How the Fiat Money works and why it doesn't

In my "Essay on Money" I wrote:

"Money is an entitlement to goods and services, which came into existence, because somebody has produced goods and/or performed a service, but hasn‘t received an equal amount of other goods and services, yet." That's true for real money (gold, cryptocurrencies).

But unfortunately we live in a fiat money world. In a fiat money world (fiat = latin word for "let there be", so "fiat money" = "let there be money") money gets created out of thin air by central banks and commercial banks. Nobody has to produce goods, perform a service or save. The dream of every Keynesian.

But how can a bank create money out of thin air?

That must be a fraud , mustn't it?!

Well, kind of a fraud, but a legal one.

I will tell you everything you need to know in this essay. I will cover the following topics:

- How fiat money comes into existence and how it disappears.

- How electronic money (interbank money) works and how it comes into existence

- Why over 90% of the money gets created by commercial banks without the involvement of a central bank.

- How central bank money works and how it comes into existence

- Why it is not possible to pay back debt in a fiat money system and why the supply of money has to grow permanently

1. How fiat money comes into existence and how it disappears Fiat money comes into existence, when a bank makes a loan. Most people think, that banks take in savings and lend these savings to the borrowers. This is true some times, but most of the time the money, the borrower gets wasn't there before. The bank created it out of nothing. So in a fiat money system , money comes into existence out of debt. Let me explain this fact in more detail: Let's suppose James has $30,000 in his bank account. These $30,000 are a liability from his bank to him. But where did the $30,000 come from? Somebody had to take out a loan of $30,000.

Let's suppose it was James himself ,who took out the $30,000 as a loan from the bank. Now what did happen?

Take a look at the bank's balance sheet before the loan was granted:

Ok, now the bank grants James a loan and credits his account with $30,000. Now the banks balance sheet has to look like this:

This was all it took to create new $30,000. The bank just extended its balance sheet. If James repays his outstanding loan, the $30,000 disappear.

The money gets terminated.

Summary: Money comes into existence by extension of credit and disappears after the repayment of the loan.

But what happens when James uses the $30,000 to buy a car? How does the car dealer get his money?

2. How electronic money (interbank money) works and how it comes into existence

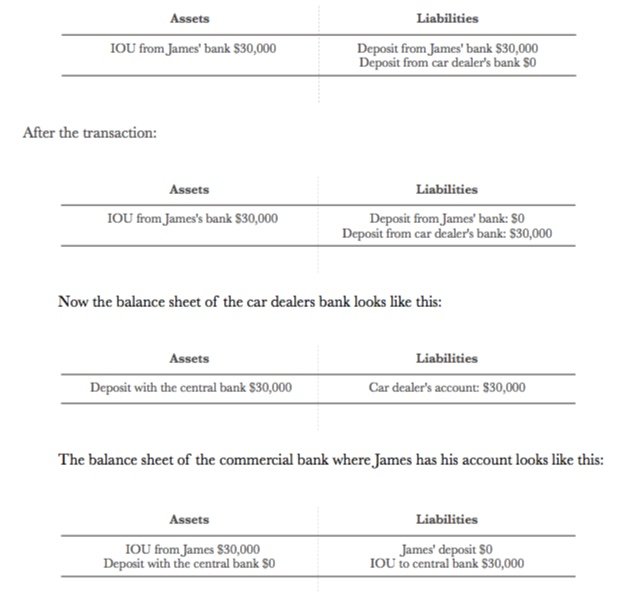

Well, it depends. If the car dealer has his account with the same commercial bank, there is no problem at all. Let's take a look at the balance sheet again:

Now James buys his new car for $30,000 from the car dealer and transfers the money to the car dealer's account:

Now a brand new car has been payed for by nothing more than numbers in a bank account (electronic money). If the car dealer has his account with another commercial bank, the situation is different. Now central bank money has to come into play.

James' commercial bank has to purchase money from the central bank.

Every commercial bank has an account with the central bank. The commercial bank can take out a loan from the central bank, but it needs a collateral and it has to pay interest for the central bank money (key interest rate). Usually the central banks takes securities like treasury bonds as a collateral. After taking out a loan from the central bank, the balance sheet of the commercial bank looks like this:

Now James' bank wires the money to the other commercial bank, where the car dealer has his account. The money gets transferred from the central bank account of James' bank to the central bank account of the car dealer's bank. Then the car dealer's bank credits his account with the $30,000.

Here's how the central banks balance sheet looks like:

Can this transaction happen without the involvement of the central bank?

Of course it can. This happens all the time, because central bank money is expensive. Therefore the commercial banks do this transactions just by delaying payments until another opposite transaction happens, which neutralizes the previous transaction.

This system broke down during the financial crisis, when the commercial banks refused to lend to each other.

3. Why over 90% of the money gets created by commercial banks without the involvement of a central bank.

Well the answer is pretty simple. Central bank money is expensive. The commercial banks need a collateral to get a loan from the central bank and they have to pay interest (key interest rate or central bank rate) for the money. Therefore they try to manage with as little central bank money as possible.

The economic textbooks tell us, that by setting the reserve ratio the central bank controls the money supply, because the reserve ratio sets the minimum fraction of customer deposits and cash which a commercial bank must hold as reserves either as cash stored in their vault or as deposit with the central bank.

Therefore a commercial bank can't lend out unlimited money. A depository institution's reserve requirements vary by the dollar amount of net transaction accounts held at that institution:

Of less than $12.4 million have no minimum reserve requirement;

Between $12.4 million and $79.5 million must have a liquidity ratio of 3%;

Exceeding $79.5 million must have a liquidity ratio of 10%.(source: Wikipedia)

Now what do these percentage numbers mean?

Let's say a commercial bank falls into category 3 and this bank has demand deposits of $10,000,000 on the right side of their balance sheet.

How much money can they lend out?

$9,000,000

But this $9,000,000 become a new deposit with another or maybe the same bank and will get loaned out again, but not the whole $9,000,000, just 90% of it: $9,000,000 x 0.9 = $8,100,000

These $8,100,000 become a new deposit and the same process starts all over again.

How far can this go theoretically or how much money can be created out of $10,000,000 and a reserve requirement of 10% according to the economic textbooks?

Well the money multiplier helps us to calculate the amount of money which can be created out of $10,000,000:

m = 1/reserve ratio

Let's do the math:

$10,000,000 x 1/0.1 = $100,000,000 Pretty good leverage...

Unfortunately this money multiplier model described in almost every economics textbook is complete nonsense. The underlying concept of the money multiplier is that in order to make loans banks first require people to deposit money. But this is not true. The truth is, when banks lend, they create deposits and they certainly don't need reserves in order to make loans. Let's see what Alan Holmes, former Senior Vice President of the Federal Reserve had to say:

"In the real world, banks extend credit, creating deposits in the process , and look for the reserves later."

4. How central bank money works and how it comes into existence

If a central bank wants to pump fresh money into the system, it creates money out of thin air and goes out into the open market and buys securities from the commercial banks. Currently the ECB is creating $30 billion every month and buys government and corporate bonds with the new created money. New created money always leads to price inflation, but nobody can foresee which prices get inflated. At present most of the new created money goes into the stock market, therefore we see moderate inflation in consumer good prices, but this fact can and will change someday.

5. Why it is not possible to pay back debt in a fiat money system and why the supply of money has to grow permanently

We have already learned, that money comes into existence, when banks extend credit and that money disappears when loans get repaid. So if all loans are repaid all the money is gone. Of course a single person can repay its loan. But not the whole system, otherwise all the money or in other words all the deposits would be gone. The truth is the supply of money and simultaneously the supply of credit has to grow permanently. Why? Because some people save (or as John Maynard Keynes would say hoard) their money and get paid interest on their deposits. And when the right side of the banks' balance sheet (liabilities) is growing, the left side (assets) has to grow, too. Otherwise there's no balance in the balance sheet. The money supply in the US's monetary system has grown in the past at an average rate of 7% and it will further grow. Therefore the banks have to try and find a new debtor every time a loan gets repaid. There is nothing we can do about, until the whole system blows up. This happened all the time in the past, just take a look at Germany after WWI and WW2, Argentina, Russia, Greece, etc. and it will happen again. But nobody can foresee when...

Great enlightenment on the flaws of fiat money and why it must fail in the end. Thanks!

That game might change in the foreseeable future, though, because the Internet now is coming for banking.