401(K): Do you have one? Will you be joining the losers' club in 2018 crash?

I had not contributed in to a 401(k) for the first 6 years of working in US. People said I was a fool for not doing so. Probably I am.

I don't like stock markets because they are filled with conniving wolves. I think 401(k) forces your money, although very cunningly, into the very hands of these wolves. When the last crash happened in 2008, Americans lost more than 2.7 trillion dollars.

That reiterated my strong stand on not contributing into 401(k). Now, I only contribute bare-minimum to get the employer's portion and I cash out a loan from this every few years (yes, you can take a personal loan from 401(k) and the interest you pay gets added to your portfolio!)

I wondered, how can you make people forget about the debacle that is not even a decade old? Then I noticed that there is a method to this.

Step 1: Target honest hard-working people: Biggest pool of 401(k) plans are honest and hard-working middle class individuals who trust that one day they can sail into their retirement. Lure them into believing that employer's are doing something for them while in reality employers are the ones that are getting the sweeter part of the deal by replacing more costlier plans for 401(k) where the match is limited. Check.

Step 2: make everything fkngly complex: I am finance graduate and when I eventually started contributing to 401(k) to bare-minimum to have employer match, I couldn't make heads or tails of the options and the agent (!) gave me an option that is supposed to be most conservative! Everything is set to code 'Complex'. Check.

Step 3: Charge fees for handling the 'complex': To convince people to pay, you make it a fractional percentage, however, you just shove it into their throats in 1000s of fractions. For example, instead of just saying 5% commission, you say, assistance fees of .5%, trade commission of .1%, customer service charge 1%, etc etc. so that people don't find a reason to resist these fees and before they know it, you mint the money and throw the hard-working and gullible investors to the winds so that other ambulance chasers can have their feast. Shoving fees in fractions and over a long period of time. Check.

Step 4: When boat sinks, let those who trusted us drown: This is what happened in 2008. Many 401(k)s lost more than 50% of their value into thin air. The most effected included people who were closest to the retirement and had no time to recoup and recover. They were forced back into the workforce. But who cares! Make more money than the investors through fees and commission, whether the investor makes or loses the money. Check.

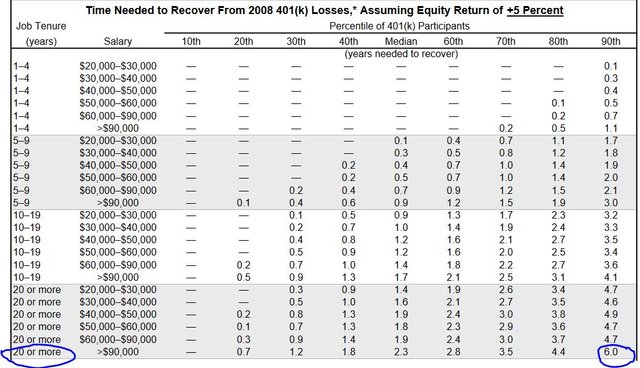

EBRI Study predicted that it will take about 6+ years to get the acounts back to where they were in 2008 at 5% yield. Sad part of this equation, as you can see below, is the longer you have worked, the longest it will take you to recover the value, not accounting for the inflation and lost opportunity etc.

Wait a second, why are we talking about 401(k)s when the market is so brim with positivity?

Probably by now, most of the 401(k) value is redeemed and we can be dandy about it and live in our lala lands?! Right?

Not quite.

IF you plot the major depressions in the US (since we are talking about 401(k)), you will see that last 3 major depressions happened within a time-frame of 8 years (average of 3).

So the logic (and some stats) tell us that next crash may be in 2018

It doesn't take an economist with 5 Ph.Ds to decipher that the next depression/crash is around the corner. My guess is that it may be in 2018.

I would love to be wrong on this one. Seriously, I don't want to see another crash that ruins the lives of so many hard-working honest people.

What can avert this could be a major technological overhaul and new jobs injected into the economy. Obviously coal doesn't that much steam left in it to deliver that. With Russia and China possibly find ways to make Chinese currency as the world currency, our USD Fiat may not be able to save the economy. What else can?

Next generation AI, blockchain, cryptos, possibly!

If not thwarted by the self-destructing Governments.

Learn from 2008 and be prepared for 2018 if you are relying heavily on a 401(k) to retire

If you are 50 or older and your biggest bet to retirement is 401(k), then be cautious. Revisit 2008 events and learn to see what you can do to avoid such a predicament.

BIGGEST RISK IN THIS WORLD IS TO THINK THAT YOU CAN BECOME IMMUNE TO RISK!

Recommended video: