Be a whale IRL. A retirement account strategy for Steemers in the USA.

Just like you, I'm all in rooting for Steemit. But just in case this whole cryptocurrency social network thing doesn’t work out, you better have a good backup plan. In the real world, a good place to earn “free money” is in a retirement account. Funnily enough, it kinda works like Steem Power (you put money away, earn compound interest and may even get 'contribution rewards', but in this case, from your employer).

Recently, I went deep to come up with a simple strategy to maximize my retirement savings. Hopefully, it will also set you up to make a load of money in the future.

This post is aimed at young, employed, single people for the 2016 tax year. I’ve excluded a lot of edge cases to be concise. Treat this as a starting guide before doing your own research.

tl;dr strategy

If you’re single and earn less than $US 132K:

- First, put in as much money as required into a Roth 401(k) to receive your employer’s full matching contribution.

- If you have money left (or didn’t have option 1), max out your Roth IRA up to your contribution limit (up to $5,500).

- If you still have money left, put more money into your Roth 401(k) (up to $18,000).

If you’re single and earn more than $US 132K:

- First, put in as much money as required into a Roth 401(k) to receive your employer’s full matching contribution.

- Next, put non-deductible post tax income into traditional IRA and immediately roll it over to Roth IRA (see details below under “the backdoor”).

- Still have money left? Buy Steem Power, duh. :)

If you’re married and filing jointly, the $132K threshold above is $194K.

Why in this order?

- It’s best to take the free money matched by your employer first.

- Then, it’s usually better to put your money in a Roth IRA, (compared to the employer sponsored plan), since it probably has lower fees, better withdrawal options, more investment choices, and better ways to pass funds to your kids.

The details

Account types

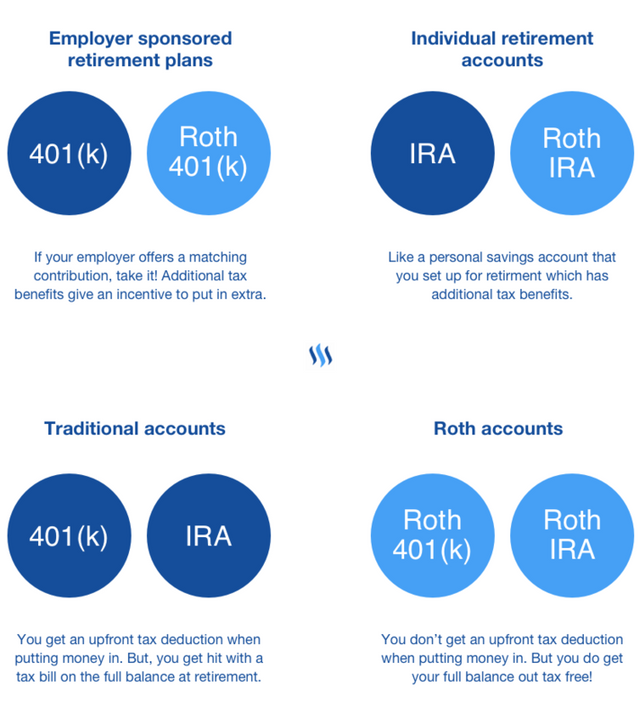

First, a quick run through of the main types of accounts:

Employer vs Individual accounts

If your company sponsors a 401(k) or Roth 401(k) with matching contributions, set it up immediately. It’s like getting free money / giving yourself a raise! If you don’t have an individual retirement account, go ahead and set one up. This is like a tax friendly, personal savings account.

Traditional vs Roth accounts (Pay tax now or at retirement)

“Roth” accounts are funded from post-tax income, which means, you don’t get an upfront deduction. “Traditional” 401(k) and IRA are retirement accounts funded with pre-tax income, so you will get an upfront deduction.

With Roth accounts, it’s like you’re paying tax on a seed (since you fund it from taxed income). While in traditional accounts, it’s like you’re paying tax on a harvest (since you fund it from pre-tax income). In most cases, you’d probably prefer to pay a smaller amount of tax upfront (on the seed), and reap the harvest tax free.

To Roth or not to Roth

Ideally, you want to pay taxes at a time in your life when your rates are the lowest. So:

Traditional (non-Roth) accounts may be best:

- If you think your income around 60 will be less than what you are making now. If so, you may as well take the upfront tax deduction which will lower you current tax bill (and may even drop you to a lower tax bracket).

- If you’re confident that you can use the money from the lower tax bill to generate a greater return than what your compounding returns in a retirement account would have earned.

- If you're living day to day or in debt and could use the upfront tax deduction now.

Roth accounts may be best:

- If you think your income at 60 will be greater than what you are making now. Note that your marginal tax rate will creep up pretty quickly if you build up multiple sources of income by retirement (e.g. from rent, dividends, bond coupons or other forms of passive income). As an example, a property that you own which rents for $3K a month makes $36K a year). Add this as income to the amount you cash out each year from your retirement account.

Another thing to keep in mind is we don’t know whether taxes will go up or down in the future. Paying tax upfront eliminates any risk of future tax rate increases but also could cost you if they go down. No one knows for sure. It depends on who’s in power and whether they believe in lower taxes and the free market, or higher taxes with society paying to finance US foreign debt, healthcare for an aging population, and unemployment benefits with the arrival of our bot overlords.

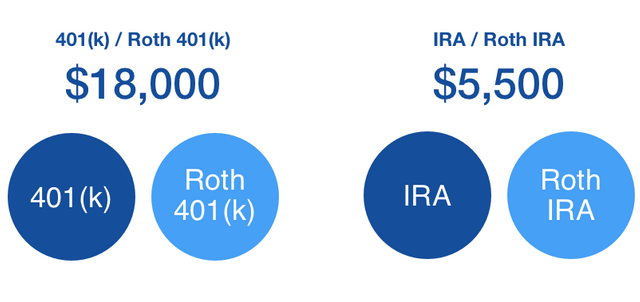

Contribution limits

There are annual contributions to both employer sponsored and individual accounts.

Note, that the $5,500 limit on IRA’s may vary based on your income:

- If you are single and earn less than $114K, you can contribute a maximum of $5,500 to the Roth IRA.

- If you earn more than $132K, you are not eligible (but see below for the “backdoor”).

- If you’re in between $114K-$132K, you’ll need to work the exact contribution limit.

- The total allowable contribution actually rises to $6,500 for people aged 50+.

The “backdoor”

If you earn over $132K, you may be able to do the ”backdoor Roth IRA”.

Basically, there are no income or account limits for rolling over to an Roth. So you could do a roll-over from your 401(k) or traditional IRA. You will get stung with tax on a Roth conversion. One way to minimize this is to put non-deductible post-tax money into a traditional IRA and then immediately do the rollover. Since you'll only owe tax on the earnings in the traditional IRA and you do the rollover immediately, you’ll pretty much avoid most tax.

Before you go ahead and try the the “backdoor” strategy, you should do your own research. Start with ’Backdoor Roth IRA’ on the Bogleheads wiki or ’Roth IRA Rules’ on Betterment’s blog

———

This is my understanding of the rules. Feel free to poke holes and correct me if I'm wrong, so we can improve our collective knowledge. Good luck out there!

Really good information. Very detailed as it case be in a post. I have the 401k, the IRA, and a 457 plan. I started when I was 22. I am 46 now. I can't stress enough to the younger generation to start as early as they can. If they start now with their first REAL job, then they won't even notice it later coming out of their pay checks.

I have put a few hundred dollars in Steem Power and deciding if a monthly transfer would be a good thing. I have been going back and fourth about the idea.

The market has been real volatile as of late. When the news came out about the hack and more people found out about it, the Steem share price jumped big time. I just wonder when this is out of beta and it starts a marketing plan and or hits some of the big news sources, how much of a jump the shares could see. A year or so, how knows how high this could be......

I agree that starting as early as possible is really important. As Albert Einstein said,

I recommend having a few sources of income, Steem Power being one. I've invested some money into Steem Power because I believe in the idea and want to support it! It is volatile but hopefully there will be a good reward for the risk!

This is what we need. SOLID. SERIOUS. Financial advice. Kudos.

Thanks! Hope it helps.