Cease-And-Desist: Are We Seeing Central Authority At Play With Bitcoin?

Coindesk posted an article yesterday that revealed a leaked pastebin that has been confirmed by supposed sources that was very close to the deal. This leak shows a list of banks interested in the R3cev blockchain firm.

List of banks from leaked pastebin:

R3 Fundraing Orderbook - Indication of Interest from DLG members as of 11/21/16 (Subject to Internal Approvals)

ING 3.5

Bank of America 2.5

Barclays 2.5

BBVA 2.5

Credit Suisse 2.5

HSBC 2.5

Intesa Sanpaolo 2.5

Natixis 2.5

Skandinaviska Enskilda Banken 2.5

Société Générale 2.5

UBS 2.5

Wells Fargo 2.5

Westpac Banking Corporation 2.5

State Street 2

Bank of Montreal (BMO Financial Group) 1

Bank of Nova Scotia (Scotiabank) 1

Bank of Tokyo-Mitsubishi UFJ (Mitsubishi UFJ Financial Group) 1

BNP Paribas 1

BNY Mellon 1

Canadian Imperial Bank of Commerce 1

Citigroup 1

Commerzbank 1

Commonwealth Bank of Australia 1

Danske Bank 1

Deutsche Bank 1

Mizuho Bank 1

Nomura 1

Nordea 1

Northern Trust 1

OP Financial Group 1

Royal Bank of Canada 1

Royal Bank of Scotland 1

Sumitomo Mitsui Banking Corporation 1

Toronto-Dominion Bank 1

UniCredit 1

Opted-out: Banco Santander, Goldman Sachs, J.P. Morgan, Macquarie Group, Morgan Stanley, National Australia Bank, and U.S. BancorpI do see the misspelling but on the bottom you can see the list of banks that opted-out of the project. I wonder what the reason for this was?

Either way, I see that banks are investing into blockchain technology and isn't that a good indicator for the average person to start investing into crypto-currency? Are we going to see banks create their own blockchains and what could that do to the current economy of crypto-currency?

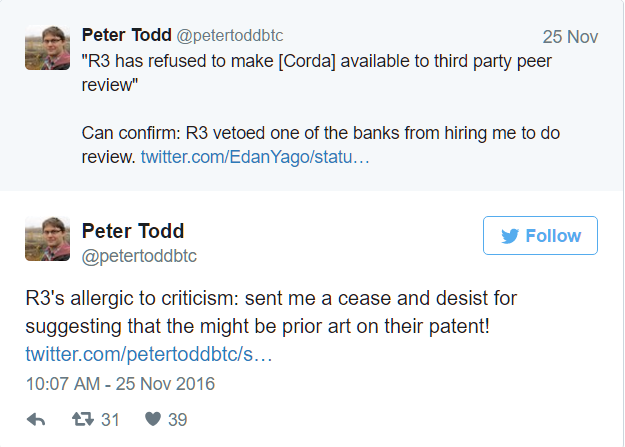

The interesting thing is, there seems to be legal twitter battle going on. R3 has apparently sent a cease-and-desist to bitcoin developer Peter Todd:

If you read the article from Goldsilverbitcoin, it seems the R3 firm is dishing legal threats against members of the bitcoin community. This is troubling to me because that looks to be a sign of centralization. Something that we are trying to get away from with blockchain technology.

Image source:Pixabay

Feel free to follow and find me in Smart Media Group on Discord.

.gif)

Facebook: @thesmartmediaproject

Facebook: @thesmartmediaproject Twitter: @the_smartmedia

Twitter: @the_smartmedia

Instagram: @the_smartmedia

Instagram: @the_smartmedia

Santander owns Ripple and is using it to build a competitor to swift, so it's logical for them to opt out. JP Morgan has it's own blockchain project in the works. Goldman Sachs same deal.

U.S. Bancorp is in with Santander on ripple... No idea on the others.

Santander is nothing to sneeze at, they are the largest bank in most of the countries they operate in and ripple should probably be called Santander coin at this point.

R3 is the wrong approach. You don't need a blockchain for what R3 is trying to accomplish. If you already have explicit trust in the members and you aren't using outside parties to validate the data then a blockchain is just overhead you don't need.

Banks know about bitcoin and crypto, but their response runs the gamut from Jamie Dimon's "This is a total scam and we will never be any part of it." To Claudio Melandri's "Hey everyone! Let's replace SWIFT!!! Hurry up for fun and prizes! Last one to the party pays the bar tab!"

FYI it's extremely unlikely that most of the banks on that list will join up with R3 once they understand what R3 is offering. Most likely this is a "golf list". Someone invited a bunch of mid-level VPs to a golf party and talked to them, but clearly these are not primary decision makers. Otherwise it wouldn't say "subject to internal approvals".

You could do something like this by purchasing a list of mid-level execs from LinkedIn and inviting them all to a conference. It would be economical, but it doesn't really build the type of solid business deal that you need when talking about moving a real financial institution to crypto land.

My advice if you're involved in crypto at all, bring your business to Santander, they get it at a fundamental level.

Yes, the banks (and the people that back them) want a digital currency.

And they will use all the buzzwords.

They will say it is a blockchain cryptographic currency, but it will be anything but.

The banks will never give up enough control. They will die first.

I've been saying for years that ripple is the perfect interbank settlement instrument except for a simple flaw that could be overcome with a few lines of code at the risk of alienating all the regular users of the currency.

In the case of ripple all the ripple that were ever to exist were mined up front. Problem is that each ripple transaction costs 1 ripple and that ripple is destroyed in the process.

For you and me this is all but meaningless, but if you're booking 100,000 transactions a day on the network you're talking about pushing up the price significantly.

It's attractive at right now prices, because it's actually cheaper than an Oracle license. But if you push the price of the coin up that advantage quickly disappears. This will raise the cost of transactions for the bank who will raise fees to compensate.

The answer of course would be to just change those limits in the coin, or at least give the fee to some operator on the network. But that would be breaking the social contract for all the ripple bag holders and devalue their currency. They would dump hardcore and if those holders were also institutional investors, they might be in a position to take legal action.

So Santander is being smart in their replace swift with ripple play. They are bringing banks on that they already have relationships with. These banks don't buy ripple as an investment, but as prepaid credit like a licensing fee. Eventually they have enough of ripple cornered that the only ones left are a handful of small players who frankly would have no standing.

FYI if you're in ripple you should run for the hills.

Wow thank you for that explanation. Yes I can see it being the "golf -list." I don't think R3 is the right approach as well but we'll see when their CORDA project launches next week. Also thank you for the advice on Santander. Something I will look into.

You're very welcome! Glad I could help. I'm in Mexico right now where Santander is huge. We'll be banking some of the VIVA coin stuff with them. So I've done my home work.

Disclaimer: I am just a bot trying to be helpful.