🎄 True Profitable Cryptocurrency Trading 🎄 - [RESEARCH PT 7.]

Here is the thing about research: it’s not just that you have to figure out your objective, but you also need to figure out how to reach and measure your objective.

Think of it like the caveman analogy: it was not enough for him to figure out how to build a hut, but he also needed to figure out how to build the tools to build the hut.

It’s actually harder to quantify the strategy than to actually research it, since once I have a benchmarking system to compare it too, then all I need to do just to check against that, and every time I find a better system, I just use that.

Now here is a dilemma I am facing, I don’t know whether to use the Profit or the Expectancy as a benchmark for the correct strategy. I have already included both LONG and SHORT trades, so it’s not biased, however it is a dilemma since it gives biased results in terms of the number of trades itself.

Explanation

Let me explain what is happening. So my thesis is that the entry point is always random. I could enter into ETH/BTC tomorrow or in 2 days or in 1 month, it’s totally random.

Now of course you could say, but yes there are ways to figure out when there is the best time to enter into the market, but the point is that you don’t know that for certain. What if the price goes further down and you want to buy, or you want to short but it goes way up?

So it’s very random, perhaps not entirely, but it tends towards that. The only thing you can control is the exit.

So once you have entered, you can control whether to make 5% or lose 5%, cut the losses or profits short or let the losses or profits go longer. Sideways movement doesn’t count, it’s essentially zero.

So once you enter the market, it’s just the speed of whether you make money or lose money depending on how fast the market goes against you or for you.

So this means that we have to simulate what happens when we enter at random points in the market. Totally randomly.

Like if I were to trade ETH/BTC tomorrow, that would be just like entering randomly on Aug 5 or Jan 17 or March 22, from this perspective it doesn’t matter. It may have some slight edge like if it’s a bearish market, buying into it at the end is usually more profitable, but we can’t know that ahead, that is the whole point.

Once we enter, we just ride it, so we cut the losses or profits according to the risk management protocol.

Now obviously trading is not random, the strategy has to have a positive expectancy, but that has to be considering all factors, it’s not enough if the strategy works on 1 instance, it has to work on all of them, otherwise the strategy is not adaptive.

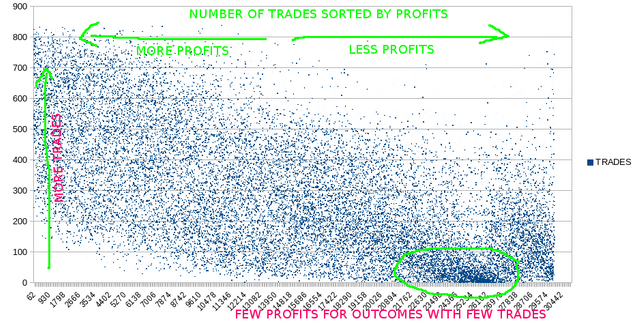

Total Profit as Benchmark

So one option is to use the total profit as benchmark. This means that the parameters will be configured in a way so that we aim for the total profit to be the highest.

Now obviously this will be heavily biased towards longer trades. So if we aim for the biggest profits, then the more trades we will have the more profits it will give. Since the number of trades is very highly correlated with the number of profits (obviously). The more trades the more profits!

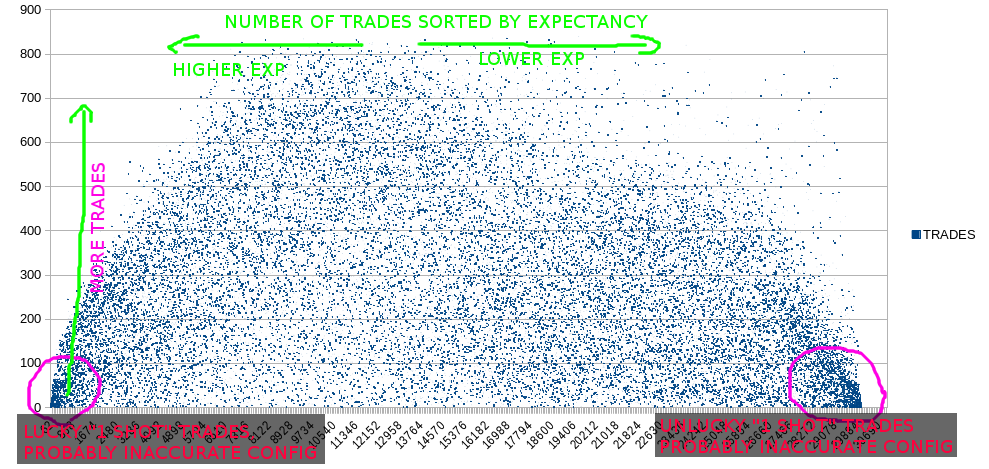

Expectancy as Benchmark

The other option is to use the expectancy as the benchmark, which doesn’t have the bias problem, but it has a “luck” problem, as in if we have fewer trades ,we could get a lot of “lucky” parameters ,which are not consistent, but just lucky as in gambling.

So we don’t know whether the parameters are consistent, into the future, or we are just lucky like winning a 5-10 streak in a casino for example.

Conclusion

So one method would be to just cutoff the outcomes where we have less than 100 trades, since the luck element will decrease the more trades we have. If we are lucky, then after 100 trades our luck should eventually run out, and if the strategy is still profitable, then it is profitable always. If not, then it’s rubbish.

The problem is that if we cutoff trades below 100, why not cutoff all trades, since the profit on the EXP chart is at the top of it. So why not just cutoff everything except the top?

So we might as well just use the Total Profit as benchmark instead with this logic, since there the profit will be biased towards the more trades we take, the more trades the more profit, the correlation is big.

Not always though since there might be events where an outcome with 200 trades will yield more profits than with 500 trades, but overall it will be biased towards the more trades.

So we might as well just use the Total Profit as the benchmark.

Okay, but the problem is that the Profit is not data-independent, it’s totally dependent on the data.

Like now I am using an older dataset, if I were to add the latest historical data, then I have to recalculate everything, since the profit should obviously be higher by now, as the nr of trades will be higher now.

Secondly, if we are biased towards more trades, then the whole point of the Monte Carlo simulation is invalidated.

Our mission is to find out what happens if we enter the market randomly at random points, but if the profits are higher the more trades we take, then we need to use the entire dataset.

So the more profit will be biased towards if we enter at the beginning and exit at the end, instead of taking small skirmishes at random intervals and random entrypoints.

So if we need to use the entire dataset to get the more profits, then the concept of randomly entering is invalidated since obviously the best outcome will be to enter at datapoint 1 and exit at the last datapoint.

So this is the dilemma I am facing, here are the pro’s and con’s:

| Benchmark | Pros | Cons |

|---|---|---|

| Profit | Eliminates “lucky” parameters and only focuses on provably good ones | Biased towards more trades, can’t have biasless random entry point analysis if it points towards using the entire dataset |

| Expectancy | Biasless random entry point analysis | Many high expectancy outcomes will come from quick “lucky” outcomes with few trades, but incorrect parameters |

Summary

So I don’t know yet how to deal with this problem. We definitely need to analyze the entry points across the board to know what happens when our entry is just totally random, but we also need to eliminate this problem. I need to think about this.

Merry Christmas by the way! If I figure this out, it could make a lot of money by the new year!

Sources:

https://pixabay.com

https://www.pexels.com/

Reminds me of looking for my Keys ,several times a Day?

Congratulations @profitgenerator! You have completed some achievement on Steemit and have been rewarded with new badge(s) :

Click on any badge to view your own Board of Honor on SteemitBoard.

For more information about SteemitBoard, click here

If you no longer want to receive notifications, reply to this comment with the word

STOP