How a No-Deal Brexit Will Strategically Weaken the UK and Lead Them Into a Recession

What a 'No-Deal Brexit' Actually Means

Intro

One of the hottest political saga’s that unfolded (and continues to do so) is Brexit. Since June 2016 when it was first announced, Brexit has been a major talking point for governments, private corporations, as well as for the ordinary citizen. Off late, the focus has shifted toward the possibility of a ‘No-deal Brexit’ and this has caused widespread concern from multiple standpoints. The gravity of the situation is underestimated by most people, even in the UK, as they have minimal understanding of how they will be affected. A few industries will be more affected than others. These particular industries also tend to have a strong relationship with the British economy and might see adverse effects from a no-deal Brexit.

Basic Inferences

The announcement of Brexit caused shock waves within the British economy and caused the pound to plunge to lows it had not seen for years on end. The last time the Pound fell that low was in the mid 1980’s after a record high of nearly 2.5 USD per Pound. There are always pros and cons to both appreciation and devaluation of currencies but for Britain, the implications are comparatively more peculiar. This week in India, we saw the Rupee surge to an all-time low of nearly 73 Rupees per USD. The effect of this as well as numerous corporate governance concerns saw the NIFTY 50 (Index for the National Stock Exchange, India’s largest stock exchange by market cap) fall by roughly 7%. This is the usual case with stock markets and devaluation of the national currency as majority of institutional players, mainly the foreign ones, tends to see a loss in value solely due to currency fluctuation. In the event of uncertainty, they are likely to pull their money out and wait for circumstances to settle before re-entering at a time and size they deem appropriate.

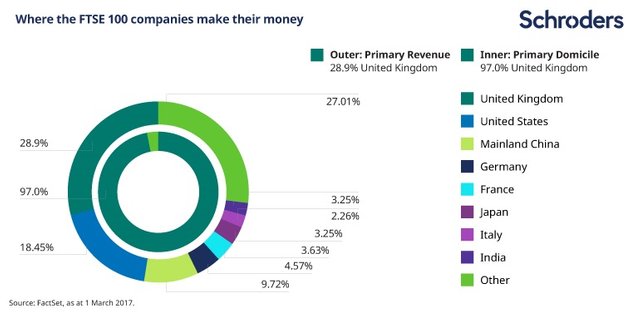

In Britain, we see a divergent situation, where depreciation of the Pound leads to higher stock market returns. Companies that make up the FTSE 100 (main index for the LSE) earn a majority of their revenue from outside the UK. That is the cause of this phenomenon. It can be seen in countries such as China, Russia, and South Korea as well, most of whom are net exporters. Breaking down the situation is quite simple; if you had $200 of sales when £1= $1.3, your total revenue in the UK would come to £152. But when the cross rate was £1= $0.9, you would earn £222. This causes financial performance and sales of UK based companies to look as though they were on the increase. It takes a while for the actual data to show up but investors with adequate knowledge of how British companies function capitalize on this and push more money into equities or equity based products.

Banking & Financial Services

Despite having the 4th largest stock exchange in the world, London is the world’s largest financial center. It has one of the largest overall equity trading volumes as well as being renowned for its debt market; especially money markets. The effect of a no deal Brexit is incredibly adverse here but the fact of the matter is that even a properly settled Brexit would shake the British financial services industry.

The UK being strategically tied with the Euro Zone was particularly important to financial firms. It meant that two of the largest economies (Euro and UK) were joint together as one economic zone, meaning a location anywhere within the UK or Euro Zone meant seamless operations throughout the rest of the area. Now that the UK wants to separate itself from the Euro Zone, tariffs and trade barriers are bound to present themselves in some form or the other. This means the large Investment Banks and FinServ companies that had their base of operations for Europe in London must downsize their UK divisions and open new offices somewhere in Europe. The UK divisions cannot be completely closed down as they will operate as the base of operations for UK customers and services.

Majority of financial companies are migrating operations to two locations; Frankfurt and Paris. HSBC is opening a new Paris division where they are set to create at least 1000 jobs, Morgan Stanley has decided on Frankfurt as their new European location, while Goldman Sachs has decided to branch out to both Paris and Frankfurt, Citi has taken the contrarian path and is headed to Luxembourg, and J.P. Morgan and Barclays plan to shift their European operations to Dublin (Northern Ireland is a part of the UK while Republic of Ireland is a part of the EU). Travel and passport issues for employees and board members remains a vital issue and is a major reason for banks to shift their European divisions. Bankers tend to travel excessively for work as their client base would be located all over Europe. Top executives and experts in a particular field like mergers & acquisitions or underwriting issues would be required to move around the country to aid local branches in servicing customers. Travel throughout Europe is likely to be an issue for those residing in the UK, with more stringent visa guidelines bound to show up post-Brexit.

Other than just the companies, the credit worthiness of UK based institutions are set to fall after Brexit. This will make international debt issues and even local ones more expensive for companies and will increase financing costs leading to an overall increase in expenses to be burdened. This is the least of their financial worries as the shifting of European wings will cause job losses across the UK.

Manufacturing

Like the ongoing trade war between the US and China, tariffs between the EU and UK post-Brexit are inevitable. What remains to be seen is whether tariffs will be based on WTO rates or self-imposed rate by each country.

European firms have halted capital expenditure and investment into their UK plants. Most companies with factories in the UK send their finished goods to other parts of the world for sale. In the automotive industry, which is set to be one of the most affected sectors, 4/5 vehicles produced in the UK are shipped and sold abroad. To offset the tariffs and duties companies would otherwise have to bear, they will shift their production capabilities to other parts of the world; mostly Eastern Europe or the EU zone. Foreign companies like Siemens and Airbus have already cut off investment to the UK and if a no-deal Brexit becomes a reality, they will abandon ship and compensate production at an existing or brand new unit.

Automotive companies are also in the line to take a massive beating if the UK walk out without a solid agreement (mainly paying the divorce bill). While it isn’t feasible for them to exit the UK soon after Brexit, it would eventually happen in a gradual manner with production being reduced and compensated for in other factories while a new production facility is set up somewhere outside the UK. But, while production cannot be immediately halted, R&D in the UK will see downsize and will be shifted to a different region. This will also lead to job loss and reduction in the size of the economy. Companies that are committed to the UK but will not hesitate to gradually transition out in the event of a no-deal include Nissan, Citroën, Jaguar Land Rover, and Volkswagen.

Food & Agriculture

Closer to the heart of the average resident, the price of food is estimated to go up by 10% due to tariffs and duties expected to be imposed. Almost all essential goods are set to see a hike in their prices, the extent of which can only be estimated depending on the outcome of the final round of negotiations between London and Brussels. Fresh and organic food will be hit the worst as the EU serves as the UK’s largest trading partner in this aspect, but price increases might force them to consider their best options, which still might be the EU as transport costs of getting it from other geographical regions is multifold. The endgame is either pay requisite tariffs to the EU or to pay more to get it from other regions. Only after everything comes into play can British importers make a decision on which is more feasible.

Farms have seen their crops rot and fall due to an immense shortage of workers in the last couple of years. The falling Pound has served as primary cause of hesitation for Eastern European workers to come to the UK for seasonal harvesting work. Labor in general has seen a huge decline and the instability of the Pound seems to be at the centre of the issue. A lot of UK based farmers have started entering into partnerships with their European counterparts in an attempt to reduce the negative impact a no-deal Brexit could have on them. On the other hand, some farmers are excited at the prospect of Brexit as it leads to a once in a lifetime opportunity for the British to revamp their agricultural policy. The CAP (Common Agricultural Policy) which is an EU initiative to provide subsidies to farmers will be withdrawn from the UK, leading to £2 billion worth of subsidies being pulled away from farmers.

Overseas Territories

Mainstream media isn’t covering the impact of Brexit on overseas territories of the UK. Despite their insignificance on a size basis, the effect of Brexit will still be felt in these regions. Gibraltar will face a closed border at Spain and tightening of restrictions on it provision of services as well as movement to Europe. The Virgin Islands and Cayman Islands are financial hubs of sorts, serving as primary locations for a number of financial services companies and a host of hedge funds. These Islands will see a major decline in their client base from the EU as regulation will be levied on the EU’s end in order to discourage their citizens from giving business to British territory based companies. The Falklands which are known for their vast marine life will see a pullback in their fishing licenses. It was a widely fancied area by Spanish fisherman as it was a zero tariff area. Brexit would see the UK impose retaliatory tariffs which would in turn discourage Spanish fisherman from purchasing licenses and entering territorial waters.

These small regions relied on EU developmental funding in various disasters and natural calamities. With their divorce from the EU, the burden of financing these activities would fall on the UK.

Conclusion

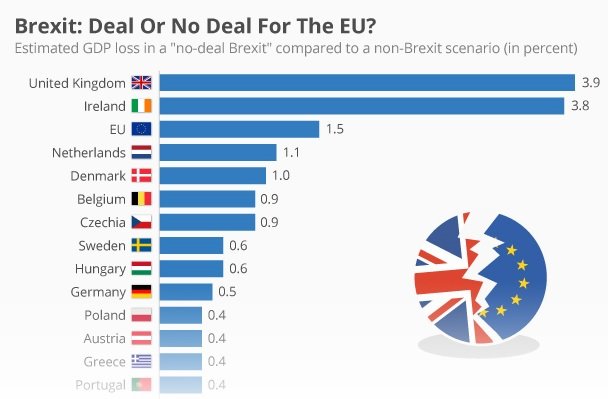

After witnessing the inefficiencies of the top brass, the general public of the UK is now leaning towards staying in the EU. Moreover, if the UK leaves without a deal, it sends a message to the rest of the world that they are unreliable trading partners. This could lead to difficulty as well as increased expenditure in securing new trading agreements. Liam Fox has said that the UK will not extend the deadline for negotiations. This is the same man who often uses the ‘vote leave’ phrase of “Let’s give the £350 million we pay to EU to the NHS”. While it sounds perfect theoretically and lets factor out the certitude of the NHS never getting that money, it has cost the UK £500 million a week to continue Brexit negotiations. This has caused the economy to backtrack, making it smaller by 2.5%. The question citizens and the government must ask themselves is if all of this is truly worth it.

Image Sources:

GDP Chart from Statista.com, FTSE 100 Revenue Chart from Schroders and Bloomberg

If majority of the EU decides to cut down on sanctions towards Britain, do you think it will be useful for Britain as it has the chance to build on its own from scratch, or do you think it is going to take a toll on them, economic and otherwise?

Good question but IMO it's an unlikely scenario in the case of a no-deal. If they leave with a mutual agreement of reduced/no sanctions, it'll still suffer losses simply because companies will have to split their European divisions into 2 factions; one for EU and one for the UK. Britain has the opportunity to reform policy as well, like I wrote about for the agricultural segment. That being said, no major structural changes are possible without seeing it eat away even more GDP than expected. That could add more steam to their recessionary troubles. Moreover, the current regime is hell bent on asserting dominance than actually doing right by their people. One of the worst governments to form in that region in a very long time.