How to pay 0% tax in Australia, legally without owning a business.

How to pay 0% tax in Australia, legally without owning a business.

If you are an anarchist like myself, then you understand that taxes are a theft and we should pay very little or no tax at all. The title may sound too good to be true. Well, fortunately it is possible, quite easy to achieve and legal. I’ll explain exactly how that can be achieved shortly.

If like myself you read investment books, business articles and follow general advice from rich people like Robert Kiyosaki and Donald Trump, then you will have heard them say “the wealthy never pay taxes”.

I have heard that statement many times over the years. My initial understanding of how rich people achieved that was via tax deductions or loopholes made only available to big businesses or companies. Something that was out of reach for the common working class man.

It wasn’t until a conversation I had recently with a successful property investor who explained that there was a huge benefit investing in properties. He explained to me how investment properties can be used to bring your taxable income below the $18,000 tax free threshold, therefore not paying any tax.

I have been with a financial advisor group for years and they never told me that. Their philosophy with properties was that you were better off running them at a loss (ie negatively geared), which never made any financial sense to me.

After receiving a detailed explanation of how to achieve it, I was stumped. I didn’t believe it at first, thinking if that were true, then why wouldn’t everyone be doing it. The simple answer was that the Australian Tax Office (ATO) wasn’t going to be forthcoming, to tell investors how they could reduce their tax, that would otherwise in due course be owed to them.

Therein lies the saying, if you don’t know that something exists, then you won’t ask for it.

The information I provide below will simply help reduce the amount of tax that you currently pay and eventually how to reduce it to 0.

How it works

When you build a new house, there are certain tax deductions that you can claim on that investment.

The list of taxable allowances and exclusions are available here: https://atotaxrates.info/allowances/payg-withholding-variation-allowances/

If you buy an investment property, there is a form you can fill in and submit to the ATO that tells them your expected income for the year (you can overestimate here as it can be adjusted end of year). Once the ATO confirm the investment and associated deductions, they reduce your taxable income on file and send a letter to your employer notifying them of your new taxable income.

What makes this so great, is that you start to receive more money in your weekly/fortnightly/monthly pay packet from day one, without the need to wait until the end of the financial year to submit a tax return.

The form to submit to the ATO is called “PAYG withholding variation” and is available at: https://www.ato.gov.au/Forms/PAYG-withholding-e-variation/

An example of the tax deductions on a single investment property

These deductions are only available for newly built home and land package investment properties (not for your primary property of residence or already established homes).

To give you a current example of what a typical overall reduction in tax from an investment property would give you:

For a $420,000 Investment property, you can expect roughly $19,500 of tax deductions if your taxable income is 38.5%. For example, if your yearly income was $80,000, your taxable income would become $60,500 ($80,000 - $19,500).

The amount of taxable deductions will also reduce slightly each year as the property ages since it is a depreciating asset. For example the second year, the investment property may only save you circa $19,000 in taxable deductions.

Please note that the figures I have provided above are rough estimates of expected tax deductions from a newly built investment property as of today's date. They are not an indication of exactly what you will get as they are based on both the value of the investment and the percentage you pay on your taxable income.

This is just the beginning, as you accumulate additional investment properties, the tax deductions will accumulate eventually reducing your taxable income to less than $18,000, where you would then no longer be paying tax.

You may be thinking, yes but how rich would you need to be to buy so many investment properties. I’ll share a simple strategy with you shortly that is achievable for anyone who can afford one mortgage.

Examples of the tax deductions with numerous investment properties

If you were on an $80,000 year income, your first year new taxable income with only one investment property would be roughly $60,500. After building a second investment property, your second year taxable income would be $41,500 (Property 1 @ now $19,000 with depreciation + Property 2 @ $19,500 = $38,500 in deductions). Building a third investment property would bring your taxable income down to $23,500 (Property 1 @ now $18,000 with depreciation + Property 2 @ $19,000 with depreciation + Property 3 @ $19,500 = $56,500 in deductions).

Using this example of building a new investment property every year, after three properties you would only be paying tax on $5,500 (the amount remaining above the $18,000 tax free threshold). It would take a fourth investment property to bring your taxable income below the $18,000 level where you would then be tax free.

These deductions are rough amounts and are based on building a new property every year, however you get the idea. If you didn’t purchase a new property every year, but perhaps every couple of years then the deductions from the existing properties would just be slightly less. The more properties you own, the less tax you pay and if you own a portfolio of properties ie four or more, then you end up no longer paying taxes at all.

In time as you pay off all the loans, then you would once again be paying tax on the income from the properties. In order to keep your taxable income low or at 0, you will need to continue accruing investment properties so there is always a tax deductible debt to offset your income. There’s another saying by the rich that ‘not all debt is bad’. This is a classic example of good debt.

How to accumulate many properties quickly and easily (a simple strategy)

Firstly I need to point out that this strategy is not mine. It is a strategy I have discovered that successful property investors use.

In this strategy, the first hurdle is the largest and from there it is all downhill. Firstly you will need to buy your first home (or investment property if you wish to keep renting) and pay down roughly $50,000 – $70,000 in equity. For most people this will take a few years.

Once you have some equity in your home, then you can use that equity to buy your first investment property. Note that it is beneficial to have an agent manage your new investment property. Using an agent helps automate the care and management of the property and the tenants including maintaining occupancy.

A property located in the right area will only have a 2-3% unoccupancy rate. Any shortfall of rental income during the year would increase on your deductible investment property loan.

The loan that you take for the investment property should be an interest only loan and cover all associated costs (ie the debt, stamp duty, lawyer and conveyancer fees). Lots of banks provide interest only loans for investment properties. Here is one for example http://www.bankwest.com.au/personal/home-loans/home-loan-types/interest-only-home-loans. I don’t advocate using this bank, they are just one example. Also make sure you use a bank that allows a long period of time for the interest only period (ie 5yrs).

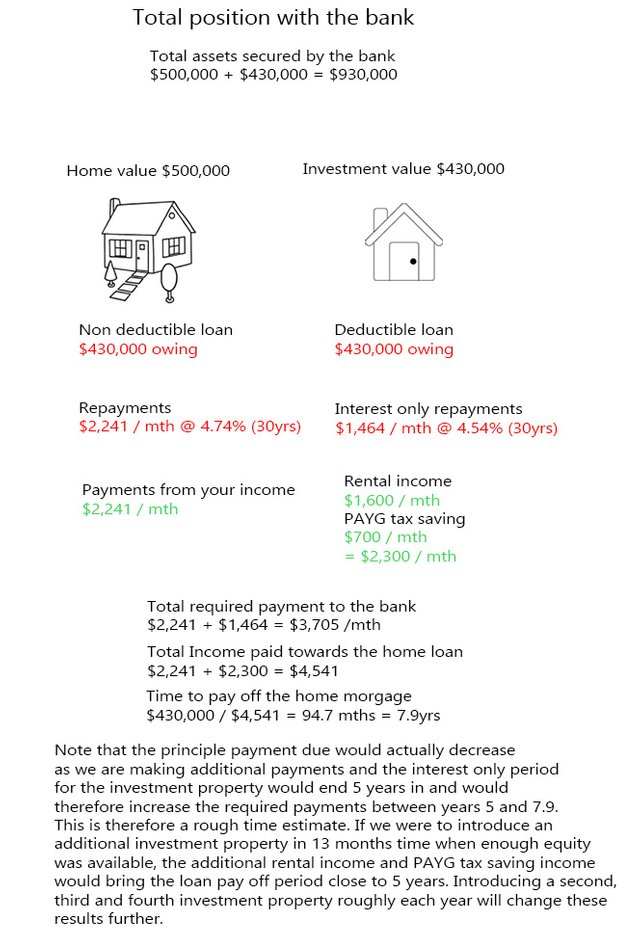

All loan payments should go towards your non deductible loan first (ie your primary property of residence). The payments would include your mortgage, rental income from your investment property(s) and the additional income received by submitting the PAYG withholding variation form. In my example below it would take roughly 8 years to pay off the loan on a home using just one investment property:

You will not have any additional out of pocket expenses using this method in addition to your original mortgage payment. Providing you use the same bank for the investment property loan that you have your home mortgage with, the bank won’t care if you pay the total principle + interest on your loans towards one property or distributed to both.

To speed things up and accumulate more properties, after another $50,000 to $70,000 of equity is available in your home, you rinse and repeat. Note that the amounts I have used here are based off a $400,000 - $500,000 property.

What makes this strategy appealing is that you are still only paying the same amount you originally were for one mortgage. Once you have some equity, you are simply making your money work for you. The aim here is to pay your non deductible debt down first, then pay down the loan on the least recent purchased investment property before the interest only period ends. If the interest only period ends first, then the combined income from your mortgage and the rental income + PAYG tax savings from each property will still cover the total principle + interest.

The information I have provided here is not financial advice, merely how to maximise your returns from investing in property and how to reduce your taxable income in the process. You will obviously still need to do your due diligence when purchasing property and research the area you choose to build in while able to make the repayments on your own home without financial hardship.

I thought this information was very valuable and worth sharing to anyone who may not be aware of this ATO form and property investing structure. If you live in a different country, it may be worth enquiring with your local tax agency about any tax withholding variation forms for investment properties to take advantage of this.

I hope you found this information as useful as I did.

Awesome info!

this applies pretty much everywhere....

In canada we have a similar system where the depreciation from capital assets reduces your taxable income, which can also apply to business assets. For property, you get a 3.5% deduction per year

so a $100,000 property would be $3500 the first year, $3377.50 the second year, and so on until there's no value left.

meanwhile this property generates you rental income, but will likely end up with an overall negative income, which will further reduce your income

technically doing this IS a business though, although you never need to officially register or incorporate. I'd suggest doing so though (at least to an asset management company of some form) after about a half dozen properties because that will further benefit you tax wise.

That was some good information

Thank you, if only I had known this information earlier on when I first bought my home back in 2008! Still, myself and my wife @Athina couldn't be happier since we started following this strategy, when we did first learn about it.

Interesting info. Guessing it's the same in Australia but here in the USSA tenants (and everyone else) are lawsuit-happy so the best advice I ever received is to make sure each rental property is owned by a separate Limited Liability Company (LLC). Not sure what the equivalent would be in Australia.

The main problem with this is it would probably change the tax deductions you get and also it would be more difficult to get the loan for the rental properties.

Man I just re-read what I wrote above, didn't mean to sound negative. Just pointing out that when dealing with tenants, and contractors etc, who are going to be on your property it's best to cover your rear end as much as possible.

Hi Kirby, you are correct about the necessary insurances to cover all things related to an investment property. I haven't included any of that advice in my post, but the general ones that would be recommended are public liability, building and contents insurance and landlord insurance. All of those are also a taxable deduction. Thanks for raising this.

taxes are theft. Thanks for sharing and putting the effort in to help your fellow humans avoid robbery. -Dave

Thanks for posting. I'll have a good read latter I hate paying tax.