Inevitable Global Ruin: Top Hedge Fund Managers Sound the Alarm

When monetary control is centralized, as it is today, prosperity withers. The Wall Street Journal just surveyed top hedge fund managers and found a significant belief that full-fledged, global ruin is on its way. Tamper with freedom, monetarily or otherwise, and you end up facing catastrophe.

That’s just where we are today.

The managers pointed directly at the purposeful monetary mismanagement of central banks around the world. These central banks large and small are pumping oceans of money into financial markets as well as lowering rates until they are actually negative, which has never happened before in recorded history.

When the final catastrophic implosion eventually occurs, we will look back on this era with amazement, wondering how people didn’t sense the disaster to come.

Here at TDV, we’ve been quite aware of what’s going to take place right from the start. Even our name – The Dollar Vigilante – speaks to our awareness of the world’s impending monetary ruin.

We were something of a lone voice because people have a hard time visualizing that King Dollar can collapse. But before all of this is over, not a currency – or economy – will be left standing. We’ll probably have to start from scratch.

We’ve said for years that all of this ends in a rock and a hard place scenario. The two options are to stop the money printing and interest rate suppression… leading to a catastrophic crash and depression of biblical proportions. Or, to continue with it until we reach hyperinflation… leading to an even worse catastrophic crash and depression of biblical proportions.

For now, they continue on with the game. And the longer they continue playing this game the crazier everything will get.

The European Central Bank, for instance, just announced it would extend its asset purchase program until the end of 2017. Its balance sheet will soon be larger than the Federal Reserve’s. The Fed has been buying bonds for years as part of its quantitative easing program.

According to these managers, the time is nearing when the world’s overstuffed markets simply won’t be able to absorb more cash. The final collapse may be a sudden unexpected major bankruptcy or perhaps a countrywide default.

Or maybe the monetary strategy itself will cause the final damage as some managers interviewed by the WSJ suggested.

Here:

“There’s no non-messy way out of this,” said Luke Ellis, chief executive of Man Group, one of the world’s biggest hedge-fund firms with $80.7 billion in assets. “There’s two versions” of how this ends, he added.

Either central banks could move to so-called ‘helicopter money,’ where they buy debt from the government, which then spends the proceeds or gives it to the population to spend. This “for a few years looks golden then leads to hyperinflation,” he said.

Or the speed at which money circulates within the economy could grind to a halt. “Then you effectively have a barter economy,” he said.

As is normal with government programs (for central banks despite their so-called independence are basically government monetary entities), the easing programs are actually doing the opposite of what they were supposed to do.

For instance, the ECB has purchased €48.2 billion ($51.2 billion) of corporate debt in about six month’s time, but the buying hasn’t been accompanied by private sector participation.

The selectivity that markets are supposed to encourage is lacking in this case. Securities are purchased with an eye toward stimulating “growth” while large private-sector investors grow even more skeptical. With so much money flowing into markets indiscriminately, it becomes impossible to winnow out deserving companies from those that are not.

Additionally, aggressive easing over the long term encourages social dysfunction. Low-to-negative interest rates eventually bankrupt retirees and savers while those who have significant assets grow richer because a low-interest rate environment yields significant, if short-term, business opportunities while assets generally keep up with inflation to a point.

The most disturbing point that the interviews with top managers reveal involves a “hard stop.” These managers say what we’ve long understood: Once central banks sustain too-low interest rates over a significant period of time, there’s no going back. There’s no way out. Ruin on a vast – worldwide – scale is the only… inevitable… result.

Government debt-to-GDP levels continue to rise while investors pour into markets that are only an inch from collapsing because they have nowhere else to go.

What we keep in mind here at TDV is that these have long ago ceased being “normal” markets where normal investing can yield results.

Even the world’s largest firms are in chaos and if you’re going to take positions on a variety of fronts you have to think in ways that you wouldn’t have before.

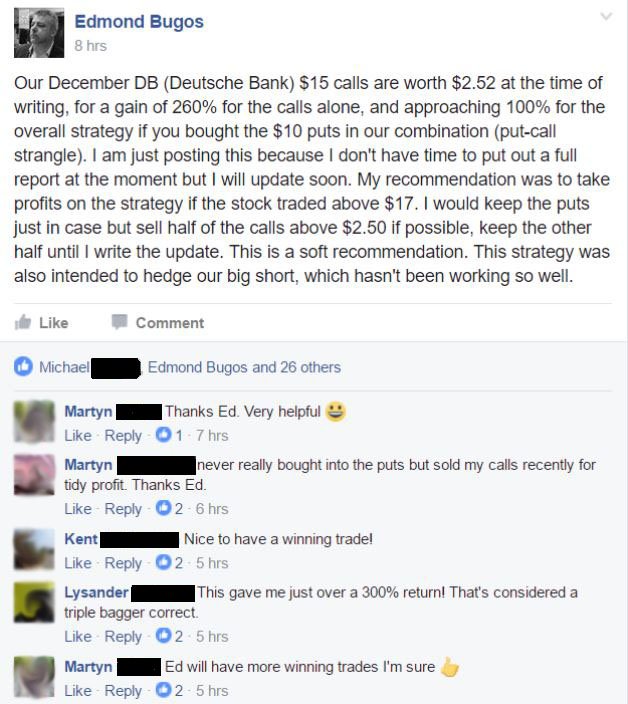

For instance, Deutsche Bank is in terrible shape, likely bankrupt as a matter of fact. But we’re also well aware that in this day and age, large institutions are basically exempt from market blowback, especially ones as large as DB.

Knowing this, we suggested subscribers buy both out of the money puts and calls on Deutsche bank.

The strategy cost $1.35 to put on: 65c + 70c for the puts and calls. So we're up 200% on the strategy or almost 500% on the calls alone. We knew that DB could go to zero. But we also believed that one way or another, at least in the short-term, various kinds of bailouts were likely to be arranged. So we hedged our bets and won.

This is important to take note of.

Here, in our daily blog, we give our general overview of what we think is going on. But we give much more specific detail and strategy in the newsletter (subscribe here).

For example, while we said that the Shemitah and Jubilee time frames could see a major crash, and there were many, including the August 2015 crash, China and Brexit… we also told subscribers to use far out-of-the-money put options to play the crash because there is also a risk of continued central bank money printing which can push the stock market much higher (albeit lower in real terms).

Through this strategy, we made 4,500% in three days last August which many subscribers made fortunes on.

Throughout 2016, we warned that Jubilee Year could bring an immediate market break and numerous economic and military disasters. But we also pointed out that, as it was with Shemitah, much of what was taking place during Jubilee could be seen as laying the groundwork for further disasters.

In fact, these hedge funds managers are talking along exactly the same lines. What has been done via government monetary policy has not yet matured into a full disaster. But as they concur, the disaster is nearly here and what’s worse, is inevitable.

We’ve shaped our entire approach to markets and news analysis around our understanding that Western monetary policy is untenable. It’s allowed us to position ourselves in such a way as to turn potential losses into significant profits. Our subscriber base, as you can see, has been handsomely rewarded as well.

I anticipate that 2017 will be a good deal worse than 2016 – by an order of magnitude. There’s simply no way global trends can continue as they are now. Cash confiscation, negative interest rates and aggressive central bank monetary manipulation will take their toll and the results will be ruinous for most, but not for us and our subscribers.

We’ve built an entire library of books and reports to help prepare you for the inevitable. And, we regularly make big gains on trades along the way. And, we have an entire network of like-minded subscribers around the world who are happy to help you prepare.

These are not normal times. And CNBC and most financial advisors are not going to even have the slightest clue of how to help protect you or help you profit during these extreme times.

To protect yourself, take advantage of our free book offer, Getting Your Gold Out of Dodge, to help you to secure and internationalize your precious metals HERE.

"The merchants of the earth will weep and mourn over her because no one buys their cargoes anymore— cargoes of gold, silver, precious stones and pearls; fine linen, purple, silk and scarlet cloth; every sort of citron wood, and articles of every kind made of ivory, costly wood, bronze, iron and marble; cargoes of cinnamon and spice, of incense, myrrh and frankincense, of wine and olive oil, of fine flour and wheat; cattle and sheep; horses and carriages; and the souls of men.

"They will say, 'The fruit you longed for is gone from you. All your luxury and splendor have vanished, never to be recovered.' The merchants who sold these things and gained their wealth from her will stand far off, terrified at her torment. They will weep and mourn and cry out: " 'Woe! Woe to you, great city, dressed in fine linen, purple and scarlet, and glittering with gold, precious stones and pearls!

In one hour such great wealth has been brought to ruin!' "Every sea captain, and all who travel by ship, the sailors, and all who earn their living from the sea, will stand far off. When they see the smoke of her burning, they will exclaim, 'Was there ever a city like this great city?' They will throw dust on their heads, and with weeping and mourning cry out: " 'Woe! Woe to you, great city, where all who had ships on the sea became rich through her wealth! In one hour she has been brought to ruin!'

Downvoted as autoreposted, autovoted and a false claim of exclusivity. This also serves as an implied upvote to all of the hundreds and thousands of actual, actively engaged steemit users.

80 downvotes with only 5 comments? Outstanding! Is this a record?

This post has been ranked within the top 10 most undervalued posts in the second half of Dec 10. We estimate that this post is undervalued by $44.14 as compared to a scenario in which every voter had an equal say.

See the full rankings and details in The Daily Tribune: Dec 10 - Part II. You can also read about some of our methodology, data analysis and technical details in our initial post.

If you are the author and would prefer not to receive these comments, simply reply "Stop" to this comment.

80 flags tells me a lot. This sort of post is no better than the media posting he so strongly opposes. Scare the hell out of people so that they subscribe to his newsletter.

It reminds me of another well known commentator who has been telling the world that the impending disaster is coming (for years and years on end). One day he will be right - but that does not help the rest of us trying to make a living and invest right now.

There is no doubt that Dollar Vigilante is right in that we do live in unprecedented times. The world has never had negative interest rates (not since the 1800's). The Global Financial Crisis was also a new phenomenon of securitized low quality debt which the world had never seen. That is why nobody knew it was coming and what to do. We are in a place where we do not know what is coming - there will be unintended consequences. That does not automatically mean that everything is broken right now.

It also does not mean that we should march forward naively. There will be unintended and unknown consequences. Our task is to watch the signals and be prepared and have contingency plans in place when the signals get strong

For example, when this chart starts rising and breaks previous levels

Chart from St Louis Federal Reserve is BofA Merrill Lynch US High Yield Option-Adjusted Spread© and can be spied here all the time http://mymark.mx/RiskIndex I check it every week.

I would like to offer another theory. Govern-cement bonds may need to be at 0% interest rates.

The old way of govern-cement bonds was to steal from tomorrow to pay for today. Taxing our children so we can have govern-cement largess now. That is evil.

There should be no benefit to those who intend to rob the unborn. So, the interest rate should be 0%. And, following this logic, as long as their is inflation, it may be appropriate to charge a percentage on the bond holder.