Emerging Markets Are The Trade Of The Decade... But..

In Q3-Q4 2015 emerging markets bottomed out and started to rally as financial conditions tilted towards easing in Japan, Europe, and the US. Emerging markets benefited from low-interest rates and quantitative easing (QE) as we can see we have had a stunning rally since that time. Evidence from chart below implies that there is a strong correlation between easing financial conditions in the US VS emerging market performance. From early 2016 that divergence has driven the rally. We can see similar occurrences in 2000, 2004 and 2009

( US Finincial condtions in white and emerging markets in purple)

Now that finincial conditions are reversing and the fed is tightening emerging markets are very vulnurable to this tightening I am currently short emerging markets and some EM currencies

Emerging markets have also seen a huge inflow into its bond market over this period as investors and institutions look to obtain a greater yield for their investments thanks to very accommodative central bank policies of low-interest rates and QE. Unfortunately, having pushed markets to these extremes, central banks now wish to begin reversing their easing policies .This reversal, historically has not and will not be a very smooth process, it will lead to higher volatility until tightening causes cracks in the economy forcing them to relent. This, therefore, is not the time to add more risk to the table if you are a portfolio manager but rather is a time to raise cash and keep stops as tight as possible. If you are a short term trader well you dreams have come true volatility is risk and risk equals opportunity.

This increase in volatility is a trader’s best friend but the worst enemy for portfolio managers. So one of two ways a trader could play this theme is either finding opportunities to short Emerging markets and currencies vs. the USD or raise cash in anticipation of the fed relenting in its tightening efforts.

The Dollar

The Dollar is starting to break out vs. most of its trading partners as global growth has peaked and overseas cash stored by co-operations start to come back home creating dollar funding issues overseas. This is of import because as the dollar appreciates riskier assets tend to get dumped in favour of US assets. As QE nailed yields to the floor and bonds to the ceiling, emerging markets benefited from the impact of low yields due to the lower interest rates they had on their bonds. Now that the fed has reversed course and yields look to rise, emerging currencies are very vulnerable to further dollar appreciation. This market or EM currencies are not a particularly safe place to park your money in the medium term. Overall emerging markets have a fantastic story of which I am intending to write about in one of the monthly reports on ‘’ Behind The Curtain’’. The issue is, it will take many whacks over time and these might be one of those whacks.

EM currency crosses showing signs of life (USD/SGD from 2013 to present day).

USDTWD looks to have violated its price channel in a bullish manner

This phenomena isn’t just associated with emerging market currencies it is appearing across a lot of other US currency pairs.

Modern Portfolio Theory Risk

One thing that has driven returns over the last 20 years is the negative correlation between bonds and stocks. If you owned both in your portfolio the idea was that when the stock sold off bonds appreciated and vice versa and this acted as a hedge against any portfolio shocks and protected institutional portfolios from market corrections. What has happened with quantitative easing, however, is that risk assets had appreciated along with US treasury bonds whilst yields have been pushed down. Now that the fed reversing policy in the form of quantitative tightening plus raising rates we are seeing yields gradually coming up.

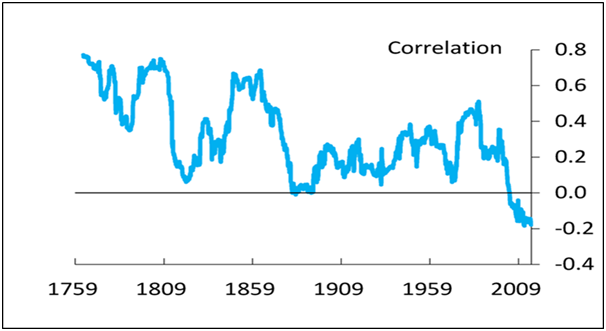

This increase in yields is risky both to the bond market and the equity market. This brings to question the negative correlation that has been around for the last 20 years between bonds and equities. According to the bank of England this correlation is about 20 years old and if you look at the data over the last 200 years the correlation has mostly been positive! i.e bonds drop and stocks drop at the same time. In this devastating scenario, THERE IS NO HEDGE!!

Chart showing positive correlation since 1759 up until the late 90s (Source BoE)

So what is a trader to do? I do not trade on the short-term basis but as a portfolio manager, it is critical to understand risks so as to adjust one's portfolio to preserve capital and avoid nights of insomnia. One recommendation I wrote about in February of this year was to short High Yield Corp Bonds. By shorting these bonds as yields climb higher it acts as a portfolio hedge in the event of any bond market tantrum.

Risks To This View

Inflation disappoints: If inflation disappoints bond yields will be on a downward trajectory and any short position in the bond market will get unwound resulting in losses from the short positions. However, some analysts think that what will happen based on the data is that bond yields and inflation accelerates and then cool off repeatedly in a two steps forward one step backwards fashion and steadily climb upwards. This volatility should be a welcome gift for short-term traders who should benefit from trading around this volatility. So I would advise traders to put these assets on their watch lists i.e. TLT, TBT, US10yr yield, US30yr yield and inflation data. Watch for yields to keep rising over 3% back below and back above in a 2 steps forward 1 step back push pull dynamic that volatility should provide trading opportunities for the less risk-averse. We Could see yields go below 2 percent but not as low as the lows in 2016.

Well Folks that is is for now if you like the content or have any questions drop a question in the comment box I will be glad to help.

Until next time keep your stops tight and your emotions steady and make sure you do your due diligence.

Many Thanks

RMD

Learn More/ Support at https://www.patreon.com/realmd

If you like the blog show some support at ETH Wallet 0xbFd2F531CdF11552f08Bce9567ce4843d8A435dd

Disclosure

There is risk in trading markets. REAL MACRO DYNAMICS reports are based upon information and research gathered from various sources and believed to be reliable but are not guaranteed as to accuracy and completeness. The information in this report is not intended to be, and shall not constitute, an offer to sell or a solicitation of an offer to buy any security or investment product or service. The information contained in this report is subject to change without notice. It should not be assumed RMD’s methods as presented will be profitable or that they will not result in losses. The indicators and strategies are provided for information and educational purposes only and should not be construed as investment advice. Accordingly, you should not rely solely on the information in making any investment. You should always check with your licensed financial advisor to determine the suitability of any investment(s).

⠀

Congratulations @thestoicobserver! You have completed some achievement on Steemit and have been rewarded with new badge(s) :

Click on any badge to view your own Board of Honor on SteemitBoard.

For more information about SteemitBoard, click here

If you no longer want to receive notifications, reply to this comment with the word

STOP