How to Earn Thousands of Dollars in Credit Card Rewards

This year I've made a couple thousand dollars from using credit cards. For a lot of people credit cards are dangerous, a last resort, and the root of all money problems. Used wisely though and you can earn some lucrative rewards for very little effort.

Levels

There are a couple of "levels" of credit card rewards - there's your Regular Joe, who maybe has a cash back card that they occasionally put purchases on (or maybe they have a store credit card). Next there's the Casual Fan (where I'm at) who uses a credit card for everything to get as much cash back as possible and maybe goes for a sign up bonus every once in a while. Finally, there's the Churner - the Churner likely prefers airline miles and travel cards and goes for multiple sign up bonuses (I'm talking the $500-$1000 ones, and yes there are bonuses that high!). To meet the requirements, they have systems in place to "manufacture spend", or transfer money (usually in the form of buying gift cards and using the gift cards to pay off the credit card, although this is becoming more difficult).

Churning requires the most time and effort, and there are some great blogs and communities out there for the ultra-serious (I like flyertalk.com and thepointsguy.com).

A Casual Fan, like myself, can get tips and inspiration from the Churners, but don't want to put in as much effort.

A Regular Joe can become a Casual Fan and increase their rewards by several thousand dollars, depending on their spending.

How?

How To Become A Casual Fan

The cardinal rule of credit card rewards is this:

NEVER PAY INTEREST

If you can't pay off your credit card IN FULL EVERY MONTH, stop reading and come back when you can. Any rewards will instantly be wiped out by a 27% interest rate.

Now that that's settled, let's really begin.

First, you need to have an idea of what your expenses are. One so you can KNOW you can afford to put all your expenses on a credit card (which takes no effort as you likely use a debit card for a lot of things anyways) and two so you can know when big expenses occur throughout the year. Big expenses are great - if you plan for them and have the money to cover them up front (like bi-annual car insurance, income taxes, big purchases) because they can help you get the BIG bonuses.

For instance, cards with bonuses in the $500-600 range (the Chase Sapphire is probably the best) require you to spend something like $3-4000 in the first 90 days to get the bonus.

By putting all your expenses on the card, you might be able to get there depending on your level of spending. If your regular expenses aren't enough, you need to time your opening of the card with an upcoming big purchase and put it on the card to get you over the hump.

For me personally, I pay my car insurance every 6 months, so that's a good chunk of change that I can use towards a sign up bonus.

Finding the Right Card

After you have an idea of how much you can spend and what you want to use your points for, it's time to find a card. I check one site for this - Hustler Money Blog. It's updated multiple times a day, has reviews and the latest offers from credit card companies. The community and comments sections are also super helpful.

Annual Fees

Most of these cards come with an annual fee (anywhere from $99-$200), but many waive them for the first year. Sometimes the card is worth keeping if your rewards outweigh the annual fee. In most cases it's best to cancel the card after a year. Set a reminder in your calendar for a couple weeks before your opening/application date.

Redemption

Also pay attention to how to redeem rewards and what to redeem them for. If you want to fund travel, look at things like bonuses for booking travel through the credit card (Chase is great for this), whether or not you can get reimbursed for travel booked through another website, or how easily points transfer to airlines and hotels.

If you're in it for the cash back, pay attention. Some cards give cash back at a 1:1 ratio, which means that if you have, say, 1000 points, that's worth $10 in cash back. Others are more stingy and have a 2:1 ratio, so if you have 1000 points, you're only getting $5.

Sometimes a card that has a bad regular cash back ratio has a 1:1 gift card ratio. In this case I recommend buying gift cards with your rewards and selling them online (or you can get gift cards to places you frequent or to stores where you have an upcoming large purchase). Selling gift cards will only get you 80-90% of the value of your points, but it's a lot better than 50%.

Before you apply for a card, familiarize yourself with the major brands (Chase, Citi, Amex, Barclaycard, Discover) and their rewards systems and point values. These change every so often so keep an eye out. For example, Chase has Ultimate Rewards, so google search Chase Ultimate Rewards Value and you'll be presented with a list of the options for points.

I also recommend having some idea of what you want to use your rewards for before you choose a card. While I think hitting a $500 sign up bonus is doable with minimal extra effort, I still want to get as many points out of the deal as I can.

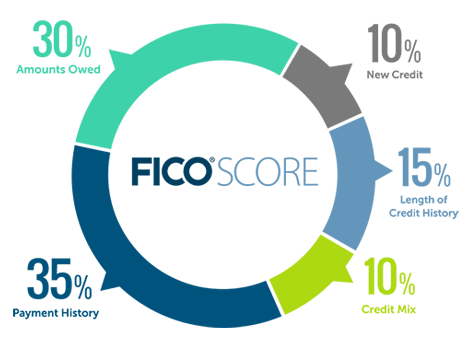

How Will This Affect My Credit Score?

Not a lot, actually, assuming you PAY YOUR CARDS IN FULL EVERY MONTH.

Opening 2-3 new credit cards a year isn't going to hurt your credit as long as you make your payments on time.

How Much Can I Make?

I have roughly $15-$17,000 a year of spending that I can put on a credit card. I use a Chase Freedom to get 5% back in rotating categories, which usually gets me around $200 a year. For all my other spending I use the Barclaycard Cashforward and get 1.5% back on everything - this comes to $20-30 a month. If you spend a lot on gas and/or groceries, there are cards out there that have higher rewards for those categories. Finally, I go for 2-3 new cards a year. When I open a new card I put ALL of my spending on it no matter what. My other cards sit in the drawer until I've hit the minimum spend.

As you can see from my spending I'm able to generate around $1500 a year in free money - or around 10% of my spending. That's money that I can use for vacation, to cover a big purchase, to pay down debt, to do whatever I want with.

It's not uncommon for a family to spend $30-$50,000 a year. Gas, groceries, and travel are the most point-lucrative categories, and probably the higher budget items for families. Imagine being able to cover at least 10% of that by working a few extra hours a year!

Summary

If you're smart and with a little bit of planning you can create a decent amount of extra income for only a few hours of work a year.

By having a plan, doing your research, and making the easy switch to paying with credit instead of debit, you can become a master of the credit card while most folks are beholden to it.

Do you do any credit card churning, travel hacking, etc? What tips/advice do you have for beginners?

This post recieved an upvote from minnowpond. If you would like to recieve upvotes from minnowpond on all your posts, simply FOLLOW @minnowpond

Very useful info! I use my credit card to buy Bitcoin, then transfer it to another address and then to my trezor/ledger. It would take time to convert that back to cash (and I won't do that! But I have done VERY well this year. I have an annuity that pays enough each month that it keeps the interest charges down. Not that I care, because I always keep 6-12 months of cash to just throw at the fiat bank and pay off that card any day of he week. It's an emergency fun, just don't try to ever use it. It's all in how you play the game!