of the socialist groups rising up are downright scary if and when they get in power.

So the bottom line is your taxes are going UP in the late 2020s and by the end of the 2030s, we could be paying more than 50% of our income just to the Federal Government.

Now, consider the tax deduction from a 401(k), SEP-IRA or IRA, or any tax avoidance vehicle… WHY?

Why avoid paying low taxes today to speculate on the future, when in all likelihood you’ll be paying a much higher tax rate?

Imagine borrowing money from a bank and the banker telling you he’ll decide what your interest rate will be in 20 years. You wouldn’t take that deal in a million years.

Yet that’s exactly what people are doing when they max out a 401(k), only it’s even worse than giving a banker a blank check – it’s the IRS!

It’s the IRS and the voters of 10, 20, or 30 years from now deciding what you get to keep.

In my opinion, everything about retirement is a misallocation of time, energy, and capital.

Financial independence can be done within 5 to 10 years by dramatically cutting expenses and focusing 90% of your investible assets on cash flow by bringing in multiple streams of income.

Start-up investing is also something we are very focused on here at Future Money Trends.

Next weekend, I’ll have a NEW cannabis stock suggestion, one that is going to be a nationwide dominator here in the U.S.

Have a great Sunday, everyone!

Best Regards,

Daniel Ameduri

President, FutureMoneyTrends.com

Legal Notice: This work is based on SEC filings, current events, interviews, corporate press releases and what we’ve learned as financial journalists. It may contain errors and you shouldn’t make any investment decision based solely on what you read here. It’s your money and your responsibility. The information herein is not intended to be personal legal or investment advice and may not be appropriate or applicable for all readers. If personal advice is needed, the services of a qualified legal, investment or tax professional should be sought.

The only choice that makes sense in "retirment land" is the Roth IRA... A self-directed one, even better. You pay taxes once out of your pay check and never have to pay taxes on your returns or withdrawals. Maybe you want to retire by 40 through entrepreneurship, fair enough. But if you fail, you'll have that Roth IRA that grew tax free for 40 years. Seems like a good deal to me.