Why the Bank of England's attempt at avoiding recession may make matters worse...

The Pound is already at multi-decade lows. Interest rates are already at a 322-year low, the lowest level in the entire history of the Bank of England. Growth in the UK economy is pacing at its slowest in decades.

The Bank of England is likely to expand its quantitative easing programme in August, as suggested by chief Mark Carney, which involes the purchases of assets to improve liquidity and borrowing conditions. The central bank is also looking at slashing interest rates to 0.25% in a bid to improve the situation and will likely be confirmed Thursday morning 11:00 GMT, despite credible reasons that this may make matters worse.

Ecology and Economics

To understandy why, view the economy as an organism and policymakers as doctors. Research has shown that the more and more policymakers try to use quantitative easing, the returns in terms of employment growth and income growth diminish rapidly. Instead of directly addressing the structural problems in the economy, this sort of monetary policy is like an antibiotic for the economy.

Patient study: Japan

The first time, quantitative easing may have had some benefits but this time it is not going to pack a punch. Also, it begs the question of where central bankers draw the line with these unconventional policies and where do we end up? Look at Japan, who spearheaded this policy, they're not in too good shape economically and they have aggressively used quantitative easing to try to influence economic activity with little success. Japan is a real-life example of an economy where the 'antibiotics' of the central bank have become ineffective.

Helicopter Ben

Japan's central bankers were also recently visited by Ben Bernanke, former Federal Reserve chief, as the government could be ready to unleash a radical form of this policy where the central bank directly funds government spending or tax cuts, eerily similar to what Weimar Germany was doing before it was struck by hyper-inflation. His advocacy of extreme monetary policies has earned him the moniker 'Helicopter Ben' referring to his reference to the idea that if needed, the Fed engage in a policy that would directly transfer created money to the private sector, which is like the Fed going around in a helicopter throwing money straight into the economy.

Bernanake is also an 'expert' on the Great Depression and in his view central banks did not do enough to remedy the situation whereas other economists argue that it exacerbated due to the central banks actions with an 'easy-credit' policy period in the 1920's followed by an unsustainable boom in stocks and bonds. This then crashed sparking the Great Depression and central banks tightened monetary policy to remedy the situation, interfering with the market's natural adjustment making matters worse.

We find ourselves in a similar situation today. But central banks today are interfering in a different way by seeing how long and how far they can extend their 'easy-credit' policies to achieve their aims.

Thank Mainstream Economics...

Switching to a theoretical perspective, there are other reasons why more quantitative easing could actually do the opposite of what it is supposed to do and harm the UK economy. The economic paradigm from the Bank of England actually believes that further quantitative easing wil benefit the economy. But mainstream economics, also known as neoclassical economics, abstracts from important forces such as the financial sector, the production of money and debt.

Also, there are mathematical oddities in this school of thought as it is based on out-dated mathematics. For example, a lot of neoclassical theory rests on the assumption the sum of the parts is equal to the sum of the whole; which is not always true. In a 'tug-of-war', the strength of one team is not the sum of each of their strengths when pulling in a one-on-one match. Slack in the rope and the opportunity to 'free-ride' means that the strength of the group is not equal to the agregation of individual's strength.

Enter the Austrian school...

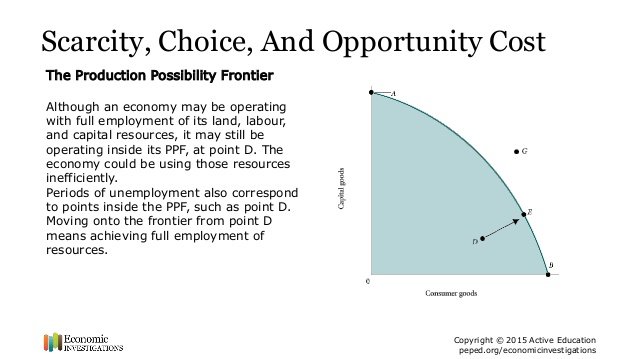

Consider the Austrian school of economics who formalise a non-mathematical, purely deductive approach to economics. Their theory of the business cycle is actually a theory about how central bank policy can induce a departure beyond, then below, the economy's production possibilites frontier; this is a theoretical construct describing the total production of goods and services, where the economy chooses betwen combinations of capital goods and consumer goods, illustrated below.

What this means is that the economy enters a boom phase, going past what resources can actually produce but then this becomes unsustianable such that the economy crashes and falls below its potential production value of goods and services.

There is an opportunity cost between producing capital goods and consumer goods and this time aspect of production is also ignored by mainstream economists. The Austrian school formalizes this as the structure of production, starting with new ventures (early-stage) such as Research and Development, capital maintenance (middle stage) leading all the way to goods that are ready for consumption (late stage). The significance of this concept is that when cental banks alter the economy's interest rate or introduce money into the economy artificially, as it does with quantitiatie easing prorammes, it alters this structure of production.

The lower induced interest rate alters the structure of production as it stimulates the production of early stage capital goods, whose payoff is in the distant future. If money is cheap to borrow now, then investing in something that pays off over the long-term becomes attractive. Excesive allocations to long-term projects are termed 'mal-investment'. On the other hand, the derived-demand effect pulls resources to the opposite side of the structure of production to satisfy the demand for consumer goods.

Visualize again a 'tug-of-war' betwen investors and consumers that arises due to this artificially low interest rate. There is a double dis-equilibrium as savers want to save less while borrowers want to borrow more. Savers save less since the return in terms of interest are reduced. This in turn reduces investment in capital goods and in processes such as Research and Development. Whereas the demand for consumer goods is artificially bloated as borrowing becomes cheaper. Therefore, investors and consumers compete for borrowing and this 'tug-of-war' leads to a disequilibrium for the economy as it moves beyond its production possibilites frontier temporarily then crashes below it due to binding real resource constraints.

"The economy is fine", they will say...

The economy will appear prosperous but the artificial boost leads to resources being under-utilized in the 'middle stage', that is there is an under-maintenance of existing capital. This drags on consumable output and the lack of genuine saving cuts the economy short from remaining above its production possibilites frontier. The economy enters into a downward spiral, known as a recession, which is exactly what the Bank of England says it is trying to avoid by intervening tommorow.

Let's increase borrowing to save ourselves from increased borrowing!

Not only does the artificiality of monetary policy reduce saving and encourage borrowing when debt is at all-time highs but it also encourages speculation. London's financial sector needs this rate cut so they can access cheap money to increase their speculative activities. The potential to lose is outweighed by the access to more money with little to no interest.

Structural and cyclical unempoyment are not distinguished between by Austrain economists since as the artifically induced boom turns to bust, much of the unemployment that appears first is associated with the early-stage liquidations. Increasing unemployment has a negative income effect; people have less money to spend leading to lower economic activity, which drives the economy further below the production possibilites frontier.

This problem is compounded if the market's adjustment is disturbed by monetary policy aimed at re-igniting a boom. So the act to prevent a recession tomorrow could potentially trigger one.

"Hi I'm Mark Carney... here markets, take my voodoo!"

Great article, let's hope some people actually read this.

If you want some info on how to promote steem posts here you got a post compilation: https://steemit.com/social-media/@top10/steemit-must-reads-collection

I'll be following you to be up to date

@top10

Since writing this, the Bank of England decided to keep interest rates at 0.5% but the market is now expecting a huge QE package in August and possibly a rate cut to 0%!

http://www.gatestoneinstitute.org/8443/brexit-eu-meddling#.V4w3Dot1C1w.twitter

Thanks for sharing your insight @jholmes91, I couldn't agree more that reducing interest rates further and increasing QE will do more harm than good. One thing I'd dispute slightly, however, is that lower interest rates cause people to save less - this is popular economic theory and may be true in some circumstances, but I've read several conflicting opinions which suggest that in actual fact they have caused people to save more due to the fact that they need more savings to achieve the same return.

One of my favourite financial publications that writes extensively on the subject is called Capital and Conflict, published by Money Week Research. They have organised a petition to the UK Government demanding the end of QE - I think anyone in the UK who's of the same opinion should sign it! The petition is found here:

Thanks again for sharing!