Make Your Credit Card Companies, Banks, and Stock Brokers Your B#%CH!

A summary and review of I Will Teach You To Be Rich by Ramit Sethi.

Is it possible? For years credit card companies, banks, and other financial institutions have put consumers over a barrel. Is there really a way to game them? Ramit Sethi seems to think so, and his advice is less sexy than practical. In fact he says that boring is the new sexy, and that most of your sexy options are usually wrong. Stock picking sexy? Yeah! How about those set-and-forget mutual funds that try to beat the market? Hell yeah! How about general low fee index funds and balenced ETF's and proper asset allocation? Sprints away

Alright now that all the get rich quick guys/gals are gone let's talk about building wealth, the smart and effective way, while still enjoying your life. Most of these types of books that discuss financial freedom will tell you that it's the end of the world and you need to eat cup noodles twice a day while living and a cramped up apartment and not spend a single dime on yourself. But where is all this hard earned money going to go to? Oh wall street of course, they recommend putting them in mutual funds that fail to beat the market 92% of the time. Sound stupid? Yeah, immensely.

So what's this grand system look like? How can you game your credit cards, banks, and set up a wicked cool financial automation system. Ramit recommends a few things to help. First pay down your debt. If I told you you can make an 18% return on investment guaranteed, would you hop at it? Yeah you might even think it's a scam, and it is! Stop paying interest, pay those suckers down, we're going to need them cleared off for the next steps. Next once they're paid down ramp up the rewards program and use it to buy everything. "But that makes no sense! I just paid it down and these financial gurus say to cut up the cards!" Please don't do that, here's why. You should not carry a balance on your cards, that does defeat the purpose, but if you're going to spend money anyways, why not get rewarded for it? You can get free gas, free air-miles, free money and so on. If you spend $1,000 a month on expenses including bills and you get 2% cash back, that's $20 a month and $240 a year you otherwise wouldn't of had, just for paying your bills! Additionally if you get ripped off, and you put the purchase on a credit card, you can get reimbursed and they'll take care of the crook for you (saves you a huge amount of headaches). You also get extended warranties on stuff you buy. That toaster come with a one year warranty? Double that for free by paying for it with your Visa. It's a win/win/lose (with the credit card companies losing ;))

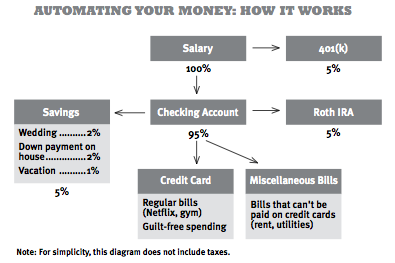

Third, set up your bank account and credit cards to work for you without your intervention. You can set up bill pay and have your savings automated. So when you open your account, you'll see that savings are automatically deposited, bills all paid with a credit card (and your bank account paying off that card so you don't hold a balance), and money going into your investment account. Also call and ask if you're paying any bank fees. Most times you are! Ask to have them waived and if they won't threaten to leave, if you've been with them long enough they'll change their tune quickly.

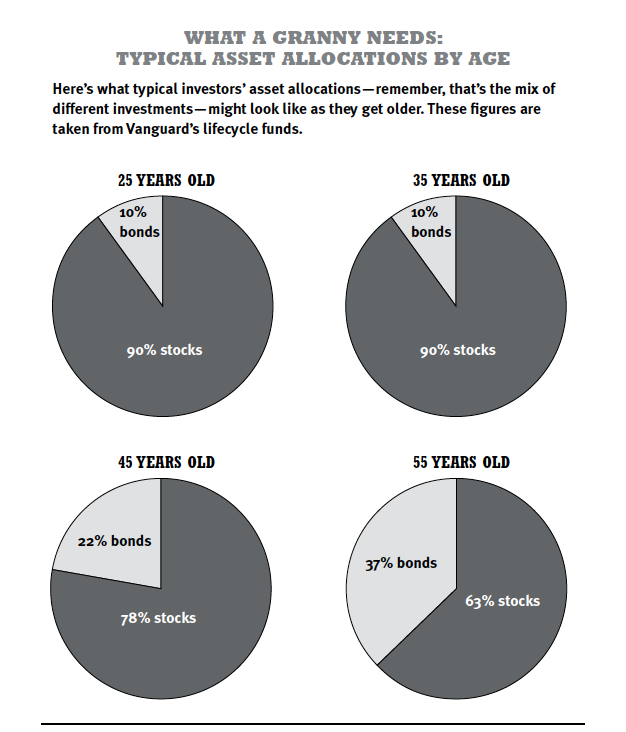

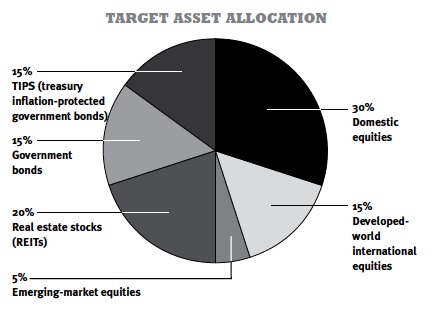

Which is what's next, how to invest without stock brokers and financial institutes blowing smoke up your ass. Asset allocation is key. You might hear gurus blab about diversification non-stop and they're right... to a point. The first thing you do is max out your 401k match with your employer, next set up a Roth IRA. Then here's where the fun happens. Below is a page from the book that outlines how you should allocate at what age:

As you can see, younger people have more risky asset classes and fewer safer investments like bonds. Below is an example of what a well balanced portfolio looks like:

Bear in mind that the equities you're investing in are not individual stocks, they're low fee index funds/ETF's. This is something you can set up within your IRA. When one part of your portfolio grows, you trim the growth and apply it to the under performing parts. How often? About once a month. That's it! No more obsessing about stock prices. Spend like 20 mins a month and you're already light years ahead of everyone else (richer too).

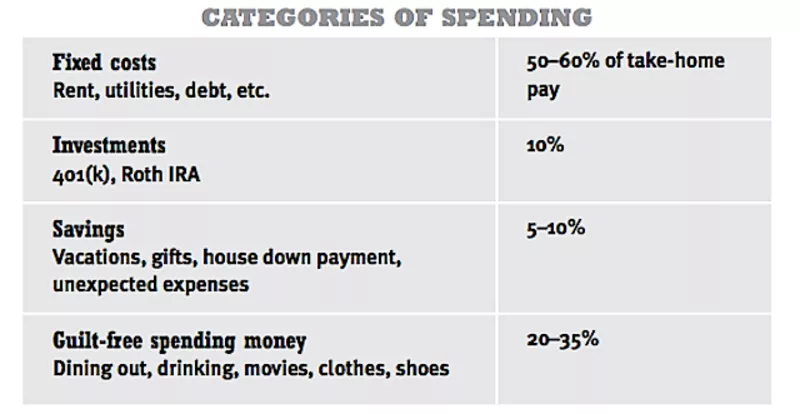

Remember when I said back in my review of The Millionaire Next Door that there's a difference between being frugal and being a cheapskate? (If not, you can read it here) So here's a quick view on how you should spend your money so you're not living like the Amish for the sake of being frugal and you can spend your money guilt free:

Oh look, there's that 10% again. Read here if you have no idea what I mean by this

So about 20-35% get spent of stuff you like. If you like dining out, it goes here. How about shoes? There's one example in the book where a woman spent $15,000 a year on shoes for her 20-35 guilt-free spending.

Review: It's a really nice book, extremely easy to read cover to cover and most likely you'll finish it in a day or three. It's a fun adventure and the language is very colorful and will keep you enthralled. There's some outdated tidbits here and there but most of what he talks about in the book is very prudent advice.

Recommendation: It's a must have! this book is fantastic and it's one of the greats. If you really want to make these predatory institutes your ich-bay then this is the direct manual on how to exactly do that including scripts on way to say and when.

Here's a link to pick up your copy if you're interested:

https://www.amazon.com/Will-Teach-You-Be-Rich-ebook/dp/B004WL4BW6

Liked this? Give an upvote! Follow for more! Next post will be about the book Rich Dad Poor Dad by Robert Kiyosaki which is a legendary book!

Until next time!