Bringing Fintech Innovation to the Insurance Market

Ever since Charles Darwin created his law of evolution by natural selection, the definition of progress has not been changed much. As in the past, progress stands for development, not growth. In order to survive, species have to evolve. The same theory works for any economy or market. Today’s panacea for market growth is fintech, especially in case of an insurance market, where “Insurtech” implementation is gaining momentum. MicroMoney thought of a way to make them stand out from the crowd by building its platform on a blockchain.

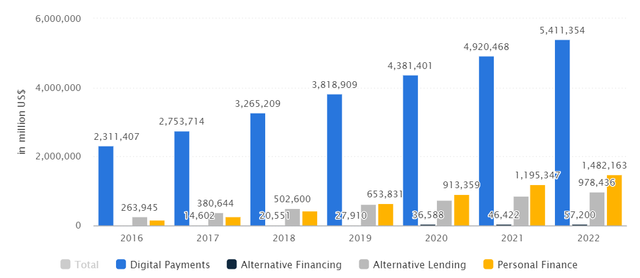

According to Statista – The Statistics Portal – Fintech is being more and more recognized and accepted.

- Transaction Value in the "FinTech" market amounts to US$4,225,551m in 2018.

- Transaction Value is expected to show an annual growth rate (CAGR 2018-2022) of 17.0% resulting in the total amount of US$7,929,153m in 2022.

- The market's largest segment is the segment Digital Payments with a total transaction value of US$3,265,209m in 2018.

- From a global comparison perspective it is shown that the highest transaction value is reached in China (US$1,562,408m in 2018).

On the other hand, the value of capital being invested in insurance technology companies globally is on the rise. The insurance industry has always been very traditional, so these new developments have the potential to dramatically change the industry. The market for underwriting improvements is set to grow by over 60 percent by 2020 (from $110.18 billion in 2016 to $175.44 billion in 2020). The market for claims processing improvements will grow by 64% passing from $44.09 billion to $72.53 billion.

The rise of InsurTech entails introduction of a multiple number of new tools and technologies that will potentially optimize and revolutionize existing business process and the whole industry. InsurTech has attracted large venture capital investments, and the trend of financing indicates that many start-ups are considered by investors to be commercially viable on a mass-scaled basis. Insurers themselves are making strategic investments in insurance start-ups, allowing them to have a stake in these developments while providing the capital for such enterprises to develop their business.

According to a research published by the Organisation for Economic Co-operation and Development (OECD), the scale of InsurTech investment is growing, and by (re)insurers in particular. As InsurTech start to attract a large number of users/policyholders, and provide an improved customer experience, (re)insurers will likely hope to capitalize on the success of such start-ups by having a stake in them. A number of (re)insurers have created strategic venture capital arms for this purpose, and have been making strategic investments in a number of start-ups.

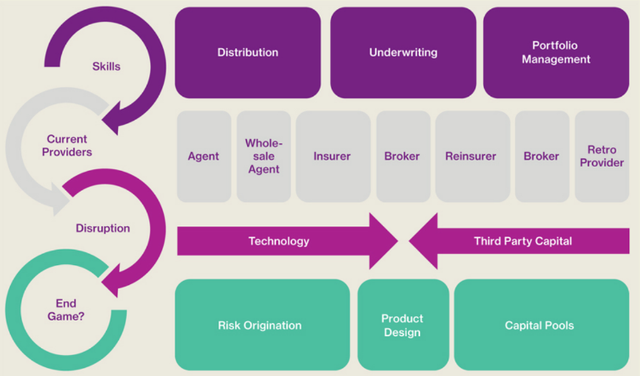

Willis Towers Watson elaborated a Pressured Insurance Value Chain:

Those companies that will decide to stay out from InsurTech, with a high probability, will shrink. Micromoney, in turn, enables cost effective entry into the insurance industry for new insurers, getting rid of the barriers of IT investment and management.

According to a research released by Venture Scanner, on the date of January 2018, there have been classified 1,422 insurtech startups into 14 categories, which collectively raised $19 billion in funding. Most of the insurtech categories are still in their infancy in terms of their funding and maturity. The Logo Map highlights the number of companies in each category and a random sampling of these companies.

The problem is that none of these companies can provide transparency, which causes the lack of credibility and trustworthiness. Meanwhile, thanks to implementation of blockchain, MicroMoney can provide smart contracts that enables borrowing in a transparent, conflict-free way while avoiding the services of an intermediary. Smart contract on a blockchain allows insurers to offer personalized products, without regard to the baggage of the legacy systems they are creating in the wake of each new product feature.

Micromoney’s business model, in fact, better addresses the insurability of policyholders by using technology to simplify the contracting process, and tailoring policies to better suit their needs. The rest of companies need to consider whether they can become the platform for some part of the industry, or take advantage of the opportunity to participate in platforms as they emerge. If innovation agendas do not include platforms, not only the innovation team, but also the company, is in a big trouble.

Good day. To get reliable insurance for yourself, it is not at all necessary to visit different companies to find the best option, since you can contact the Geico insurance company, which can offer an insurance product that will satisfy any client. Anyone can view their insurance policies on the company’s website. And if anyone needs help choosing the best insurance product, just contact geico customer service and they will offer an option that will suit both the needs and budget of the client.