These Are Three Mandatory Fundamentals To Building Wealth

In the world of finance, the plethora of choices of where you can save/invest your money can be as confusing to the newcomer as it is for the novice. Instead of getting bogged down in the details of exactly which asset is or isn’t best for you, I’d like to step back and keep focus on some fundamental principles regarding wealth building. To some this may sound like common-sense, but we must get absolutely elementary in order to grasp the full scope of how to go about actually building wealth. So these are the three most important fundamentals

1. Build a habit of saving a portion of each paycheck.

Yes, it’s the old “pay yourself first” mantra that you’ve probably heard from every personal finance expert in the world already. In spite of this, it is still a timeless principle that every generation should embrace and pass on to the next. Saving and investing for the future simply means that you are continually capitalizing your own private pension, which will hopefully provide you with a sufficient and stable source of income in retirement. The main feature of any retirement account is that the income is passive, or in other words, income that is paid to you even though you don’t trade your time/labor for it. Investing for income implies just that.

The need for individuals to take the initiative to save on their own is becoming more important in today’s economy.

Practically zero industries are moving towards full-time employment, which means the old mindset of relying on a rock solid pension from a big company or government is going the way of the Dodo bird.

Far too many people have avoided personally creating savings habits simply because their employer automatically enrolls them in a 401K or pension, thus taking the very topic of retirement income out of their mind. This is irresponsible behavior IMO. Most people have no idea what kinds of investments are held in their 401K, and most certainly aren’t aware of the fund fees they are paying.

To truly understand why it’s so important to build a habit of saving, one must first appreciate a concept which is at the core of all of finance, and this is known as the time value of money.

2. Understand and Embrace the Time Value of Money

The time value of money is finance 101. It simply states that since interest can be earned on money, a dollar today is not worth the same as a dollar in the future. If someone asks for a loan of $100, and they offer to pay back the $100 in exactly one year, the lender would miss out on any interest that could be earned on that $100 in the meantime. This is where a rate of interest comes into the picture, as any lender would seek a return in the form of interest payments on their loan. There are many factors which affect the actual rate itself, but the core all interest is based on the time-preference of the individual lender and debtor.

To embrace this concept, one must put their money into an income-producing asset as opposed to letting the money sit idle. Even earning a few measly basis points on an online checking account is far better than letting your cash sit in account that pays no interest or even worse, charges you a monthly fee just for depositing your money with the bank. In the current financial landscape, online savings accounts are generally the best options for American and Canadians(the markets I’m most familiar with). Once the money is in an interest bearing account, the next and arguably most important principle take place, and it’s known as compound interest.

3. Understand and Embrace Compound Interest

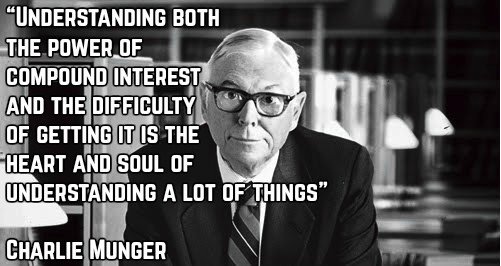

A famous Einstein quote is often used in regard to compound interest, but I think a quote from Charlie Munger is more appropriate since Munger along with his partner Warren Buffett are one of the best empirical example of compounding stretched out over many decades. Casual observers still view Buffett as mostly a stock picker, but that’s not true.The key to the Berkshire Hathaway fortune is built on compounding through the buying of entire businesses(wholly-owned subsidiaries), and using the earnings to buy other businesses, which in turn creates higher earnings and enables larger acquisitions. The share price of Berkshire stock in 1965 was $18/share, and today it has snowballed to $296,400/share. That is a whopping compounded annual growth rate of 20.53%.

In other words, $1000 of Berkshire stock purchased in 1965 would be sitting at $16.46 million today!

The term snowballing is most fitting when discussing compounding, as the force of it grows stronger the longer it’s allowed to go on. When an avalanche has reached its full intensity, there is basically nothing that can stop it. Herein lies the key point though:

For compounding to properly work, you MUST let it work without touching it for at least ten years, preferably many more than that.

The compounding force will never properly build up if you take away money every so often, so you must embrace the mentality of letting the money grow without viewing it as readily spendable.

There are methods to automate both the habit of savings and the reinvestment of the interest/dividends, but my view is that you must hammer down the basic understanding of the principles talked about here in order to be motivated to begin creating new habits. You will be much more likely to begin and stick to a purposeful plan of saving and investing if you can generate some level of excitement about it to begin with.

Pic Sources:

http://massrealestatevoice.com/channels/lending

Some good advice ! But what has worked for the past 60-70 years may not work now. The days of investing in stocks may be over in 5 to 10 years because of the increasing demand for cryptocurrencies. Instead of a IPO the next big thing is a ICO. If Uber needs to raise funds to expand into self driving cars 🚗 will then go to Wall Street or Silicon Valley?

upvote your post my friend, many thanks for sharing